Guide to Swiss business administration for global entrepreneurs

- 1 day ago

- 8 min read

TL;DR:

Switzerland offers a stable currency, advanced banking, and favorable taxes, but strict compliance is also necessary. Entrepreneurs must carefully choose legal structures, monitor VAT thresholds in real time, and optimize canton-level tax rates for long-term benefits. Ongoing proactive management, including accurate record keeping and local representation, is essential for legal compliance and business growth in Switzerland.

Switzerland surprises most international entrepreneurs the moment they move past the brochure version of the country. The stable currency, world-class banking, and favorable tax environment are real. So are the strict compliance deadlines, layered tax obligations, and governance requirements that most founders discover only after they have already incorporated. This guide to Swiss business administration covers what actually matters: the legal structure choices, VAT thresholds that trigger faster than expected, canton-level tax differences worth tens of thousands of francs annually, and the ongoing administrative calendar that keeps your company legally sound.

Table of Contents

Key Takeaways

Point | Details |

Mandatory VAT registration | You must register for VAT within 30 days after exceeding CHF 100,000 annual turnover in Switzerland. |

Tax varies by canton | Swiss corporate tax rates differ widely between cantons, affecting overall business tax burden. |

Ongoing compliance required | Swiss company administration is a continuous process involving records, tax filings, and governance. |

Swiss resident director needed | At least one director must reside in Switzerland to meet legal governance requirements. |

Professional support advantage | Partnering with local experts simplifies compliance and optimizes Swiss business operations. |

Understanding the Swiss company formation process

Getting your company formation right in Switzerland is not just a paperwork exercise. It is the foundation every subsequent legal and financial decision rests on. Two entity types dominate the landscape for foreign investors: the GmbH (Gesellschaft mit beschränkter Haftung, the Swiss equivalent of a limited liability company) and the AG (Aktiengesellschaft, a share corporation).

The key differences are practical. A GmbH requires a minimum share capital of CHF 20,000, fully paid up at incorporation. An AG requires CHF 100,000, with at least CHF 50,000 paid up at founding. The GmbH lists shareholders publicly in the commercial register, which matters for confidentiality-focused founders. The AG issues shares that can be transferred privately without updating the register, making it the preferred structure for equity-heavy businesses or those planning future investment rounds.

Both structures require:

Drafting articles of association and having them notarized

Depositing share capital in a Swiss bank account before registration

Registering with the relevant cantonal commercial register

Establishing a Swiss registered business address

Appointing at least one Swiss resident director or using a nominee director service

That last point trips up many international entrepreneurs. Swiss law requires local legal representation, and ignoring it delays registration or creates compliance gaps from day one. Reviewing a company formation checklist before starting saves significant time. If you are leaning toward the GmbH structure, the practical steps for setting up a Swiss GmbH differ enough from an AG that they deserve separate attention. Make sure you also understand the key documents for registration specific to your chosen entity type, as missing even one notarized document restarts the clock.

Navigating Swiss VAT registration and compliance

Here is where many foreign founders get caught. VAT in Switzerland does not work on a calendar-year lag like in some other jurisdictions. VAT registration becomes mandatory when annual turnover exceeds CHF 100,000, and once you cross that threshold you must register with the Swiss Federal Tax Administration within 30 days. Not 90 days. Not at year-end. Thirty days from the moment you exceed it.

This means your accounting must track turnover in real time, not quarterly. A company that invoices CHF 110,000 in its first year and fails to monitor this faces retroactive VAT liability plus penalties.

Key VAT compliance points to understand:

The CHF 100,000 threshold applies to worldwide turnover, not just Swiss revenue in many cases

Voluntary registration below the threshold is possible and can benefit companies with significant input VAT to reclaim

VAT returns are typically filed quarterly, though high-turnover companies may face more frequent obligations

Swiss VAT rates are 8.1% standard, 3.8% for accommodation, and 2.6% for essential goods

Accurate categorization of every sale and expense from day one is not optional, it determines your threshold calculation

“Businesses that wait until year-end to assess their VAT position often find themselves registering late, correcting historical invoices, and absorbing avoidable interest charges.” This is a pattern our team sees repeatedly with newly incorporated companies.

Pro Tip: Build your accounting system before your first invoice, not after. The way you categorize your first ten transactions sets the methodology your VAT returns will depend on for years.

For a detailed walkthrough of the registration process and documentation, the Swiss VAT registration guide covers each step clearly.

Optimizing Swiss corporate tax with canton selection

Switzerland’s corporate tax system is one of the most misunderstood in Europe. It looks simple until you realize it has three layers operating simultaneously. The Swiss corporate tax structure breaks down as follows: a federal corporate profit tax of 8.5% (nominal), plus cantonal tax, plus communal tax. The combined effective rate is what actually hits your bottom line, and it varies dramatically depending on where you incorporate.

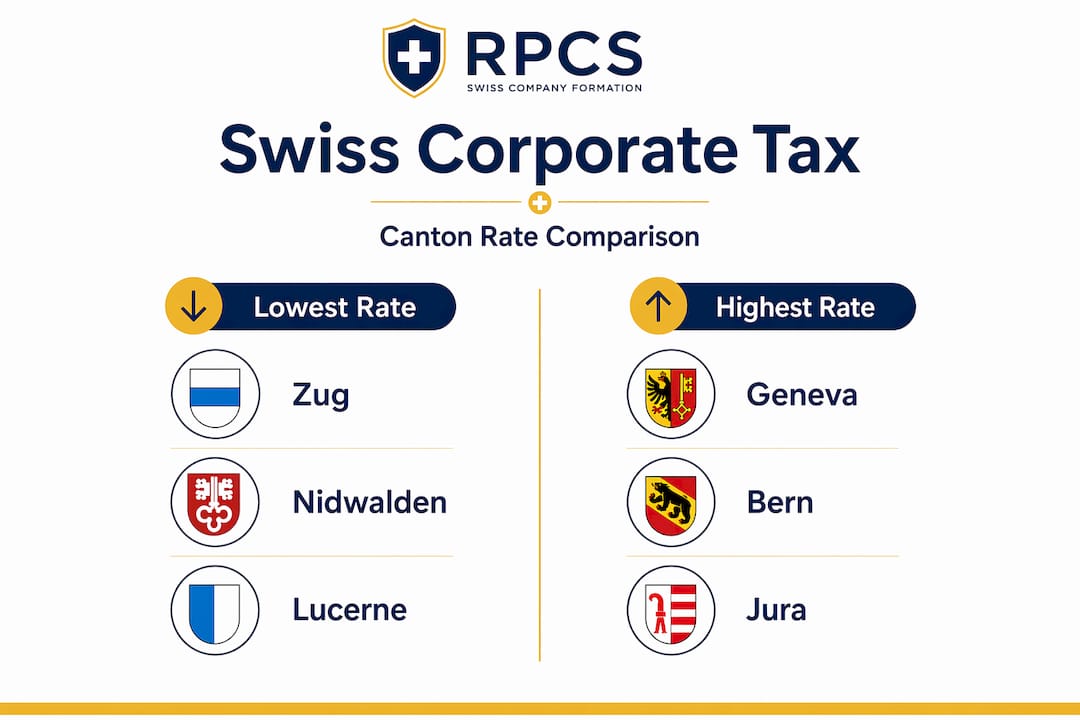

Canton | Effective corporate tax rate (2026) |

Zug | ~11.85% |

Nidwalden | ~11.97% |

Lucerne | ~12.32% |

Geneva | ~13.99% |

Zurich | ~19.70% |

Bern | ~20.54% |

For a company generating CHF 500,000 in annual profit, the difference between incorporating in Zug versus Bern is roughly CHF 43,000 per year. That is not a rounding error. It is a meaningful cash flow decision that compounds over time.

Additional tax planning tools available in Switzerland include:

Patent boxes: Reduce tax on income from qualifying intellectual property, available in most cantons

R&D super-deductions: Some cantons allow deductions above 100% for qualifying research expenditure

Notional interest deduction: Available in a few cantons for equity-financed companies

GmbH and AG structures receive identical tax treatment at the federal and cantonal levels, so your entity choice does not change your tax rate. What it does affect is administrative simplicity and the way profits flow to shareholders. For a deeper look at geographic advantages, the guide on tax benefits by canton is worth your time. Pair it with the Swiss tax optimization guide to understand how tools like patent boxes actually apply in practice.

Pro Tip: Choose your canton before you open your bank account. Changing your registered address after incorporation is legally possible but administratively complex and sometimes triggers new cantonal tax assessments.

Ongoing Swiss company administration and compliance essentials

Incorporation is a single event. Swiss business administration is everything that happens afterward, indefinitely. Swiss company administration is best treated as an ongoing control system rather than one-off filings: you need reliable document retention, repeatable accounting closes, and a coordinated calendar for filings and updates.

Your annual compliance calendar must cover:

Annual general meeting (AGM): Required by Swiss law, typically within six months of the financial year end

Corporate tax returns: Filed annually at both federal and cantonal levels, deadlines vary by canton

VAT returns: Quarterly or semi-annually depending on your turnover volume

Commercial register updates: Any change in directors, registered address, or share capital must be reported promptly

Financial statements: Must be prepared in accordance with Swiss accounting standards and approved at the AGM

Beyond the calendar, ongoing compliance means building internal controls that catch issues before regulators do.

Essential practices for maintaining compliance:

Retain all business documents, contracts, and accounting records for a minimum of 10 years

Conduct quarterly internal reviews of VAT positions and expense categorizations

Audit your commercial register entry at least annually for accuracy

Document board decisions formally, even for small companies without external shareholders

Review data protection practices under the nFADP (the revised Swiss Federal Act on Data Protection) regularly, not just at setup

The nFADP, which came into full force in September 2023, imposes ongoing obligations around data inventories, privacy notices, and breach reporting. Many small Swiss companies treat it as a one-time setup task, then fall out of compliance as their data practices evolve.

Pro Tip: Create a master compliance calendar at the start of each year and assign ownership to specific people, not just “the accountant.” Shared ownership of deadlines is how deadlines get missed. A detailed reference for maintaining this discipline lives in the Swiss company compliance steps guide.

Why Swiss business administration demands proactive strategic management

Most foreign entrepreneurs approach Swiss business administration the same way they approach taxes in their home country: reactively. They get organized at year-end, call their accountant in a panic, and file just before the deadline. In Switzerland, that approach is expensive.

Here is what years of working with international clients reveals: many founders underestimate how early they must line up accounting capability, because tax and VAT decisions depend on initial transaction categorization. The invoice you issue on day three of operations is already part of a data set that will inform your VAT threshold calculation, your tax return, and potentially your transfer pricing documentation if you have related-party transactions. You cannot retroactively fix how those early transactions were categorized without triggering corrections, interest, and auditor attention.

The second mistake is treating the commercial register as a set-and-forget document. When a director changes, a shareholder exits, or your registered address moves, that update must reach the register promptly. Delays create gaps between your legal record and your operational reality. Banks, counterparties, and regulators rely on register data. Outdated information has a way of surfacing at the worst possible moment, usually when you are trying to close a deal or open a new banking relationship.

The proactive approach looks different. It starts with choosing the right canton not just for today’s tax rate but for the incentives that match your business model in years two through five. It continues with quarterly self-audits, not because the law requires them but because they surface problems when they are still cheap to fix. And it integrates legal, financial, and operational administration into a single calendar that the leadership team actually owns.

This is not theoretical. Companies that treat maintaining Swiss compliance as a strategic priority consistently outperform those that treat it as a cost center to minimize. The difference shows up in cleaner audits, faster banking relationships, and the ability to move quickly on growth decisions without stopping to fix compliance gaps first.

How RPCS Solutions supports your Swiss business administration

Running a compliant, tax-efficient Swiss company from outside the country is genuinely complex. You need local knowledge, local representation, and local processes that do not break down when your team is in a different time zone.

RPCS Solutions provides end-to-end support for international entrepreneurs at every stage of Swiss business administration, from Swiss company formation services covering both GmbH and AG structures to helping you open a Swiss bank account that meets regulatory requirements. Our Swiss accounting services keep your books, VAT filings, and tax returns current and accurate throughout the year. We also handle nominee director appointments, registered address services, and commercial register maintenance, so your governance is always in order. Whether you are incorporating for the first time or taking over administration of an existing Swiss entity, RPCS provides the structured support that replaces guesswork with confidence.

Frequently asked questions

At what turnover must a company register for VAT in Switzerland?

VAT registration becomes mandatory once your annual turnover exceeds CHF 100,000, and you must register with the Swiss Federal Tax Administration within 30 days of crossing this threshold.

How do Swiss corporate tax rates vary across cantons?

Effective tax rates range from approximately 11.85% in Zug to 20.54% in Bern depending on the canton and commune, making canton selection one of the most impactful financial decisions you will make at incorporation.

What ongoing administration tasks are crucial for Swiss companies?

Key ongoing tasks include maintaining accurate records for 10 years, filing annual tax returns at federal and cantonal levels, updating the commercial register after governance changes, holding AGMs, and complying with nFADP data protection obligations.

Why is appointing a Swiss resident director important?

Swiss law requires at least one board member or managing director to be a Swiss resident, creating direct local accountability and ensuring your company can legally execute governance decisions and sign binding documents within the country.

Recommended

Comments