How to open a business bank account in Switzerland

- Mar 16

- 8 min read

Opening a Swiss business bank account as an international entrepreneur presents unique challenges. Strict anti-money laundering regulations, extensive documentation requirements, and complex verification processes can overwhelm even experienced business owners. Many foreign investors struggle to navigate the banking landscape without local expertise or clear guidance. This comprehensive guide walks you through every step of establishing your Swiss business bank account, from understanding regulatory requirements to selecting the right banking partner and successfully completing the application process.

Table of Contents

Understanding Swiss Banking Requirements For Business Accounts

Gathering Required Documents And Preparing Your Company For Banking

Selecting The Right Swiss Bank And Account Type For Your Business

Step-By-Step Process To Open Your Swiss Business Bank Account

How RPCS Solutions Can Help With Your Swiss Business Banking

Key takeaways

Point | Details |

Regulatory compliance is mandatory | Swiss business banking requires compliance with anti-money laundering laws and detailed documentation for foreign investors. |

Documentation preparation is critical | Comprehensive company and personal documents are essential to fulfill Swiss banks’ due diligence processes. |

Bank selection impacts your operations | Banks in Switzerland vary widely in their account features, fees, and suitability for international businesses. |

The process requires patience | The account opening process involves rigorous due diligence, often including in-person meetings and background checks. |

Understanding Swiss banking requirements for business accounts

Switzerland’s reputation as a global financial center comes with stringent regulatory oversight. Banks must comply with comprehensive anti-money laundering legislation that requires thorough verification of every business account holder. These regulations protect the integrity of the Swiss financial system but create additional hurdles for foreign entrepreneurs.

Your business activity must demonstrate transparency and legitimate purpose. Banks scrutinize the nature of your operations, revenue sources, and anticipated transaction volumes. They want clear answers about your business model, target markets, and why you specifically need Swiss banking services. Vague explanations or inconsistent information trigger red flags that can delay or derail your application.

Identification requirements extend beyond simple passport verification. Banks need certified copies of identification documents for all beneficial owners, directors, and authorized signatories. Anyone with 25% or more ownership typically qualifies as a beneficial owner requiring full documentation. Some institutions request proof of address dated within the last three months, tax identification numbers, and even curriculum vitae demonstrating business experience.

Non-residents face additional scrutiny compared to Swiss nationals. Banks assess whether your business has genuine economic substance in Switzerland or merely seeks the prestige of a Swiss address. You may need to demonstrate physical presence through office space, local employees, or concrete business operations within the country. Remote account opening exists but often requires working through specialized intermediaries who can vouch for your credentials.

Pro Tip: Establish your company structure and obtain all registration documents before approaching banks. A fully registered entity with clear ownership structure significantly improves your approval odds compared to applications submitted during the formation process.

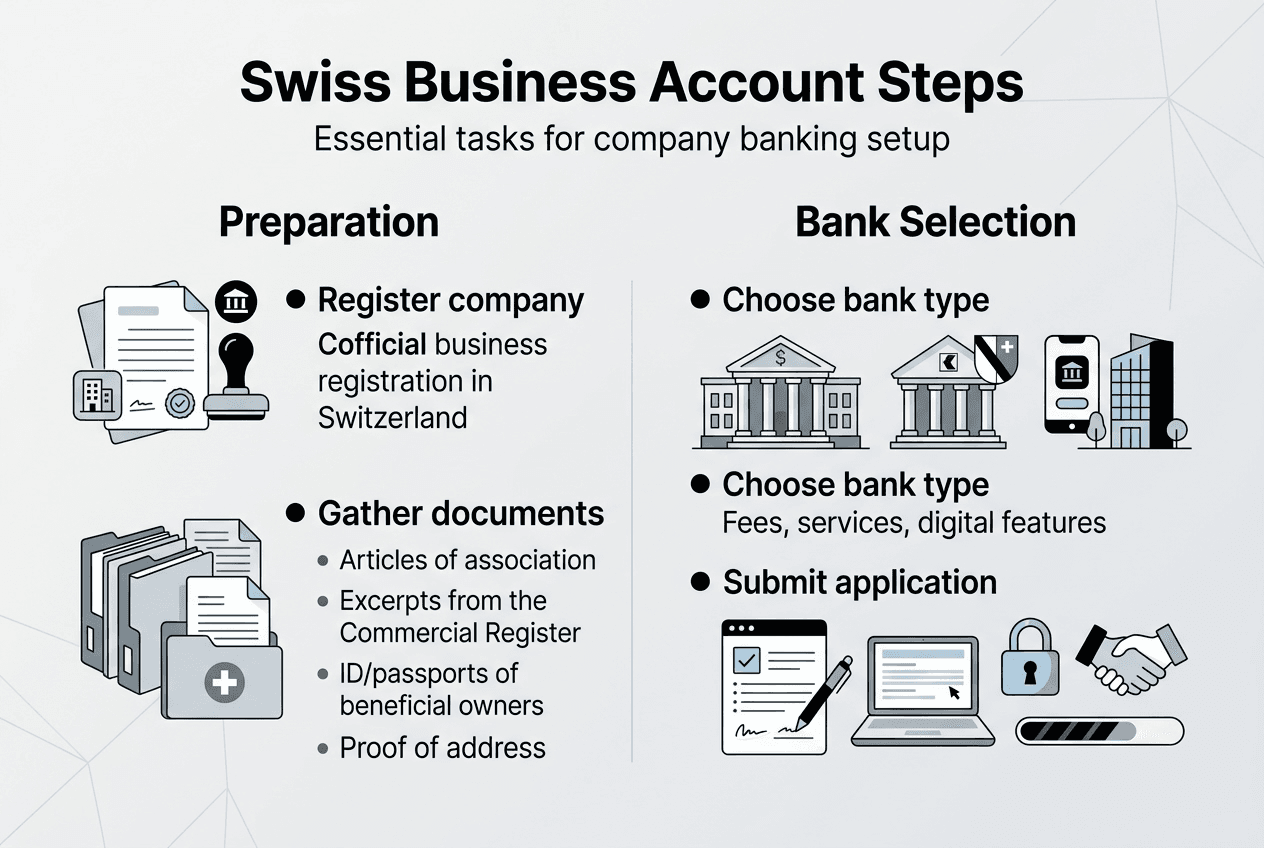

Gathering required documents and preparing your company for banking

Successful account opening hinges on meticulous document preparation. Start by collecting your company’s foundational papers. You need certified copies of your articles of incorporation, commercial register extract showing current registration status, and shareholder register listing all equity holders with their respective ownership percentages. These documents prove your company’s legal existence and ownership structure.

Personal identification extends across your entire ownership and management team. Each director, shareholder, and authorized signatory must provide a valid passport or national identity card. Banks require certified copies, not simple photocopies. Certification typically comes from notaries, lawyers, or official government agencies. Some banks accept apostilled documents for international recognition, particularly useful when dealing with foreign nationals.

Business planning documentation demonstrates commercial viability. Prepare a detailed business plan outlining your company’s activities, target markets, revenue projections, and operational strategy. Financial projections for the first two to three years show banks you have realistic expectations and sustainable business model. If your company already operates elsewhere, include recent financial statements, tax returns, and proof of existing banking relationships.

Document authenticity matters enormously. Banks reject applications with questionable or unverified paperwork. Original documents or properly certified copies prevent unnecessary delays. Organize everything systematically with clear labels and translations where necessary. Swiss banks operate in multiple languages, but English translations of foreign language documents facilitate faster processing.

Obtain certified commercial register extract dated within 30 days

Collect notarized identification for all beneficial owners and directors

Prepare comprehensive business plan with financial projections

Gather proof of business address and operational presence

Compile references from existing banks or professional advisors

Organize documents in clearly labeled folders for easy review

Pro Tip: Create a master checklist tracking every required document with collection dates and certification status. This systematic approach prevents last-minute scrambles and demonstrates professionalism to banking officers.

Document Category | Typical Requirements | Certification Level |

Company Formation | Articles of incorporation, commercial register extract, shareholder register | Notarized or apostilled |

Personal Identification | Passports, proof of address, tax ID numbers | Certified copies |

Business Operations | Business plan, financial projections, contracts | Original or certified |

Financial History | Bank statements, tax returns, audit reports | Bank-certified or official |

Selecting the right Swiss bank and account type for your business

Swiss banking options span from traditional private banks to modern fintech solutions. Private banks cater to high-net-worth clients and established corporations, offering personalized service and relationship banking. They typically require substantial minimum deposits, sometimes exceeding CHF 100,000, and charge premium fees. Retail banks like UBS, Credit Suisse, and PostFinance provide more accessible business accounts with lower entry barriers but less personalized attention.

Fintech providers have disrupted traditional banking with streamlined digital solutions. Companies like Neon, Yapeal, and Radicant offer business accounts with simplified opening processes and competitive fee structures. These platforms excel at international payments and multi-currency management but may lack the comprehensive services traditional banks provide. Consider whether you need investment advisory, trade finance, or complex treasury services when evaluating options.

Fee structures vary dramatically across institutions. Monthly maintenance fees range from zero for basic digital accounts to several hundred francs for premium private banking relationships. Transaction fees, foreign exchange spreads, and wire transfer charges add up quickly for internationally active businesses. Some banks waive fees if you maintain minimum balances or generate sufficient transaction volume. Calculate your anticipated banking activity and compare total cost of ownership across providers.

Account accessibility matters for international operations. Does the bank offer robust online banking platforms with multi-user access controls? Can you initiate international wire transfers without visiting a branch? Mobile banking capabilities, API integrations for accounting software, and real-time transaction notifications enhance operational efficiency. Foreign entrepreneurs particularly value banks with English-speaking support teams and experience serving international clients.

Traditional private banks: High minimums, premium services, relationship focus

Major retail banks: Moderate fees, broad services, established infrastructure

Cantonal banks: Regional focus, competitive rates, strong local presence

Fintech providers: Low fees, digital-first, streamlined processes

Specialized business banks: Industry expertise, tailored solutions, flexible terms

Bank Type | Minimum Deposit | Monthly Fees | Best For |

Private Banks | CHF 100,000+ | CHF 200-500 | High-value clients, complex needs |

Retail Banks | CHF 5,000-25,000 | CHF 30-100 | General business banking |

Fintech Solutions | CHF 0-5,000 | CHF 0-30 | Startups, digital operations |

Cantonal Banks | CHF 10,000-50,000 | CHF 40-120 | Local businesses, regional focus |

Step-by-step process to open your Swiss business bank account

Begin with preliminary research and initial contact. Most banks allow you to submit inquiry forms online or schedule introductory calls. Clearly explain your business nature, anticipated banking needs, and international connections. This conversation helps banks assess whether your profile fits their risk appetite and service capabilities. Some institutions immediately decline certain industries or business models, saving everyone time.

Submit your complete documentation package once you identify a suitable banking partner. Include every required document organized logically with a cover letter summarizing your application. Missing paperwork triggers requests for additional information that extend processing timelines. Banks typically acknowledge receipt within a few business days and assign your application to a relationship manager or compliance officer.

The compliance and risk assessment phase involves thorough background checks. Banks verify your company registration, screen beneficial owners against sanctions lists, and assess your business model’s legitimacy. They may request additional clarification about specific transactions, business relationships, or funding sources. Respond promptly and transparently to all inquiries. Evasive or incomplete answers raise suspicions that can terminate your application.

Most banks require face-to-face meetings or video verification sessions. Relationship managers want to meet key decision-makers, understand your business firsthand, and assess your credibility. Prepare to discuss your company’s operations, growth plans, and why you chose Switzerland for banking. Bring original identification documents for verification against certified copies. These meetings also let you ask questions about account features, fees, and ongoing requirements.

Account approval arrives after successful due diligence completion. Banks issue account numbers, online banking credentials, and initial funding instructions. You typically need to deposit the minimum required balance before full account activation. Some institutions place temporary restrictions on new accounts, limiting transaction volumes or requiring additional approvals for large transfers during the first few months.

Research banks matching your business profile and needs

Submit initial inquiry with business overview and documentation preview

Compile and submit complete application package with all required documents

Participate in compliance interviews and provide additional information as requested

Attend in-person or video verification meeting with bank officials

Receive account approval and complete initial funding requirements

Activate online banking and configure account features

Pro Tip: Schedule your bank meetings during Swiss business hours and dress professionally even for video calls. Swiss banking culture values formality and punctuality, and first impressions significantly influence relationship managers’ assessments.

“The key to successful Swiss bank account opening lies in preparation and transparency. Banks appreciate clients who understand requirements, provide complete documentation, and communicate openly about their business activities.” This approach builds trust and demonstrates the professionalism Swiss institutions expect.

How RPCS Solutions can help with your Swiss business banking

Navigating Swiss banking requirements becomes significantly easier with expert guidance. RPCS Solutions specializes in Swiss company formation services that include comprehensive banking support for international entrepreneurs. We handle document preparation, ensure compliance with all regulatory requirements, and leverage established banking relationships to facilitate introductions.

Our team understands what Swiss banks expect and how to present your business optimally. We assist with everything from initial company registration through successful account activation, including securing a business address in Switzerland that demonstrates local presence. This end-to-end support eliminates guesswork and accelerates your market entry.

Whether you need help opening your first Swiss account or expanding banking relationships for an existing operation, our expertise streamlines the process. We work with multiple banking partners across different tiers, matching you with institutions suited to your specific needs and profile. Let us help you open a Swiss bank account efficiently while you focus on building your business.

FAQ

Can non-residents open Swiss business bank accounts?

Yes, non-residents can successfully open Swiss business bank accounts, though they face more stringent documentation and due diligence requirements than Swiss nationals. Banks carefully evaluate the business purpose, economic substance in Switzerland, and legitimacy of operations. Working with knowledgeable service providers who understand banking expectations significantly speeds the process and improves approval rates.

What documents are essential for opening a Swiss business account?

Mandatory documents include certified articles of incorporation, current commercial register extract, complete shareholder register, and valid identification for all beneficial owners and directors. Banks also require detailed business plans, financial projections, and proof of business address. Notarized and apostilled copies expedite acceptance, particularly for international documents requiring cross-border recognition.

How long does the account opening process usually take?

Typically, the complete process takes four to eight weeks from initial application to full account activation, depending on documentation completeness and due diligence complexity. Applications with missing paperwork or unclear business models face longer timelines. Early preparation with all required documents and professional support can shorten processing time to as little as three weeks for straightforward cases.

Are there costs associated with opening and maintaining a Swiss business bank account?

Fees include initial account setup charges ranging from zero to several hundred francs, monthly maintenance fees, transaction charges, and sometimes minimum deposit requirements. Fee structures vary significantly between banks and account types, with private banks charging premium rates while fintech providers offer more economical options. Compare total cost of ownership including hidden fees like foreign exchange spreads and wire transfer charges when evaluating banking partners.

Recommended

Comments