Why Switzerland Is the Top Choice for Family Offices

- 18 hours ago

- 9 min read

TL;DR:

Switzerland offers a unique combination of stability, discretion, and advanced banking infrastructure for family offices, making it difficult to replicate. Effective structuring requires meeting strict cantonal qualification criteria, building genuine operational substance, and maintaining ongoing compliance amid evolving regulations. Its long-term resilience and institutional strength continue to make Switzerland a premier choice for multigenerational wealth management despite recent market shifts.

Switzerland is not simply a low-tax address you park wealth in and forget. For high-net-worth families and institutional family offices evaluating where to build their long-term financial infrastructure, the real story is far more layered. Switzerland offers a rare combination of political stability, institutional depth, and legal precision that few jurisdictions can match, but accessing those advantages requires deliberate structuring, ongoing compliance, and a clear-eyed understanding of what has changed in recent years. This article cuts through the myths and gives you a practical framework for thinking about Switzerland in 2026.

Table of Contents

Key Takeaways

Point | Details |

Stability and discretion | Switzerland’s unique blend of financial stability and privacy laws makes it an attractive hub for family offices. |

Selective tax advantages | Cantonal tax incentives are valuable but hinge on strict qualification criteria for passive income and substance. |

Compliance is critical | Family offices must prioritize substance, licensing, and global compliance to access Swiss benefits in 2026. |

Evolving regulatory landscape | Ongoing regulatory and economic changes mean Switzerland is not a static solution—careful planning is necessary. |

Switzerland’s unique advantages for family offices

Switzerland’s reputation as a premier wealth management jurisdiction is not built on marketing. It rests on three interlocking pillars that are genuinely difficult for competing jurisdictions to replicate.

Political and institutional stability is perhaps the most underappreciated factor. Switzerland has maintained political neutrality for over two centuries, operates under a rule of law that is consistently ranked among the world’s strongest, and has not experienced the kind of abrupt regulatory reversals that have rattled family offices in other jurisdictions. When you are managing multigenerational wealth, that predictability has real monetary value.

Discretion goes beyond banking secrecy, which has admittedly narrowed under international pressure. Swiss culture and legal tradition still place a high premium on confidentiality, and the country’s professional ecosystem, including lawyers, trustees, and fiduciaries, operates within a framework that protects sensitive information. That matters when family dynamics, succession planning, and reputation management are all in play.

Banking infrastructure sets Switzerland apart in ways that pure tax calculations miss. Swiss private banks offer access to a depth of expertise in alternative assets, cross-border custody, currency management, and structured lending that most jurisdictions simply cannot offer at the same level. As advisors consistently note, Switzerland is a “stability + discretion + banking depth” jurisdiction, and all three components matter simultaneously.

Key structural advantages that family offices consistently cite include:

Access to multi-currency accounts and seamless cross-border transfer infrastructure

A deep pool of qualified investment managers, legal counsel, and compliance professionals

A legal stability environment that allows long-term planning without fear of sudden policy shifts

Central European location, making it operationally efficient for families with assets across multiple continents

Robust asset protection in Switzerland mechanisms under Swiss civil law

“Switzerland’s combination of stability, privacy culture, and financial infrastructure gives family offices a platform that is genuinely hard to replicate elsewhere, regardless of what the tax rate is in any given year.”

Recent trends reinforce this picture. After a period of regulatory turbulence globally, families are increasingly prioritizing jurisdictions that offer resilience and adaptability over those that simply advertise low nominal rates. Switzerland’s value proposition has actually strengthened in that environment.

Tax advantages and the reality of cantonal incentives

Switzerland’s federal structure is one of its most strategically useful features for family office planning. The country operates 26 cantons, each with its own tax rates layered on top of a federal base. The result is a range of effective tax rates across the country that can vary dramatically depending on where you establish your structure.

The cantonal tax system enables structuring family-office activities in lower-tax cantons, but qualification depends on meeting strict holding company criteria. This is where many families stumble. The assumption that you can simply register in Zug or Schwyz and automatically enjoy near-zero taxation is incorrect.

Holding company status requirements typically include:

At least 80% of gross income must come from dividends, interest, royalties, or capital gains, not active business income

No substantive commercial activity directed at the Swiss domestic market

Qualifying participations in subsidiaries must meet minimum ownership thresholds

Compliance with both cantonal and federal anti-abuse provisions

Documented economic rationale for the chosen canton

Here is a simplified comparison of what different cantonal environments can mean in practice:

Canton | Approximate effective corporate tax rate | Notes |

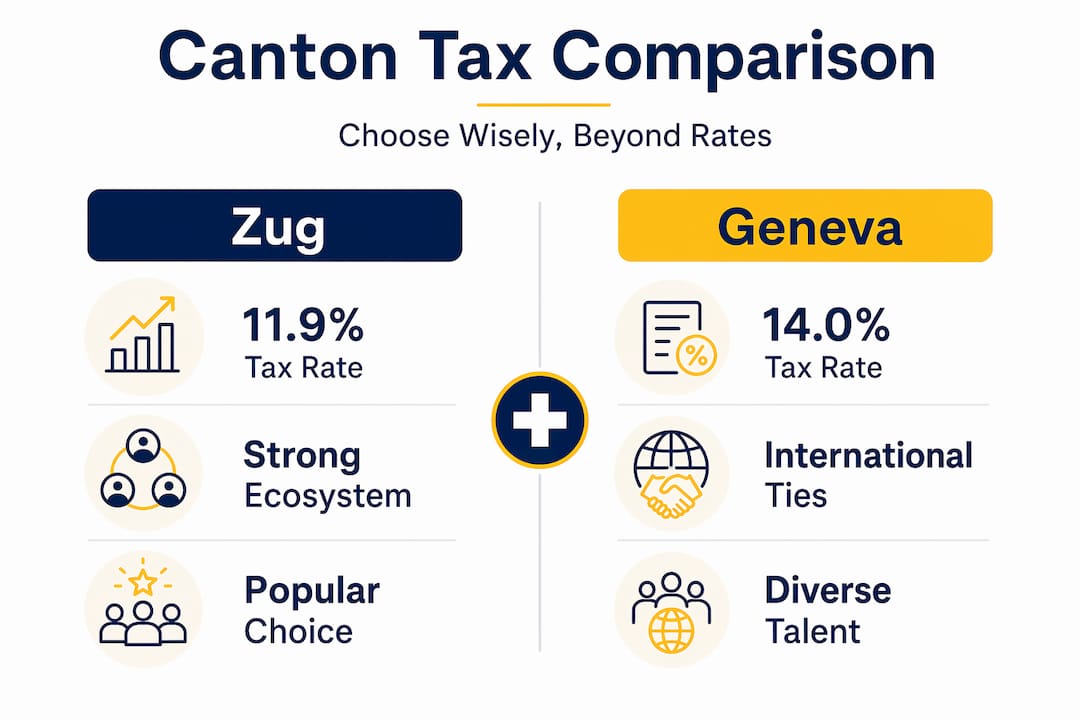

Zug | 11.9% | Popular, competitive, strong service ecosystem |

Schwyz | 12.5% | Low personal tax too, smaller infrastructure |

Nidwalden | 12.7% | Growing appeal for holding structures |

Geneva | 14.0% | Higher costs, greater banking access |

Zurich | 19.7% | Highest infrastructure depth, higher tax |

These figures represent standard corporate rates. Holding company regimes can reduce effective rates significantly below these benchmarks for qualifying structures, and in some scenarios, effective rates on passive income can fall below 1% when the participation exemption (tax relief on qualifying dividend income) is applied correctly.

Pro Tip: Do not select a canton based solely on its headline tax rate. Factor in the availability of qualified local directors, proximity to banking relationships, and the canton’s track record with international family office structures. Canton Zug offers more than a low rate; it offers an ecosystem.

For a detailed breakdown of how these structures work at the Swiss federal level, the Swiss tax structure benefits framework and specific tax optimization strategies are critical starting points for any planning exercise.

Modern substance and compliance expectations

The days when a brass-plate company in a Swiss canton was sufficient to claim tax benefits are firmly behind us. Swiss authorities, in alignment with OECD standards and bilateral commitments, now apply a substance-over-form test rigorously. What this means in practice is that the advantages of Swiss structuring are only accessible to family offices that build genuine operational presence.

Substance, as Swiss authorities define it, includes:

A physical office address that is not simply a shared mailbox

At least one qualified local director who actively participates in decision-making

Board meetings held in Switzerland with documented minutes and resolutions

Local staff or contracted professionals performing investment oversight functions

Clear evidence that the actual center of management is in Switzerland, not in the home country of the beneficial owner

Substance regulations and compliance duties play a critical role in Switzerland’s family office landscape, and the right structure depends on asset location, regulator comfort level, and applicable reporting frameworks like CRS (Common Reporting Standard) and FATCA (Foreign Account Tax Compliance Act).

On the licensing side, family offices need to assess carefully whether their activities trigger obligations under FINMA (the Swiss financial markets regulator) regulations. Managing third-party assets, providing investment advice for compensation, or operating as a collective investment scheme can all create licensing requirements. A pure single-family office managing only the founding family’s assets generally has a cleaner regulatory path, but even that requires careful documentation.

CRS and FATCA have eliminated the assumption of financial privacy in the traditional sense. Switzerland participates in automatic exchange of information with over 100 jurisdictions. This does not undermine Switzerland’s value, but it does mean that transparency is now built into the operating model. Families that understand this and structure accordingly are better positioned than those who resist it.

The shift from opacity to transparency in Swiss financial services has actually strengthened Switzerland’s long-term credibility as a jurisdiction. Structures that survive scrutiny are more durable than those built on information asymmetry.

For detailed guidance on meeting these Swiss substance requirements and understanding the broader company setup advantages, early planning is essential. Reviewing ESG and compliance resources can also support ongoing governance alignment for family offices with responsible investment mandates.

Pro Tip: Budget for a real compliance infrastructure from day one. Trying to retrofit substance after the fact is far more expensive than building it correctly at formation. A single qualified local director with genuine authority can satisfy many regulatory tests and adds real value beyond compliance.

Risks, tradeoffs, and common misconceptions

Switzerland’s advantages are real, but they are not unconditional. Several developments in the past few years have materially changed the risk calculus for family offices, and decision-makers need to factor these in honestly.

Recent market commentary warns that tax and regulatory changes, combined with increased scrutiny following major banking disruptions, can create meaningful uncertainty around Swiss benefits. The 2023 collapse of Credit Suisse, for example, prompted a broader reassessment of Swiss systemic risk assumptions that had previously been treated as near-absolute.

Risk category | Description | Mitigation approach |

Regulatory change | Cantonal or federal tax reform | Diversified holding structure, flexible entity |

Substance challenge | Authorities dispute real management location | Documented governance, active local directors |

Banking concentration | Over-reliance on single institution | Multi-bank relationships, custodian diversification |

Reporting obligations | CRS/FATCA compliance gaps | Annual review, specialist tax counsel |

Lump-sum tax changes | Reform of expenditure-based taxation | Regular legislative monitoring |

Common misconceptions that derail otherwise well-designed Swiss family office structures include:

“Switzerland always offers the lowest tax rate.” Not true. Several jurisdictions, including UAE free zones and certain Channel Islands structures, offer lower nominal rates. Switzerland competes on the total value package, not just price.

“All cantons are equally advantageous.” Far from it. The difference between Zug and Zurich can be 8 percentage points, plus significant differences in service infrastructure and regulatory culture.

“The setup is one-time.” Swiss tax authorities and FINMA both conduct ongoing reviews. Your structure must be maintained and adapted annually.

“Privacy means secrecy.” Switzerland offers legal confidentiality and discretion within a transparent reporting framework. Conflating the two creates compliance risk.

Mitigating these risks demands active management rather than passive administration. For families concerned about corporate tax advantages and how to preserve them over time, continuous legal and tax review is non-negotiable. Similarly, family office risk management frameworks that account for climate-related financial exposure are increasingly expected by regulators and institutional counterparties.

What most experts miss about choosing Switzerland

Most guides on this topic spend 80% of their content listing Switzerland’s advantages and 20% on boilerplate risk warnings. That ratio is backwards for anyone actually trying to make a well-informed decision.

The single most overlooked reality is that Switzerland rewards families who treat it as a living operating environment, not a static legal address. The families who extract the most value from a Swiss structure are those who invest in their Swiss operations: qualified directors who genuinely engage with investment decisions, governance processes that are documented and audited, and professional relationships with local advisors who understand both the legal landscape and the evolving political environment.

The second gap in most coverage is the failure to distinguish between short-term tax arbitrage and long-term capital preservation. Switzerland’s tax rates are competitive, but they are not the lowest you can find globally. What Switzerland offers that lower-tax jurisdictions often cannot is institutional resilience. A family office established in Switzerland in 1980 has operated through currency crises, geopolitical shocks, and major global regulatory reforms without losing its fundamental legal and operational footing. That durability is worth quantifying, even if it does not appear on a spreadsheet.

We have also seen families underestimate the importance of cantonal selection as an ongoing strategic decision rather than a one-time choice. As Switzerland continues to adapt its tax framework to OECD Pillar Two minimum tax requirements (the global 15% minimum corporate tax agreed under the OECD’s base erosion and profit shifting project), the differential between cantons is narrowing somewhat. This does not eliminate the value of Swiss structuring, but it does mean that the basis for canton selection is shifting toward operational factors like service quality and regulatory relationships, rather than pure rate arbitrage.

Finally, the best structures we see are built around secure wealth advice that integrates legal, tax, and banking considerations from the outset. Siloed advice from a tax lawyer who does not talk to the banking team, or a trustee who does not engage with the family’s estate planning counsel, produces fragile structures. Switzerland works best as a system, not as a collection of separate advantages stitched together.

Next steps: Establish your optimal family office structure in Switzerland

Building a Swiss family office that genuinely delivers on the jurisdiction’s promise demands more than choosing a canton and filing paperwork. It requires precise structuring, early engagement with banking institutions, and an ongoing compliance framework built by professionals who understand Swiss regulatory culture from the inside.

At RPCS Solutions, we work with high-net-worth individuals and family office executives to design and establish Swiss structures that are built for durability, not just initial tax efficiency. From Swiss company formation in the right entity type and canton, to helping you open a Swiss bank account with the right institutional partner, our team coordinates every layer of the setup process. We handle legal documentation, notarization, registration, and ongoing administrative support so your structure works correctly from day one and continues to perform as regulations evolve.

Frequently asked questions

What is the main advantage of Switzerland for family offices?

Stability, discretion, and banking infrastructure make Switzerland a leading jurisdiction, offering a complete ecosystem for managing complex, multigenerational wealth rather than just a favorable tax rate.

Is it easy to qualify for Switzerland’s lowest tax rates?

No. Qualifying for the lowest cantonal rates requires meeting strict holding company criteria, including passive income thresholds and documented absence of active domestic business activity.

How is substance defined for Swiss family offices?

Substance means real operations, including qualified local directors, physical office presence, and genuine governance activity in Switzerland, not just a registered legal address.

Are the tax benefits of Swiss family offices threatened by recent changes?

Switzerland remains highly attractive, but tax and regulatory changes following recent banking disruptions and OECD Pillar Two implementation require active monitoring to protect and maintain structural advantages.

Recommended

Comments