Swiss Payroll Services Explained: Compliance & Efficiency 2026

- Apr 2

- 8 min read

Swiss payroll is one of the most underestimated operational challenges for foreign business owners. Many entrepreneurs assume that setting up a Swiss company is the hard part, then discover that managing payroll correctly is a separate, ongoing legal obligation with real financial consequences. Switzerland’s payroll system involves multiple mandatory deductions, age-dependent pension rates, and annual regulatory updates that generic global payroll tools simply cannot handle. Get it wrong and you face audits, back payments, and fines. This guide breaks down every layer of Swiss payroll, from basic deductions to employer budgeting, compliance checklists, and practical tips that help you run a clean, efficient operation from day one.

Table of Contents

Key Takeaways

Point | Details |

Payroll complexity in Switzerland | Swiss payroll requires careful calculation of mandatory social contributions and pension obligations. |

Employer costs and risks | Employers face substantial costs beyond salaries and need robust compliance to avoid penalties. |

Stepwise compliance approach | Using checklists and professional services ensures compliance and efficient Swiss payroll management. |

Local expertise is essential | Foreign businesses succeed when they leverage experienced Swiss payroll providers for setup and ongoing operations. |

Understanding the basics of Swiss payroll

Swiss payroll is not just about calculating a salary and transferring money. It is a structured legal process that requires you to account for multiple mandatory deductions before an employee receives a single franc. Understanding the difference between gross and net salary is your starting point.

Gross salary is the total agreed compensation. Net salary is what the employee actually receives after all statutory deductions. The gap between these two numbers surprises most foreign employers when they see it for the first time.

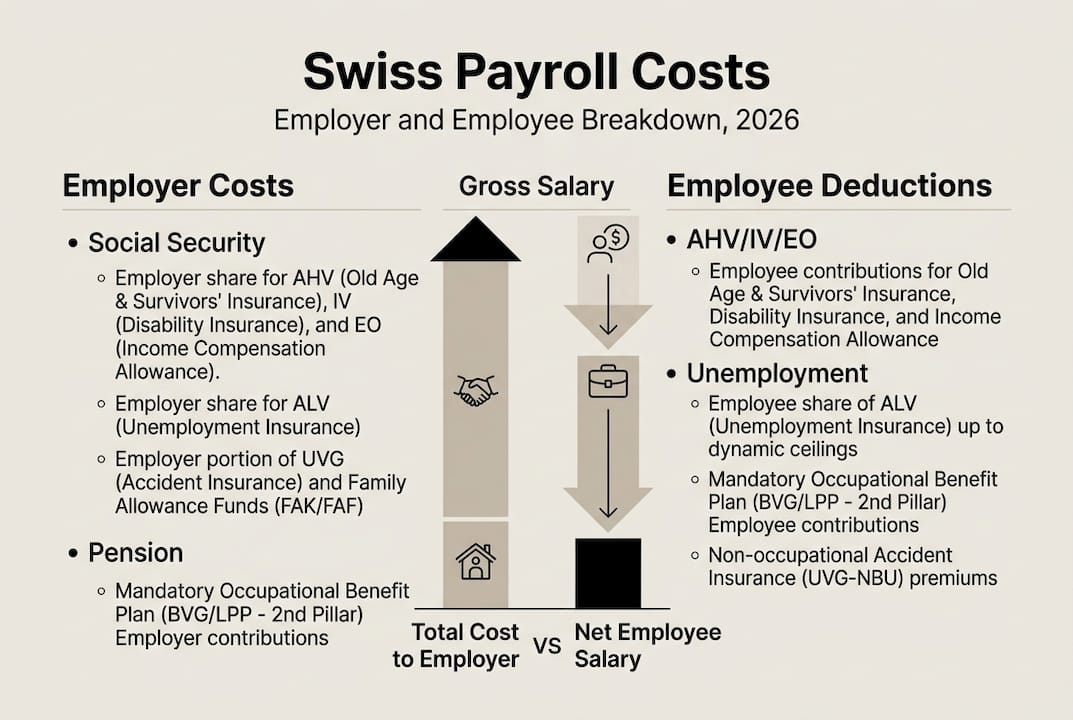

The mandatory deductions that every Swiss employer must process fall into three main categories:

AHV/IV/EO (Pillar 1 social security): This covers old-age insurance (AHV), disability insurance (IV), and income compensation (EO). The social security contributions 2026 confirm a combined rate of 10.6%, split equally between employer and employee at 5.3% each.

ALV (unemployment insurance): Applies at 2.2% of salary up to CHF 148,200 annually, with each party paying 1.1%.

BVG (Pillar 2 occupational pension): Contributions depend on the employee’s age bracket and are calculated on the coordinated salary.

Additional withholdings: These include accident insurance (SUVA or private), daily sickness allowance insurance, and for foreign employees, withholding tax at source.

The AHV/IV/EO rate of 10.6% split equally means both you and your employee each contribute 5.3% of gross salary to Pillar 1 alone. That is before pension and insurance are added.

“Accurate payroll is not optional in Switzerland. It is a legal obligation that protects both employer and employee, and errors are treated as compliance failures, not administrative oversights.”

Understanding Swiss accounting requirements alongside payroll obligations ensures you do not treat these two functions as separate silos. They are deeply connected in Swiss corporate governance.

Social security and pension obligations step-by-step

With the basics clear, let’s walk step-by-step through the major payroll obligations you must cover as an employer.

Here is a structured breakdown of how to calculate payroll deductions for a single employee:

Determine gross salary. Start with the agreed annual or monthly gross figure.

Calculate AHV/IV/EO. Multiply gross salary by 5.3% for the employee share. Match it with your 5.3% employer contribution.

Calculate ALV. Apply 1.1% to gross salary up to CHF 148,200. Both parties pay 1.1%.

Identify coordinated salary for BVG. Subtract the entry threshold (CHF 22,680) from gross salary, capped at CHF 90,720. This is the base for Pillar 2 contributions.

Apply the age-dependent BVG rate. Rates range from 7% to 18% depending on the employee’s age bracket.

Add accident and sickness insurance. Non-occupational accident insurance (NBUV) is typically employee-paid; occupational accident insurance (BUV) is employer-paid.

The Pillar 2 BVG pension rates are age-dependent, with the employer required to fund at least 50% of the total contribution.

Age bracket | BVG contribution rate |

25 to 34 | 7% |

35 to 44 | 10% |

45 to 54 | 15% |

55 to 65 | 18% |

Real-world example: An employee aged 40 earns CHF 80,000 gross. Coordinated salary = CHF 80,000 minus CHF 22,680 = CHF 57,320. BVG at 10% = CHF 5,732 total. You as employer pay at least CHF 2,866.

Pro Tip: Always verify your employee’s birth year before setting up payroll. A one-year age bracket difference can shift BVG contributions significantly, and retroactive corrections are time-consuming.

Reviewing your Swiss company compliance steps early helps you align payroll setup with your broader legal obligations. Also, getting Swiss tax registration right from the start prevents overlap errors between withholding tax and social security filings.

Hidden costs and employer budgeting in Swiss payroll

Now that you understand the core obligations, let’s examine what these mean for your company budget and where hidden costs often surface.

Most foreign employers focus on the employee’s deductions when reviewing payroll. The bigger shock is usually the employer-side costs. Here is what you are actually paying on top of the agreed gross salary:

Matching AHV/IV/EO: 5.3% of gross salary

Matching ALV: 1.1% up to the CHF 148,200 threshold

BVG employer share: Minimum 50% of the applicable BVG rate

Occupational accident insurance (BUV): Employer-paid, typically 0.1 to 0.3% of salary

Family allowance contributions (Familienzulagen): Varies by canton, typically CHF 200 to CHF 400 per child per month

Administration and payroll processing fees: Often overlooked in early budgeting

Key benchmark: Employee deductions typically run 15 to 25% of gross salary, while employer-side costs add another 13 to 41% on top of gross, depending on age, canton, and insurance choices.

To make this concrete, consider a sample employee earning CHF 100,000 gross annually. Employee deductions might total CHF 18,000 to CHF 22,000. Your employer contributions could add CHF 15,000 to CHF 35,000 on top of the gross. The real cost of that CHF 100,000 employee is often CHF 115,000 to CHF 135,000 or more.

Cost component | Switzerland | Germany | UK |

Employer social security | ~13 to 20% | ~20% | ~13.8% |

Mandatory pension (employer) | ~3.5 to 9% | Included above | 3% minimum |

Accident insurance | ~0.1 to 0.3% | Included | Not separate |

Family allowances | Canton-dependent | Employer-funded | State-funded |

Switzerland’s system is not necessarily more expensive than Germany’s, but it is more fragmented and canton-specific, which creates more opportunities for budgeting errors.

Managing these costs well requires solid bookkeeping. Reviewing Swiss accounting for global firms and understanding the Swiss accounting setup workflow will help you integrate payroll costs into your financial reporting accurately.

Ensuring payroll compliance and avoiding common mistakes

Understanding the financial implications is only part of the story. Compliance is just as crucial to business success in Switzerland.

The most common payroll mistakes foreign employers make are not dramatic errors. They are small, consistent oversights that compound over time. Here are the most frequent compliance risks:

Inaccurate wage records: Swiss law requires detailed payroll records for every employee. Missing entries or inconsistent figures are an immediate red flag during audits.

Wrong deduction rates: Rates change annually. Using last year’s AHV or BVG rates is a common error that creates underpayment.

Late filings: AHV contributions must be reported and paid monthly or quarterly depending on company size. Late payments trigger interest charges.

Incorrect withholding tax: Foreign employees subject to tax at source require separate calculation logic. Errors here create personal tax liability for your employees.

Missing Pillar 2 enrollment: Every employee earning above CHF 22,680 must be enrolled in a BVG pension fund. Failure to enroll is a serious compliance breach.

Here is a practical compliance checklist to run every payroll cycle:

Confirm current AHV/ALV rates for 2026

Verify each employee’s BVG age bracket and coordinated salary

Check canton-specific family allowance rates

Confirm withholding tax status for all foreign employees

File and pay AHV contributions on time

Retain all payroll records for at least 10 years

“Matching contributions and mandatory insurances are frequent audit points. Swiss authorities cross-reference employer filings against employee tax declarations, making discrepancies easy to detect.”

Pro Tip: Schedule a quarterly payroll review with your accountant or payroll provider. Annual reviews are too infrequent given how often Swiss rates and thresholds shift.

Keeping up with annual administration for compliance is not optional. It is the backbone of staying legally operational in Switzerland.

The uncomfortable truth about Swiss payroll for foreign businesses

Here is something most guides will not tell you directly. The biggest payroll failures we see from foreign-owned Swiss companies are not caused by ignorance. They are caused by overconfidence.

Smart entrepreneurs who have successfully run payroll in Germany, the US, or the UK assume the logic transfers. It does not. Switzerland has 26 cantons, each with its own family allowance rules, and the federal government updates AHV, ALV, and BVG thresholds every single year. A global payroll platform that handles 50 countries will almost always lag behind on canton-specific Swiss updates.

We have seen companies use automated tools that were 18 months behind on BVG coordination thresholds. The resulting underpayments triggered retroactive corrections, interest charges, and an audit. The cost of fixing it was five times what local expert support would have cost upfront.

The lesson is not that technology is bad. It is that Swiss payroll requires local, current expertise, not generic automation. Understanding Swiss branch setup insights early in the process helps you build the right payroll infrastructure before you hire your first employee, not after.

Get expert Swiss payroll solutions for your business

If you’re ready to make Swiss payroll work seamlessly for your business, here’s how RPCS can help.

Managing Swiss payroll correctly requires more than a spreadsheet. It demands current knowledge of federal and cantonal rules, precise deduction calculations, and timely filings across multiple authorities.

RPCS provides company formation support alongside fully managed payroll services designed specifically for foreign-owned Swiss entities. Our team handles everything from AHV enrollment to monthly filings, so you stay compliant without the administrative burden. Our Swiss accounting experts integrate payroll with your broader financial reporting for a clean, audit-ready setup. Explore our custom payroll packages to find the right level of support for your business size and structure. Contact us today for a consultation.

Frequently asked questions

What are the main payroll deductions in Switzerland?

The main deductions are AHV/IV/EO at 10.6% total, unemployment insurance (ALV) at 2.2%, occupational pension (Pillar 2 BVG), and accident and sickness insurance premiums. Each is calculated separately and applies to different salary bases.

How much do Swiss employers pay for social security and pension?

Employers match employee social security contributions and must cover at least 50% of Pillar 2 pension costs. Overall, employer-side costs add 13 to 41% on top of gross salary depending on age, canton, and insurance structure.

What happens if payroll compliance is not maintained in Switzerland?

Non-compliance triggers penalties, interest charges on late payments, and formal audits. Matching contributions and insurance are among the first items authorities review, and discrepancies can result in back payments and loss of good standing.

Is it mandatory to engage a payroll provider for a Swiss company?

There is no legal requirement to use a payroll provider, but most foreign-owned Swiss companies do so because the canton-specific rules and annual rate changes make in-house management genuinely risky without local expertise.

What is ‘coordinated salary’ in Swiss Pillar 2 pension?

Coordinated salary is the portion of gross salary between CHF 22,680 and CHF 90,720 used as the calculation base for BVG pension contributions. Salary below or above these thresholds is excluded from the standard Pillar 2 calculation.

Recommended

Comments