Swiss company formation process 2026: Foreign investor guide

- Mar 14

- 10 min read

Many foreign investors believe forming a Swiss company is a simple, universally open process. However, sweeping legal changes in 2025 and 2026 have introduced strict transparency rules, foreign investment screening in critical sectors, and new tax reporting obligations that fundamentally reshape how international entrepreneurs establish GmbH and AG entities. These reforms target shell company abuse, enhance beneficial ownership tracking, and require government approval for certain takeovers. Understanding these updates is essential for compliance and successful market entry. This guide walks you through the complete formation process, legal requirements, tax considerations, and practical steps to launch your Swiss business in 2026.

Table of Contents

Key takeaways

Point | Details |

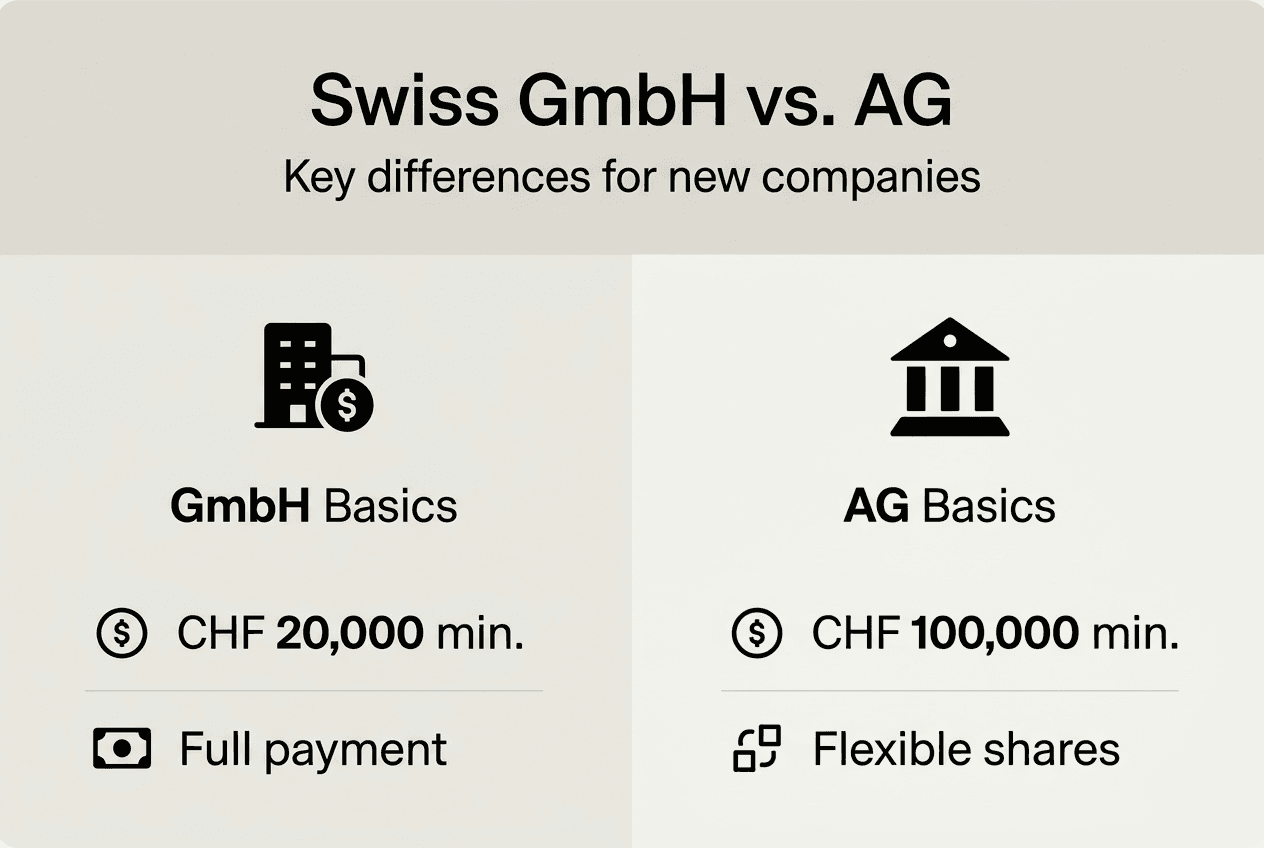

GmbH vs. AG structures | GmbH suits smaller ventures with CHF 20,000 capital; AG offers flexibility for larger, public fundraising with CHF 100,000 minimum. |

New transparency laws | Central beneficial owner database and shell company ban enforce stricter compliance from January 2025. |

Investment screening | Foreign takeovers in security-critical sectors now require formal SECO approval under the 2026 Investment Screening Act. |

Updated tax reporting | Minimum taxation rules and crypto asset reporting frameworks take effect in 2026, with exchange starting 2027. |

Overview of Swiss company structures: GmbH vs. AG

Choosing between a GmbH (Gesellschaft mit beschränkter Haftung) and an AG (Aktiengesellschaft) is the first critical decision for foreign investors entering Switzerland. Both structures provide limited liability, meaning shareholders risk only their contributed capital, not personal assets. However, they differ significantly in capital requirements, governance complexity, and suitability for different business models.

A GmbH setup requires a minimum share capital of CHF 20,000, fully paid at incorporation. This makes it attractive for startups, small to medium enterprises, and family businesses seeking cost-effective entry. GmbH shares are not freely transferable; any transfer requires notarized approval and often unanimous shareholder consent, ensuring tight control over ownership. Governance is simpler, with fewer mandatory reporting obligations compared to an AG. For a fast start with limited liability, a GmbH/Sàrl is the most common choice among foreign entrepreneurs prioritizing speed and simplicity.

An AG incorporation demands CHF 100,000 minimum capital, with at least CHF 50,000 paid in at formation. This structure suits larger ventures, companies planning public fundraising, or those seeking international credibility through stock issuance. AG shares are freely transferable unless the articles of association impose restrictions, facilitating investor entry and exit. Governance is more formal, requiring a board of directors, annual general meetings, and audited financial statements in many cases. The AG’s flexibility in share classes and public listing potential makes it ideal for scaling businesses and attracting institutional investors.

Pro Tip: If you anticipate frequent ownership changes or plan to raise venture capital, an AG offers smoother share transfer mechanisms and greater investor appeal than a GmbH.

Feature | GmbH | AG |

Minimum capital | CHF 20,000 (fully paid) | CHF 100,000 (CHF 50,000 paid) |

Share transferability | Restricted, requires notarization | Freely transferable |

Governance complexity | Lower, simpler reporting | Higher, formal board and audits |

Typical use case | SMEs, family businesses | Large firms, public fundraising |

Both structures offer Swiss legal forms with distinct advantages. Your choice depends on capital availability, growth plans, and desired ownership flexibility. Understanding these differences ensures you select the optimal legal form for your business goals and investor profile.

Legal compliance and recent reforms affecting company formation

Switzerland’s legal landscape for company formation has undergone significant transformation since early 2025, directly impacting foreign investors. These reforms address transparency gaps, prevent corporate abuse, and introduce national security safeguards for critical sectors. Navigating these changes is mandatory for lawful incorporation and ongoing operations.

The Investment Screening Act, adopted in December 2025, introduces a legal instrument for reviewing domestic company takeovers by foreign investors, particularly in security-critical sectors. Under this law, foreign entities acquiring Swiss companies operating in infrastructure, technology, or defense must obtain approval from the State Secretariat for Economic Affairs (SECO) before completing the transaction. This measure aims to protect Swiss economic sovereignty and prevent hostile takeovers that could compromise national security. If your investment targets sectors like energy, telecommunications, or advanced manufacturing, expect rigorous due diligence and potential delays while SECO evaluates strategic risks.

Transparency improvements represent another major shift. Effective January 1, 2025, Switzerland launched a central beneficial owner database accessible to authorities, enhancing anti-money laundering enforcement. All companies must register ultimate beneficial owners holding 25% or more equity or control. This database closes loopholes that previously allowed anonymous ownership structures. Foreign investors must now disclose their identity and ownership stakes transparently, eliminating the appeal of Swiss entities as vehicles for concealing wealth.

New provisions in Swiss company law, effective January 1, 2025, aim to prevent bankruptcy abuses and shell company transactions. The reforms explicitly ban shell companies, defined as entities lacking genuine business activity, from participating in mergers, demergers, or transformations. This prevents insolvent firms from using corporate restructuring to evade creditor claims. Additionally, the law prohibits retroactive opting out of liability, closing a loophole where companies could retrospectively shield themselves from obligations. These rules ensure that only operationally legitimate businesses enjoy the benefits of Swiss corporate flexibility.

Distinguishing shell companies from shelf companies is crucial. A shell company has no real operations, assets, or employees, existing only on paper. A shelf company is a pre-registered, dormant entity available for purchase, which becomes active once a buyer injects capital and begins operations. Shelf companies remain legal if used for legitimate business purposes, while shell companies designed to obscure ownership or evade taxes are now explicitly prohibited.

Key compliance actions for foreign investors:

Verify that your planned Swiss entity will conduct genuine business activity with real assets and employees.

Register beneficial owners in the central database within statutory deadlines.

If acquiring a Swiss company in a critical sector, initiate SECO screening early to avoid transaction delays.

Consult Swiss corporate law updates to ensure your structure aligns with 2026 standards.

Understand that choosing a GmbH structure or AG must reflect operational substance, not just tax optimization.

These reforms signal Switzerland’s commitment to maintaining its reputation as a transparent, stable jurisdiction while deterring misuse. Foreign investors who embrace these standards will find Switzerland remains highly attractive, but those seeking opacity or minimal substance face significant legal barriers.

Swiss tax considerations and operational setup for foreign investors

Tax compliance is a cornerstone of Swiss company formation, and recent regulatory updates demand careful attention from foreign investors. The 2026 tax landscape includes new minimum taxation rules for multinational groups, extended reporting for crypto assets, and operational risk guidance for digital asset custody. Understanding these requirements ensures your Swiss entity meets obligations from day one.

Amendments to the Ordinance on Minimum Taxation of Large Corporate Groups (MindStV) came into force on January 1, 2026, implementing international reporting requirements (GloBE Declaration) and information exchange. This regulation enforces the OECD’s Pillar Two framework, imposing a 15% minimum effective tax rate on multinational enterprises with consolidated revenues exceeding EUR 750 million. If your Swiss company is part of a global group meeting this threshold, you must file a GloBE Declaration detailing tax calculations and jurisdictional allocations. Even if your group currently falls below the threshold, monitor revenue growth, as crossing it triggers immediate compliance obligations.

Amendments to the ordinance on the International Automatic Exchange of Information in Tax Matters (AIAG) extended the reporting framework to crypto assets on January 1, 2026. Financial institutions and crypto service providers must now collect and report information on crypto asset holdings and transactions for clients. However, actual information exchange with foreign tax authorities will commence in 2027, giving firms a transition period to implement systems. If your Swiss company deals in cryptocurrencies or holds digital assets, ensure your accounting infrastructure can track and report these holdings accurately.

Operational risk management for crypto custody received formal guidance when FINMA published Guidance 01/2026 Custody of crypto based assets on January 12, 2026. This document clarifies operational and security standards for institutions offering crypto custody services, addressing key management, cold storage protocols, and disaster recovery. If your business model includes holding client crypto assets, compliance with FINMA’s guidance is non-negotiable to maintain regulatory standing.

Practical tax and operational steps for newly formed companies:

Determine if your group meets the EUR 750 million threshold for minimum taxation and prepare GloBE reporting infrastructure.

Register for VAT if your annual turnover exceeds CHF 100,000, ensuring timely quarterly filings.

Enroll in mandatory social insurance schemes (AHV/IV/EO) for all Swiss-based employees within 30 days of hiring.

Establish a Swiss business bank account to deposit share capital and manage operational cash flows.

Implement accounting systems compliant with Swiss GAAP or IFRS, depending on company size and sector.

If handling crypto assets, integrate tracking and reporting tools to meet AIAG requirements by 2027.

Pro Tip: Engage a Swiss tax advisor before incorporation to structure your entity optimally for cantonal and federal tax efficiency, as rates vary significantly across Switzerland’s 26 cantons.

Tax Obligation | Deadline | Applicable Threshold |

GloBE Declaration | Annual, within filing period | Groups > EUR 750M revenue |

VAT Registration | Within 30 days of threshold | > CHF 100,000 turnover |

Corporate Tax Return | Cantonal deadlines vary | All entities with profit |

Crypto Asset Reporting | Annual (exchange starts 2027) | All crypto holdings |

Navigating these tax obligations requires diligence and often professional support. The Swiss company formation checklist and document preparation guide provide structured frameworks to ensure you address every compliance requirement systematically.

Step-by-step guide to the Swiss company formation process

Forming a Swiss GmbH or AG involves a clear sequence of legal, administrative, and financial steps. While the process is well-defined, foreign investors must pay close attention to documentation, notarization, and post-registration formalities to avoid delays or rejections.

1. Preliminary planning and business plan preparation

Define your business model, target market, and operational structure. Draft a comprehensive business plan outlining revenue projections, staffing needs, and capital allocation. Decide between GmbH and AG based on capital availability and growth ambitions. Select a unique company name and verify its availability through the Swiss Commercial Register online database. Choose a registered office address in Switzerland; if you lack a physical presence, consider a business address service to meet legal requirements.

2. Draft articles of association and shareholder agreements

Prepare the articles of association (statutes) defining company purpose, share capital, shareholder rights, and governance structure. For a GmbH, specify share transfer restrictions and voting rights. For an AG, detail share classes, par values, and any transfer limitations. If multiple shareholders exist, draft a shareholder agreement covering decision-making, profit distribution, and dispute resolution. These documents must comply with Swiss Code of Obligations standards and are subject to notarial review.

3. Notarization of incorporation documents

Schedule a notarization appointment with a Swiss notary public. All founding shareholders (or their authorized representatives) must attend in person or via authenticated power of attorney. The notary verifies identities, reviews the articles of association for legal compliance, and certifies the incorporation deed. This step is mandatory and cannot be bypassed. Notary fees typically range from CHF 1,000 to CHF 2,500, depending on company complexity and canton.

4. Deposit share capital in a Swiss bank account

Open a capital deposit account (Kapitaleinzahlungskonto) at a Swiss bank. Transfer the minimum required capital: CHF 20,000 for a GmbH (fully paid) or at least CHF 50,000 for an AG. The bank issues a confirmation letter (Kapitaleinzahlungsbestätigung) certifying the deposit, which the notary requires for registration. Note that opening a Swiss bank account as a foreign entity can take several weeks due to due diligence requirements, so initiate this process early.

5. Register with the Commercial Register

Submit the notarized incorporation documents, bank capital confirmation, and identification documents for all directors and shareholders to the cantonal Commercial Register. The registry reviews the application for completeness and legal compliance. Upon approval, your company receives a unique identification number (UID) and is officially entered into the public register. Registration typically takes 5 to 10 business days. Once registered, your company gains legal personality and can commence operations.

6. Post-registration formalities

Register for VAT with the Federal Tax Administration if your turnover will exceed CHF 100,000 annually. Enroll in mandatory social insurance schemes for employees. Obtain any sector-specific licenses or permits required for your business activity. Open a standard business bank account to replace the capital deposit account, transferring the deposited capital. Implement bookkeeping systems and appoint an auditor if your company meets statutory audit thresholds.

Following these steps systematically ensures a smooth formation process. The GmbH setup steps and AG incorporation process guides provide additional detail and jurisdiction-specific nuances to support your planning.

Discover professional Swiss company formation services

Navigating Swiss company formation, especially with the 2026 legal and tax reforms, demands expertise and local knowledge. Professional company formation services streamline the entire process, from drafting articles of association to completing Commercial Register filings. Experienced providers handle notarization coordination, ensure compliance with transparency and investment screening rules, and manage interactions with cantonal authorities.

Beyond incorporation, establishing operational infrastructure is critical. Securing a business address in Switzerland satisfies legal domicile requirements and enhances credibility with clients and partners. Opening a Swiss bank account remains challenging for foreign entities, but specialized support accelerates approval by preparing compliant documentation and liaising with banking compliance teams. Ongoing accounting, tax filing, and payroll administration ensure your Swiss entity remains in good standing with authorities. Leveraging professional services allows you to focus on business growth while experts handle regulatory complexity and administrative burdens.

What is the minimum capital required to start a Swiss GmbH?

The minimum share capital for a GmbH is CHF 20,000, which must be fully paid up at incorporation. This capital ensures limited liability protection for shareholders and must be deposited in a Swiss bank account before registration. Unlike an AG, no partial payment option exists for a GmbH.

How does the new Investment Screening Act affect foreign investors in Switzerland?

Foreign takeovers in security-critical sectors need formal government approval under the Investment Screening Act. SECO reviews proposed acquisitions to assess risks to national security and economic sovereignty. This measure aims to protect Swiss interests in infrastructure, technology, and defense sectors. Investors should initiate screening early to avoid transaction delays.

When will crypto asset reporting start under Swiss tax regulations?

The extended crypto reporting framework was announced effective 2026 under AIAG amendments. However, actual information exchange with foreign tax authorities will start in 2027. Financial institutions and crypto service providers must implement tracking systems now to meet future reporting obligations. Companies holding or transacting crypto assets should prepare compliance infrastructure immediately.

Can I use a shelf company to start my Swiss business?

Yes, purchasing a shelf company is legal if you inject capital and conduct genuine business activity. Shelf companies are pre-registered, dormant entities available for quick activation. However, shell companies with no real operations are now banned under 2025 reforms. Ensure your entity has substantive business purpose, assets, and employees to comply with transparency rules.

What are the main differences between GmbH and AG governance?

A GmbH has simpler governance with fewer mandatory reporting requirements and restricted share transferability. An AG requires a formal board of directors, annual general meetings, and often statutory audits. AG shares are freely transferable unless restricted by articles of association, making it suitable for larger ventures and public fundraising. Choose based on your growth plans and desired ownership flexibility.

How long does Swiss company formation typically take?

The formation process typically takes 4 to 6 weeks from initial planning to Commercial Register approval. Notarization and capital deposit can be completed within 1 to 2 weeks. Commercial Register review takes 5 to 10 business days. Delays often occur during bank account opening due to due diligence requirements, so initiate banking early. Professional services can expedite timelines by managing documentation and coordination efficiently.

Recommended

Comments