How to Meet Swiss KYC Requirements in 2026

- 6 hours ago

- 8 min read

TL;DR:

Meeting Swiss KYC requirements involves comprehensive customer due diligence under FINMA and VSB standards, from identity verification to beneficial ownership disclosure. International businesses must gather proper identification documents, apply risk-based due diligence, and leverage technology like AI and blockchain for efficient compliance. Common pitfalls include incomplete disclosures, outdated files, and insufficient staff training, which can lead to regulatory penalties and delayed onboarding.

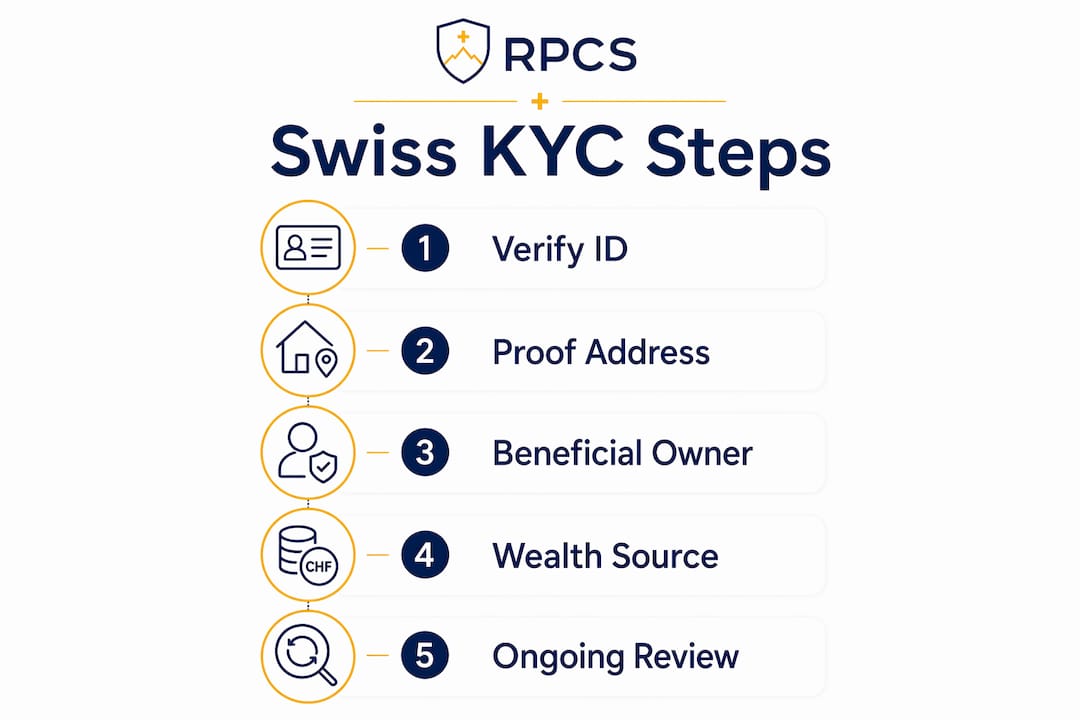

Meeting Swiss KYC requirements means conducting thorough customer due diligence under standards set by FINMA (the Swiss Financial Market Supervisory Authority) and the Swiss Banks’ Code of Conduct, known as the VSB. These two frameworks define every step of the verification process, from collecting government-issued identification to disclosing beneficial ownership. FINMA mandates compliance with AML and KYC rules, and noncompliance risks penalties including license revocation. This guide gives international businesses and financial institutions a practical, step-by-step path through Swiss KYC compliance, covering required documents, risk-based due diligence, technology tools, and the most common mistakes to avoid.

How to meet swiss KYC requirements: documents and ID

Swiss KYC compliance starts with collecting the right documents before any business relationship begins. The VSB sets private-law standards for client and beneficial owner identification, and violations can result in fines up to CHF 10 million. That penalty level signals how seriously Swiss regulators treat incomplete or inaccurate documentation.

Accepted government-issued identification includes:

Passports (required for non-Swiss nationals)

Swiss national identity cards

Swiss residence permits (for foreign residents)

Proof of address must accompany identity documents. Accepted formats include utility bills, bank statements, and official correspondence, all dated within the last three months. Digital copies are increasingly accepted, but institutions often require certified originals for high-risk clients.

Beneficial ownership disclosure is where many international businesses stumble. Required forms include Form A for individual beneficial owners, Form K for corporate controlling interests, and Form S for foundations or trusts. Each form serves a distinct legal purpose, and submitting the wrong one delays onboarding significantly.

Source of wealth and source of funds documentation rounds out the package. Clients must provide tax declarations, audited financial statements, or inheritance documentation to prove the legitimate origin of assets. Swiss KYC has shifted from reputation-based verification to absolute transparency requiring complete and auditable documents, including transaction trails.

Pro Tip: Prepare a compliance document checklist tailored to your client’s legal structure (individual, corporation, or trust) before initiating onboarding. Sending a structured request upfront cuts back-and-forth by days.

Video verification and selfie checks are now standard practice at many Swiss institutions. These methods confirm that the person submitting documents matches the identity claimed, adding a biometric layer that paper alone cannot provide.

How does risk-based due diligence work in swiss KYC?

Risk-based due diligence is the operational core of Swiss KYC compliance. Not every client carries the same risk, and Swiss regulations require institutions to calibrate their verification depth accordingly.

Conduct an initial risk assessment. Classify each client as low, medium, or high risk based on factors including country of origin, business type, transaction volumes, and whether the client is a politically exposed person (PEP). Swiss institutions use risk matrices aligned with FINMA guidance to standardize this step.

Apply standard due diligence for low-risk clients. Collect the required identification and beneficial ownership forms. Verify the documents against official databases. Document the process and store records securely.

Apply enhanced due diligence (EDD) for high-risk clients. EDD requires deeper investigation into source of wealth, additional reference checks, senior management approval, and more frequent review cycles. PEPs, clients from high-risk jurisdictions, and clients with complex ownership structures always trigger EDD.

Monitor transactions on an ongoing basis. Financial institutions must use risk-based procedures including ongoing monitoring and updating client information when circumstances change. A client who was low-risk at onboarding may become high-risk after a major transaction or change in business activity.

Report suspicious activity to MROS. The Money Laundering Reporting Office Switzerland (MROS) is the designated authority for suspicious activity reports (SARs). Institutions must file promptly when red flags appear, including unusual transaction patterns, inconsistent source of funds explanations, or sudden changes in client behavior.

Retain all records for a minimum of 10 years after the business relationship ends. This is a hard legal requirement under Swiss AML law, not a best practice.

Pro Tip: Schedule periodic client reviews at fixed intervals (annually for standard clients, semi-annually for high-risk clients) rather than waiting for a trigger event. Proactive reviews catch compliance gaps before regulators do.

The Swiss AML Ordinance (AMLO-FINMA) mandates that institutions establish internal anti-money laundering departments responsible for staff training, audits, monitoring, and reporting. This is not optional. Building that internal structure is a prerequisite for sustainable compliance, not an afterthought.

What technologies help with swiss KYC compliance?

Technology has changed what Swiss KYC compliance looks like in practice. Manual document review and paper-based records are giving way to digital workflows that are faster, more accurate, and easier to audit.

Technology | Primary Function | Compliance Benefit |

AI document verification | Reads and validates passports, IDs, and forms | Reduces human error and speeds onboarding |

Video KYC platforms | Conducts live identity checks remotely | Confirms biometric match without in-person meetings |

Blockchain KYC platforms | Shares verified compliance data between institutions | Eliminates duplicate verification across entities |

Automated transaction monitoring | Flags unusual patterns in real time | Supports ongoing monitoring obligations under FINMA |

Digital onboarding workflows | Manages document collection and approval steps | Creates auditable records for every client interaction |

AI-powered KYC solutions simplify verification, improve accuracy, and enable continuous monitoring. That combination directly addresses the three most common compliance failures: missed documents, delayed reviews, and undetected suspicious activity.

Blockchain-based platforms like Wecan Comply represent a newer approach. These systems allow multiple Swiss financial institutions to share verified compliance data securely, so a client verified by one institution does not need to repeat the full process at another. This reduces friction for clients while maintaining regulatory integrity.

Key considerations when selecting KYC technology:

Confirm the platform supports Swiss-specific forms (Form A, Form K, Form S)

Verify that data storage meets Swiss data protection law requirements

Check whether the system integrates with your existing client management software

Confirm audit trail functionality meets the 10-year record retention standard

The Swiss bank onboarding workflow for companies involves multiple document stages that technology can automate, reducing onboarding time from weeks to days when implemented correctly.

What are the most common swiss KYC compliance mistakes?

Most compliance failures in Switzerland trace back to a small set of recurring mistakes. Knowing them in advance is the most direct way to avoid them.

Incomplete beneficial ownership disclosure is the leading cause of onboarding delays. Many international businesses underestimate the specificity required by Form A, Form K, and Form S. A corporate structure with multiple holding layers requires a separate disclosure for each layer, not a single summary.

Physical cash complicates onboarding more than most clients expect. Handling large volumes of cash requires more rigorous and time-consuming KYC processes because cash is difficult to trace. Institutions treat cash-heavy clients as higher risk by default, triggering EDD regardless of other factors.

Outdated client files create audit exposure. Institutions that collect documents at onboarding but never update them face regulatory risk when a client’s circumstances change. A client who acquires a new business, changes residency, or becomes a PEP requires an immediate file update.

Insufficient staff training is a structural problem. The AMLO-FINMA requirement for internal AML departments includes mandatory training programs. Institutions that treat compliance training as a one-time event rather than an ongoing program consistently underperform in audits.

Pro Tip: Run a mock audit on your KYC files annually. Pull ten random client files and check them against your current compliance checklist. Gaps you find internally are far less costly than gaps a regulator finds.

Staying current with regulatory updates is also non-negotiable. FINMA issues circulars and guidance updates regularly, and the Swiss regulatory environment for financial institutions continues to evolve. Assign a designated compliance officer to monitor FINMA publications and translate updates into internal policy changes within 30 days of publication.

Key takeaways

Swiss KYC compliance requires verified identity documents, accurate beneficial ownership disclosures, risk-based due diligence, and 10-year record retention under FINMA and VSB standards.

Point | Details |

Start with correct documentation | Collect government-issued ID, proof of address, and the appropriate Form A, K, or S before onboarding begins. |

Apply risk-based due diligence | Classify every client by risk level and apply enhanced due diligence to PEPs, high-risk jurisdictions, and complex ownership structures. |

Report suspicious activity to MROS | File suspicious activity reports promptly; delayed reporting creates regulatory liability even when the underlying activity is later explained. |

Retain records for 10 years | Swiss law requires a minimum 10-year retention period after the business relationship ends, with no exceptions. |

Use technology to close compliance gaps | AI verification, video KYC, and automated monitoring reduce human error and create the auditable records regulators expect. |

Swiss KYC: what i’ve learned working across borders

Swiss KYC used to run on reputation. A well-connected client with a respected name could open accounts and establish relationships with minimal documentation. That era ended after 2008. The shift to document-based verification was not gradual. It was a structural reset, and institutions that did not adapt quickly paid for it.

What I find most underestimated by international businesses entering Switzerland is the cultural dimension of compliance here. Swiss institutions are not just checking boxes. They are building a legal record that must withstand scrutiny years into the future. That mindset requires a different approach than what most foreign clients bring from jurisdictions where KYC is lighter.

The institutions that handle Swiss KYC best are the ones that treat it as a client service function, not a legal obstacle. When you explain to a client exactly what you need and why, the process moves faster and the relationship starts on a stronger foundation. Compliance and client experience are not in conflict. They reinforce each other when the process is well-designed.

Digital currencies and blockchain-based assets will push Swiss KYC into new territory over the next few years. The Swiss banking sector’s approach to crypto already shows how regulators are extending existing KYC logic into new asset classes. Institutions that build flexible compliance infrastructure now will adapt far more easily than those locked into legacy processes.

— Rolands

How Rpcs supports your swiss KYC and compliance needs

Rpcs provides end-to-end support for international businesses establishing a compliant presence in Switzerland. From Swiss company formation under GmbH or AG structures to opening a Swiss bank account with full KYC documentation support, Rpcs handles the process steps that slow most foreign clients down. The team understands FINMA requirements, beneficial ownership disclosure obligations, and the documentation standards Swiss banks expect. Whether you need a registered business address, accounting services aligned with Swiss record-keeping law, or guidance on meeting ongoing compliance obligations, Rpcs offers the local expertise that international businesses need to operate in Switzerland without compliance gaps.

FAQ

What is KYC in switzerland?

KYC in Switzerland is the legal process by which financial institutions verify client identity, beneficial ownership, and source of funds under FINMA regulations and the Swiss Banks’ Code of Conduct (VSB). It applies to banks, asset managers, and other regulated financial intermediaries.

What documents are required for swiss KYC?

Swiss KYC requires a government-issued ID (passport, Swiss ID card, or residence permit), proof of address, and a beneficial ownership disclosure form. The correct form depends on client type: Form A for individuals, Form K for corporate controlling interests, and Form S for foundations or trusts.

What is the role of FINMA in swiss KYC compliance?

FINMA is the Swiss Financial Market Supervisory Authority and the primary regulator enforcing KYC and AML rules. It sets mandatory standards for client identification, risk assessment, and due diligence, with penalties including license revocation for noncompliance.

How long must swiss KYC records be retained?

Swiss law requires financial institutions to retain all KYC and transaction records for a minimum of 10 years after the business relationship ends. This applies to all client files, due diligence reports, and transaction documentation.

What triggers enhanced due diligence in switzerland?

Enhanced due diligence is triggered by high-risk client classifications, including politically exposed persons (PEPs), clients from high-risk jurisdictions, complex ownership structures, and clients with significant cash-based transactions. These clients require deeper source of wealth verification and senior management approval.

Recommended

Comments