What is Swiss AG: Your 2026 guide to legal, tax benefits

- Mar 17

- 10 min read

Many international entrepreneurs mistakenly believe that a Swiss AG (Aktiengesellschaft) is a joint-stock company designed for larger operations, particularly those seeking to raise capital or attract outside investors. In reality, this corporate structure offers significant advantages for businesses of all sizes, from ambitious startups to established multinationals. Beyond limited liability protection, the Swiss AG provides investor appeal, shareholder anonymity, and access to Switzerland’s favorable tax environment. This guide examines the legal framework, share capital requirements in Switzerland, governance structures, and tax benefits that make the Swiss AG an attractive choice for international business ventures in 2026.

Table of Contents

Key takeaways

Point | Details |

Limited liability and investor appeal | Swiss AG offers complete separation of personal and corporate assets while attracting institutional investors through its recognized corporate structure. |

Capital requirements | Minimum share capital of CHF 100,000 required, with at least CHF 50,000 paid in cash or assets at incorporation. |

Tax advantages | Corporate tax rates average 14.4% nationally in 2026, with Canton Zug offering rates as low as 11.85%. |

Shareholder privacy | Shareholders remain anonymous in public records while board members are disclosed for transparency. |

Governance flexibility | Professional board of directors manages operations independently from shareholders, enabling scalable decision making. |

Understanding the Swiss AG: Definition and legal foundation

The Swiss AG represents one of Switzerland’s two primary corporate forms, governed by the Swiss Code of Obligations and designed specifically for businesses requiring external capital or planning significant growth. Unlike sole proprietorships or partnerships, the AG creates a separate legal entity distinct from its owners, providing comprehensive liability protection. Shareholders risk only their invested capital, never personal assets, making this structure particularly attractive for international investors navigating unfamiliar markets.

Switzerland’s civil law system provides exceptional legal stability and predictability compared to common law jurisdictions. The Swiss corporate law AG and GmbH framework has remained fundamentally unchanged for decades, offering businesses long term planning security. Courts consistently uphold corporate structures and shareholder agreements, reducing legal risk for foreign entrepreneurs. This stability extends beyond corporate law to encompass tax policy, banking regulations, and international treaties.

The AG structure separates ownership from management through a mandatory board of directors role in Swiss AG governance. Shareholders elect board members who then oversee company strategy and operations, but shareholders themselves need not participate in daily management. This separation enables professional management teams to operate efficiently while protecting shareholder interests through clearly defined oversight mechanisms.

Several characteristics distinguish the Swiss AG from other corporate forms:

Shares can be freely transferred without notarization, unlike GmbH ownership interests

Companies can issue bearer or registered shares with varying rights and restrictions

Public listing on stock exchanges becomes possible, though not required

Institutional investors and venture capital firms recognize and prefer the AG structure

Pro Tip: If you plan to raise capital from international investors or eventually pursue an IPO, establish your company as an AG from the start rather than converting later, which adds legal complexity and costs.

The AG structure particularly suits businesses in technology, finance, manufacturing, and professional services where credibility matters. International clients and partners often view Swiss AG status as a quality signal, associating it with financial stability and professional management. This perception advantage can accelerate business development efforts in competitive markets.

Swiss AG capital requirements and corporate governance

The minimum required share capital is CHF 100,000, of which at least CHF 50,000 must be paid in at incorporation. The remaining CHF 50,000 can be called upon by the board as needed, providing flexibility for growing businesses. Founders can contribute this capital in cash, intellectual property, real estate, or other assets, subject to independent valuation for non-cash contributions. This flexibility allows technology companies to capitalize patents or software, while real estate firms can contribute property holdings.

Share capital structure follows strict legal requirements but permits creative arrangements within those boundaries. Companies can issue multiple share classes with different voting rights, dividend preferences, or transfer restrictions. Par value shares must equal at least CHF 0.01 each, while total authorized shares cannot exceed ten times paid capital without shareholder approval. These rules balance flexibility with creditor protection, ensuring the company maintains adequate financial backing.

Capital Component | Requirement | Flexibility |

Minimum total capital | CHF 100,000 | Fixed by law |

Initial payment | CHF 50,000 | Must be paid before registration |

Remaining capital | CHF 50,000 | Callable when needed |

Contribution types | Cash or assets | Assets require independent valuation |

Share classes | Unlimited | Must be defined in articles of association |

Governance operates through a three tier structure comprising shareholders, the board of directors, and executive management. Shareholders hold ultimate authority through general meetings where they approve financial statements, elect board members, and decide major corporate actions like mergers or liquidation. The board handles strategic oversight, appoints executives, and ensures legal compliance. Executive management runs daily operations within parameters set by the board.

Board composition requirements include at least one member with Swiss residency and signature authority. Larger companies often maintain boards of three to seven members, balancing diverse expertise with efficient decision making. Board members need not be shareholders, allowing companies to recruit independent directors with specific industry knowledge or professional credentials. This separation enables truly professional governance even in closely held companies.

Shareholders can remain anonymous; only the board of directors is publicly listed in the commercial register. This privacy feature attracts international investors seeking confidentiality while maintaining corporate transparency through disclosed governance. Bearer shares, which previously offered complete anonymity, now require registration with the company under anti-money laundering regulations, though this information remains private unless legal proceedings demand disclosure.

Compliance obligations for Swiss AGs include:

Annual financial statements prepared according to Swiss GAAP or IFRS standards

Ordinary audit for companies exceeding size thresholds or upon shareholder request

Commercial register updates within specified timeframes for governance changes

Proper documentation of board and shareholder meeting minutes

Maintenance of share register tracking all registered shareholders

Pro Tip: Appoint a Swiss resident with deep local knowledge as a board member from day one, even if you maintain majority control, to navigate regulatory requirements and build credibility with banks and authorities.

The governance framework balances shareholder protection with operational efficiency. Minority shareholders enjoy statutory rights to information, inspection, and special audits if they suspect mismanagement. Majority shareholders cannot simply override these protections, creating a fair environment for co-investment arrangements. This legal balance makes the Swiss AG attractive for joint ventures between international partners.

Tax advantages and market stability for Swiss AGs in 2026

Corporate tax rates in Switzerland fell from 14.6% to 14.4% year over year, reflecting the country’s commitment to maintaining competitive taxation despite global pressure for higher rates. This average combines federal, cantonal, and municipal taxes, with significant variation across Switzerland’s 26 cantons. The federal corporate tax rate remains fixed at 8.5%, while cantonal rates range from approximately 3% to over 15%, creating strategic opportunities for location optimization.

The Canton of Zug offers the most attractive corporate tax rate at 11.85%, making it a preferred location for international holding companies, trading firms, and technology businesses. Other competitive cantons include Lucerne at 12.2%, Nidwalden at 12.7%, and Schwyz at 13.9%. These low-tax cantons cluster in central Switzerland, offering excellent infrastructure and proximity to Zurich’s financial center while maintaining favorable fiscal policies.

Beyond headline rates, Switzerland’s Swiss company tax advantages include participation relief on dividend income and capital gains from qualifying subsidiaries. Companies holding at least 10% of another firm’s capital for one year pay no tax on dividends or capital gains from that investment. This relief makes Switzerland ideal for holding company structures managing international operations. Patent box regimes in certain cantons further reduce taxes on income from intellectual property, benefiting research-intensive businesses.

Cantonal tax competition drives continuous improvement in business conditions:

Cantons actively court international businesses through streamlined approval processes

Many cantons offer advance tax rulings providing certainty on complex transactions

Bilateral tax treaties with over 100 countries prevent double taxation

Withholding tax reforms reduce administrative burden on cross-border payments

Switzerland’s legal and economic stability provides risk mitigation that justifies any tax differential compared to lower-cost jurisdictions. The country has avoided recession for extended periods, maintains AAA credit ratings, and demonstrates political continuity rare in today’s volatile environment. Currency stability through the Swiss franc offers natural hedging for international businesses, while banking secrecy laws, though modified for tax compliance, still protect legitimate business confidentiality.

The Swiss legal system resolves commercial disputes efficiently through specialized courts familiar with complex corporate matters. Arbitration enjoys strong support, with Zurich and Geneva serving as major international arbitration centers. Contract enforcement consistently ranks among the world’s most reliable, reducing transaction costs and enabling confident long-term planning. These factors combine to create a business environment where companies focus on growth rather than managing political or legal risks.

Market access represents another stability advantage, with Switzerland’s bilateral agreements providing favorable terms with the European Union despite non-membership. Swiss companies enjoy reduced tariffs and regulatory alignment in many sectors while maintaining flexibility to negotiate independent trade agreements globally. This balanced approach provides EU market access without full regulatory burden, particularly valuable for financial services and technology firms.

Swiss AG compared to Swiss GmbH: Choosing the right structure

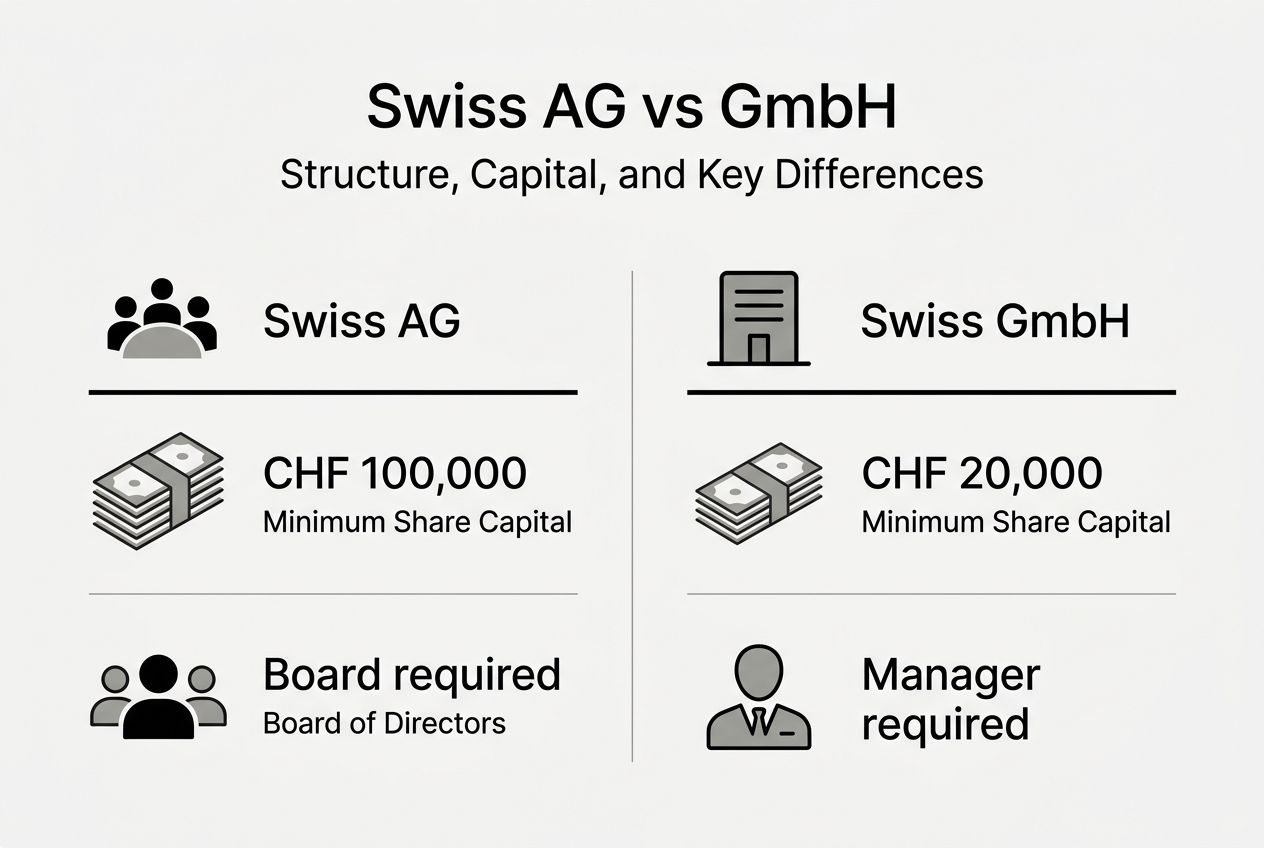

The Swiss GmbH vs AG capital comparison reveals the most obvious distinction: GmbH requires only CHF 20,000 minimum capital versus CHF 100,000 for AG. This fivefold difference significantly impacts initial formation costs and ongoing capitalization requirements. However, capital requirements represent just one factor in a complex decision affecting long-term business development, investor relations, and operational flexibility.

Choosing between a Swiss GmbH and a Swiss AG depends on your business size, goals, and preferences for control, transparency, and capital flexibility. The GmbH suits smaller businesses with stable ownership, limited expansion plans, and preference for tight control among known partners. The AG better serves companies anticipating external investment, planning eventual public listing, or requiring the credibility that comes with Switzerland’s premier corporate form.

Feature | Swiss AG | Swiss GmbH |

Minimum capital | CHF 100,000 | CHF 20,000 |

Initial payment | CHF 50,000 | CHF 20,000 (full amount) |

Ownership transfer | Freely transferable shares | Notarized transfer required |

Shareholder anonymity | Yes (with registration) | No (publicly listed) |

Typical use case | External investment, growth, IPO | Family business, professional services |

Investor perception | Highly credible, institutional grade | Suitable but less prestigious |

Liability protection functions identically in both structures, with shareholders risking only invested capital regardless of corporate form. Neither structure exposes personal assets to business creditors absent fraud or gross negligence. This parity means liability considerations should not drive the choice between AG and GmbH.

Corporate governance differs substantially in practice despite similar legal frameworks. GmbH vs AG key differences include shareholder meeting requirements, with GmbH often involving all owners in major decisions while AG boards operate more independently. GmbH shareholders typically know each other personally and participate actively in management, while AG shareholders may number in the hundreds or thousands with purely financial interest.

Market perception heavily favors AG for certain industries and transaction types:

Venture capital firms and institutional investors strongly prefer AG structures

International corporations typically establish Swiss subsidiaries as AGs

Banking relationships often develop more smoothly with AG status

Government procurement and major contracts may favor AG credibility

Pro Tip: If you are uncertain about future growth trajectory but want to preserve options for external investment, establish an AG initially despite higher costs, as converting from GmbH to AG later involves significant legal expenses, shareholder approvals, and potential tax consequences.

Share transfer mechanics create practical differences affecting business operations. AG shares transfer like any other property, through simple agreement and registration with the company. GmbH ownership interests require notarized transfer documents and commercial register updates, adding time and cost to ownership changes. This distinction matters enormously for businesses with active investor turnover or employee stock ownership plans.

Flexibility in share structure gives AG significant advantages for complex capitalization. Companies can issue preferred shares with enhanced dividends, non-voting shares for passive investors, or shares with transfer restrictions protecting strategic ownership. GmbH permits some variation but within narrower bounds, making sophisticated capital structures difficult. Technology startups using multiple funding rounds particularly benefit from AG flexibility in accommodating diverse investor preferences.

The AG structure also facilitates international expansion through recognized corporate form. Foreign regulators, partners, and customers immediately understand AG status as equivalent to corporation, plc, or SA in their jurisdictions. GmbH, while perfectly legitimate, requires explanation as an LLC equivalent, potentially slowing business development in unfamiliar markets.

Experience seamless Swiss company formation with RPCS

Navigating Swiss corporate law, cantonal variations, and administrative requirements challenges even experienced international entrepreneurs. RPCS specializes in Swiss company formation services that transform complex legal processes into straightforward, efficient experiences. Our team handles everything from initial structure consultation through commercial register filing, notarization, and bank account establishment, ensuring your Swiss AG launches properly from day one.

Beyond formation, we provide business and company address services giving your company a prestigious Swiss presence while maintaining compliance with residency requirements. Our comprehensive accounting services ensure ongoing regulatory compliance, proper financial reporting, and optimized tax positions across cantonal jurisdictions. Whether you are establishing your first Swiss entity or expanding existing international operations, RPCS delivers the local expertise and personalized service that makes Swiss business formation accessible and efficient.

FAQ

What is the minimum share capital for a Swiss AG?

The minimum required share capital is CHF 100,000, of which at least CHF 50,000 must be paid in at incorporation. You can contribute the initial payment in cash or through valued assets like intellectual property, equipment, or real estate. The remaining CHF 50,000 stays callable by the board as your business needs evolve, providing financial flexibility during growth phases.

Can shareholders remain anonymous in a Swiss AG?

Shareholders can remain anonymous; only the board of directors is publicly listed in Switzerland’s commercial register. While anti-money laundering rules require companies to maintain internal shareholder registers, this information remains confidential except during legal proceedings or regulatory investigations. Board members, by contrast, appear in public records to ensure governance transparency and accountability.

What corporate tax rates apply to Swiss AGs?

Corporate tax rates in Switzerland fell from 14.6% to 14.4% year over year, with Zug offering rates as low as 11.85%. The effective rate combines federal tax at 8.5% with cantonal and municipal taxes that vary significantly by location. Strategic canton selection can reduce your total tax burden by several percentage points, making location choice a critical financial decision for new Swiss AGs.

Who should choose a Swiss AG over a GmbH?

AG is suited for companies planning IPOs, requiring flexible shares, or aiming for strong investor appeal compared to GmbH. Businesses anticipating venture capital investment, international expansion, or eventual public listing benefit from AG structure and credibility. The GmbH works better for stable, closely held businesses with limited growth ambitions and preference for simpler governance among known partners.

Recommended

Comments