Why Swiss Financial Stability Matters for Global Investors

- 14 hours ago

- 8 min read

TL;DR:

Swiss financial stability depends on the Swiss National Bank’s regulatory role, strong capital buffers, and legal system. It manages 25% of global cross-border wealth, offering currency safety, asset protection, and trusted private banking. Recent reforms reinforce resilience by requiring full capital backing for foreign subsidiaries and enhancing crisis resolution measures.

Swiss financial stability is defined as the sustained capacity of Switzerland’s banking system, monetary institutions, and regulatory framework to absorb economic shocks while maintaining continuous market function. The Swiss National Bank (SNB), UBS, and the broader financial sector collectively generated CHF 73.9 billion in GDP in 2023, representing 9.4% of the Swiss economy and employing 243,000 full-time workers. That scale makes the financial sector not just a pillar of domestic growth but a direct determinant of Switzerland’s credibility as a global investment destination. For international investors and business professionals, understanding why Swiss financial stability matters is the first step toward making informed decisions about cross-border asset allocation, company formation, and wealth preservation.

Why Swiss financial stability matters: the structural foundations

Switzerland’s financial resilience does not happen by accident. It is the product of deliberate regulatory architecture, conservative monetary policy, and a legal system that prioritizes rule of law above political convenience.

The SNB sits at the center of this architecture. Its mandate covers both price stability and macroprudential oversight, meaning it monitors systemic risk across the entire banking sector, not just individual institutions. Swiss banks are required to maintain capital buffers above minimums, including countercyclical capital reserves that activate automatically during credit booms. This design forces banks to build shock-absorbing capacity during good times rather than scrambling for capital during crises.

Several structural factors reinforce this foundation:

Common Equity Tier 1 (CET1) requirements: Swiss banks hold CET1 ratios well above Basel III minimums, giving them a genuine cushion against sudden credit losses.

Political neutrality: Switzerland’s non-alignment in geopolitical conflicts reduces the risk of sanctions exposure and asset freezes that affect banks in the United States, the United Kingdom, and the European Union.

Rule of law: Swiss contract law is enforced consistently and predictably, which matters enormously for cross-border investment structures and dispute resolution.

Foreign currency risk management: Swiss banks actively control intragroup currency transfers and maintain liquidity in major currencies, addressing a vulnerability that aggregate capital ratios alone cannot capture.

Pro Tip: When evaluating a Swiss banking relationship, ask specifically about the bank’s CET1 ratio and its foreign currency liquidity buffers, not just its headline capital adequacy figure. These two metrics reveal far more about real shock resilience.

The Credit Suisse collapse in 2023 exposed gaps in the “too big to fail” framework. Swiss regulators responded with targeted reforms rather than systemic retreat, which itself signals institutional confidence in the underlying model.

How does Swiss financial stability impact global investors?

Switzerland manages approximately 25% of global cross-border private wealth, totaling CHF 2.4 trillion in early 2026. That concentration is not coincidence. It reflects decades of trust built on political predictability, currency strength, and legal confidentiality.

For international investors, the benefits of Swiss banking translate into four concrete advantages:

Currency diversification: The Swiss franc consistently acts as a safe-haven currency during global volatility. Holding assets denominated in Swiss francs reduces correlation risk against dollar or euro portfolios.

Political predictability: Patrick Thomson, CEO at J.P. Morgan Asset Management, identifies political predictability as Switzerland’s single most important competitive advantage in 2026, particularly as geopolitical volatility reshapes capital flows globally.

Asset protection structures: Swiss legal frameworks support trusts, foundations, and holding companies that provide genuine asset segregation. Foreign investors often combine Swiss banking with offshore structures to maximize protection, since banking jurisdiction alone does not guarantee full asset security.

Private banking expertise: Swiss private banks have managed multigenerational wealth for over two centuries. That institutional knowledge is not replicable in younger financial centers.

The costs are real, however. Foreign clients face annual fees of $7,000 to $15,500 before investment charges, and minimum deposit thresholds frequently exceed $1 million. These barriers mean Swiss banking is most cost-effective for high-net-worth individuals and institutional investors rather than small-scale operators. Understanding the full Swiss banking requirements before committing capital prevents costly surprises.

The SNB’s role as ultimate crisis backstop also matters directly to investor confidence. The SNB’s resolution authority provides a credible floor under systemic risk that no private capital buffer can fully replicate. Investors who understand this distinction price Swiss assets more accurately than those who focus only on bank-level capital ratios.

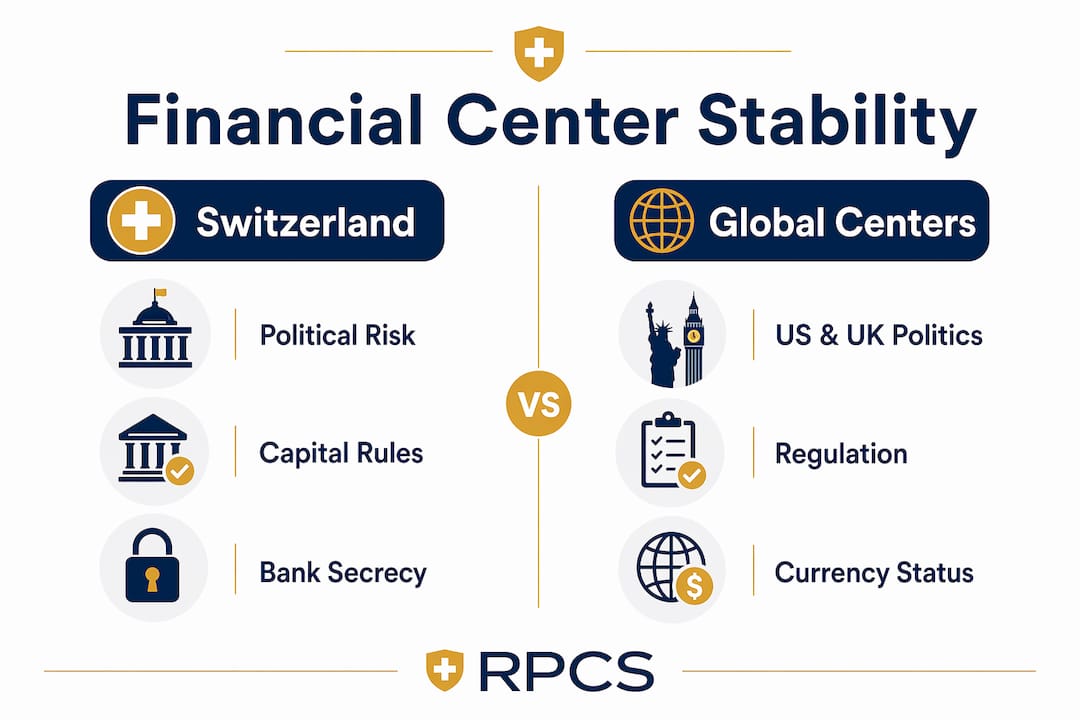

Switzerland vs. other major financial centers: a stability comparison

Switzerland’s financial stability profile differs meaningfully from New York, London, and Singapore. Each center offers distinct advantages, but the combination of factors Switzerland provides is genuinely unique.

Financial center | Political risk | Capital requirements | Banking secrecy | Currency safe-haven status |

Switzerland | Very low | Above Basel III minimums | Evolved toward transparency; strong confidentiality remains | Yes (Swiss franc) |

United States (New York) | Low to moderate | Basel III compliant | No banking secrecy | Reserve currency (USD) |

United Kingdom (London) | Moderate (post-Brexit) | Basel III compliant | No banking secrecy | Partial (GBP) |

Singapore | Low | MAS-regulated, strong buffers | Limited confidentiality | No |

Switzerland’s neutrality gives it an advantage that New York and London cannot match. Both American and British financial institutions are subject to extraterritorial sanctions regimes that can freeze assets with limited judicial review. Swiss institutions operate under a different legal framework, and the evolution of Swiss banking secrecy has moved toward international transparency standards without abandoning the core confidentiality protections that attract private wealth.

Singapore is the closest competitor in Asia, offering political stability and strong regulation. But Singapore lacks the Swiss franc’s safe-haven status and does not have Switzerland’s depth of private banking expertise or its centuries-long track record in wealth preservation.

Pro Tip: Investors comparing Switzerland with Singapore should examine each center’s treatment of trust structures and foundation law. Swiss foundations offer legal protections that Singapore’s trust framework does not fully replicate, particularly for multigenerational estate planning.

The importance of Swiss finance to global markets also shows up in crisis behavior. During the 2008 financial crisis, the 2011 European debt crisis, and the 2020 pandemic shock, Swiss franc assets appreciated while other currencies fell. That pattern is not random. It reflects deep structural trust in Swiss institutions.

What recent developments are shaping Swiss financial stability in 2026?

The Credit Suisse crisis forced a fundamental reassessment of Swiss financial regulation. The Federal Council and the SNB responded with a package of reforms announced in april 2026 that address the specific vulnerabilities the crisis exposed.

Key developments include:

Full CET1 capital backing for foreign participations: New 2026 regulations require Swiss banks to hold full CET1 capital against their foreign subsidiaries. This closes a loophole where capital held at the parent level did not fully protect against losses in overseas operations.

Tightened “too big to fail” rules: The Federal Council has expanded the scope of resolution planning requirements, ensuring that UBS and other systemically important banks maintain credible wind-down plans.

Liquidity requirements: New intraday liquidity monitoring rules require banks to demonstrate real-time capacity to meet obligations in multiple currencies, not just end-of-day aggregate positions.

Accountability culture shift: Swiss Finance Minister Karin Keller-Sutter has stated publicly that banks must contribute to stability by limiting risks to taxpayers, signaling that the government no longer acts as an unconditional backstop.

“Everyone must contribute to stability.” — Karin Keller-Sutter, Swiss Finance Minister, 2026

These reforms matter for international investors because they reduce moral hazard without undermining the SNB’s crisis management role. The Swiss government is explicitly shifting stability responsibility onto banks themselves, which aligns incentives more effectively than blanket government guarantees. For investors considering Swiss regulatory environment exposure, these changes represent a more durable stability model, not a weaker one. The international banking security implications of these reforms extend well beyond Switzerland’s borders, influencing how global wealth managers structure cross-border portfolios.

Key Takeaways

Swiss financial stability rests on the SNB’s regulatory authority, above-minimum capital buffers, political neutrality, and 2026 reforms that shift accountability directly onto banks, making it the most reliable foundation for cross-border wealth preservation available today.

Point | Details |

SNB as ultimate backstop | The SNB’s resolution authority provides crisis confidence that bank capital alone cannot deliver. |

25% of global private wealth | Switzerland manages CHF 2.4 trillion in cross-border assets, reflecting deep institutional trust. |

2026 capital reforms | Full CET1 backing for foreign subsidiaries closes the key gap exposed by the Credit Suisse collapse. |

Real costs for foreign investors | Annual fees of $7,000–$15,500 and $1 million+ minimums mean Swiss banking suits high-net-worth clients. |

Political neutrality advantage | Switzerland’s non-alignment reduces sanctions exposure that affects U.S. and U.K. financial institutions. |

Switzerland’s stability is more than a marketing claim

I have spent years working with international entrepreneurs and investors who treat “Swiss stability” as a vague reassurance rather than a specific, analyzable set of institutional features. That misunderstanding costs them money.

The real insight is this: Swiss financial stability is not primarily about banking secrecy or low taxes. Those are secondary benefits. The core advantage is the SNB’s integrated role as both monetary authority and resolution backstop, combined with a legal system that enforces contracts without political interference. No other financial center combines those two features at the same depth.

The Credit Suisse crisis actually strengthened my conviction here. The Swiss system absorbed a major bank failure without systemic contagion, without a depositor panic, and without a currency crisis. That outcome was not luck. It was the product of the exact regulatory architecture described in this article. The 2026 reforms build on that foundation rather than dismantling it.

My practical advice for investors: do not evaluate Swiss financial security in isolation. Combine a Swiss banking relationship with a properly structured Swiss company or holding entity. The combination of Swiss asset protection structures and banking access provides far stronger protection than either element alone. The costs are real, but for serious cross-border investors, the risk-adjusted value is clear.

— Rolands

How Rpcs helps you access Swiss financial stability directly

Establishing a Swiss company is the most direct way for international investors and entrepreneurs to access the full benefits of Swiss financial stability, including local banking relationships, credible business addresses, and a legal presence within the Swiss regulatory framework. Rpcs specializes in Swiss company formation for foreign clients, covering GmbH and AG structures, legal documentation, notarization, registration, and banking setup. The platform also provides registered business addresses, accounting services, and ongoing compliance support, so you can operate within Switzerland’s stable financial environment without needing local expertise from day one. If you are ready to position your business inside one of the world’s most resilient financial systems, Rpcs is the starting point.

FAQ

Why does Swiss financial stability matter for international investors?

Swiss financial stability provides political predictability, currency safe-haven status, and a credible regulatory backstop through the SNB, making it the most reliable environment for cross-border wealth preservation. Switzerland manages 25% of global cross-border private wealth, which reflects the depth of institutional trust investors place in the system.

How does Switzerland maintain financial stability?

Switzerland maintains stability through SNB macroprudential oversight, above-minimum CET1 capital requirements, political neutrality, and 2026 reforms requiring full capital backing for banks’ foreign subsidiaries. These structural features work together to absorb economic shocks before they become systemic crises.

What are the main costs of Swiss banking for foreign investors?

Foreign investors typically face annual fees between $7,000 and $15,500 before investment charges, with minimum deposit thresholds often exceeding $1 million. These costs make Swiss banking most practical for high-net-worth individuals and institutional investors.

How do the 2026 Swiss banking reforms affect stability?

The 2026 Federal Council reforms require full CET1 capital backing for foreign bank subsidiaries and tighten “too big to fail” resolution requirements. These changes reduce taxpayer exposure and align bank incentives with long-term stability rather than short-term risk-taking.

Is Switzerland still the best financial center for wealth management?

Switzerland remains the leading global wealth management hub, managing CHF 2.4 trillion in cross-border assets as of early 2026. Its combination of political neutrality, SNB crisis authority, and deep private banking expertise is not matched by New York, London, or Singapore.

Recommended

Comments