Double Taxation in Switzerland: What Investors Must Know

- 1 day ago

- 9 min read

TL;DR:

Switzerland uses over 100 bilateral double taxation agreements to prevent the same income from being taxed twice. The country applies exemption with progression or the credit method to resolve double taxation, depending on the income type. Active monitoring of permanent establishment status and proper treaty application are crucial for cross-border tax planning.

Double taxation in Switzerland is defined as the simultaneous taxation of the same income or capital by two countries, typically the country where income is earned and the country where the taxpayer is resident. Switzerland addresses this directly through a network of over 100 double taxation agreements (DTAs), making it one of the most treaty-covered jurisdictions in the world. The Swiss Federal Tax Administration enforces two primary relief methods: exemption with progression and the credit method. For international business owners and investors operating through Swiss GmbH or AG structures, understanding these rules is not optional. It is the foundation of sound cross-border tax planning.

What is double taxation in Switzerland and why does it matter?

Double taxation occurs when two countries each assert the right to tax the same income or capital in the same period. Switzerland resolves this through bilateral DTAs that allocate taxing rights between the source country and the residence country. The treaties do not create new taxation rights. They restrict and distribute existing rights under each country’s domestic law.

This distinction matters enormously for investors. A DTA between Switzerland and Germany, for example, determines which country taxes dividend income paid from a German subsidiary to a Swiss holding company, and at what rate. Without the treaty, both countries could apply their full domestic rates. With the treaty, one country’s right is limited or eliminated.

Switzerland has 8 additional agreements covering inheritance and estate taxes, beyond its core DTA network. That breadth gives Swiss-based structures access to treaty protection across virtually every major investment jurisdiction. For international investors, this is one of Switzerland’s most concrete and measurable advantages.

How do Swiss double taxation agreements prevent taxing the same income twice?

Swiss DTAs are bilateral treaties negotiated between Switzerland and individual partner countries. Most Swiss treaties follow the OECD model convention but include country-specific provisions that modify the standard framework. These modifications can affect which types of income are covered, which country has primary taxing rights, and what withholding tax rates apply.

The core mechanism works as follows:

Source state taxation: The country where income originates taxes it first, often at a reduced treaty rate.

Residence state relief: Switzerland, as the investor’s country of residence or incorporation, then applies either the exemption method or the credit method to eliminate or reduce residual double taxation.

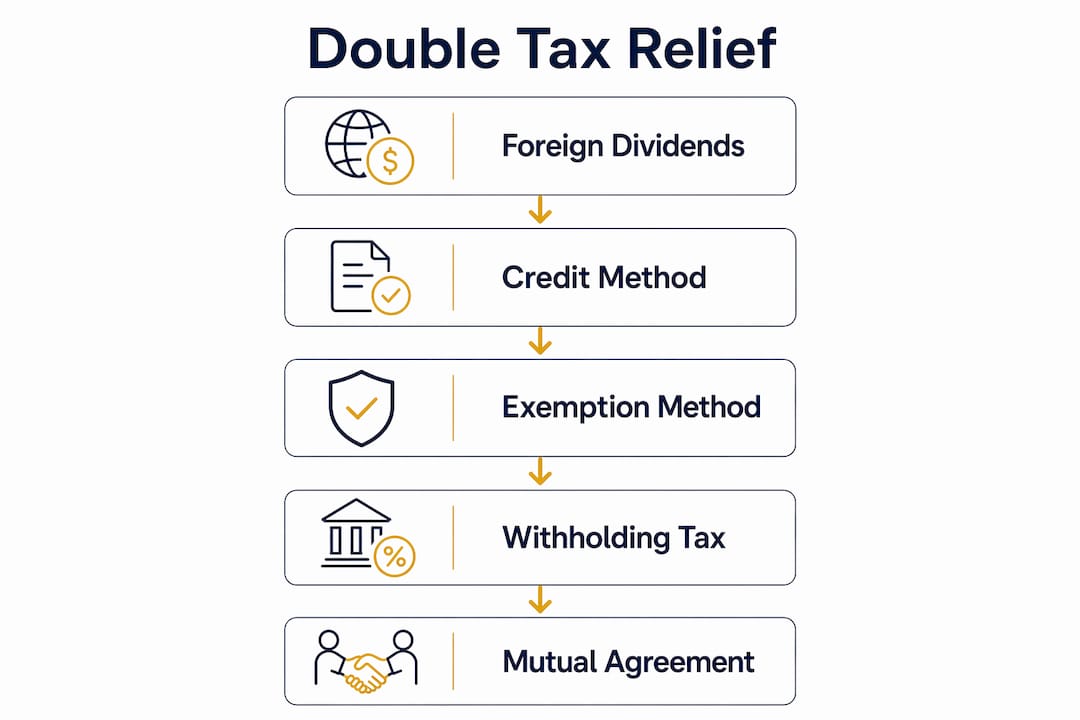

Withholding tax reduction: Switzerland’s domestic withholding tax rate on dividends stands at 35%. Treaty rates are generally lower than this statutory rate, often reduced to 5%, 10%, or 15% depending on the partner country and the ownership stake held.

Income scope: DTAs typically cover dividends, interest, royalties, capital gains, employment income, and business profits attributed to a permanent establishment.

Treaty limitations: Not all income types receive equal protection. Passive income and capital gains treatment varies significantly by treaty.

Pro Tip: Before structuring a holding company in Switzerland, verify the specific withholding tax rates in the relevant bilateral DTA. A 5% treaty rate on dividends versus a 15% rate can represent a material difference in annual cash flow for high-volume investment structures.

The Mutual Agreement Procedure (MAP) sits at the center of treaty dispute resolution. MAP allows taxpayers to apply to the Swiss State Secretariat for International Finance (SIF) when they believe a treaty partner has taxed them contrary to the agreement. The two competent authorities then negotiate directly to resolve the conflict. This mechanism protects investors from being caught between two tax authorities with conflicting interpretations.

What are the key methods Switzerland uses to relieve double taxation?

Switzerland applies two distinct relief methods, and the choice between them depends on the type of income and the applicable treaty.

Exemption with progression: Foreign income is excluded from Swiss taxable income but is included in the calculation of the applicable tax rate. A Swiss resident earning CHF 200,000 domestically and CHF 100,000 from a foreign source will pay Swiss tax only on the CHF 200,000, but at the rate that would apply to CHF 300,000 total income. The foreign income raises the rate without being directly taxed.

Credit method: Foreign taxes already paid on investment income such as dividends, interest, and royalties are credited against the Swiss tax liability on that same income. The credit is capped at the actual Swiss tax due on the foreign income. No carry-forward is allowed for unused credits, meaning excess foreign tax paid in a given year cannot offset Swiss tax in future years.

Federal and cantonal application: Both methods apply at the federal, cantonal, and communal tax levels. Switzerland’s three-tier tax system means relief must be calculated and claimed at each level separately.

Non-DTA countries: For income from countries without a DTA with Switzerland, no credit or exemption applies. A limited pre-tax deduction for irrecoverable foreign taxes may be available under Swiss domestic law, but this provides significantly less relief than a treaty credit.

Income type | Typical relief method | Key limitation |

Foreign dividends (DTA country) | Credit method | Capped at Swiss tax on that income |

Foreign business profits | Exemption with progression | Rate impact on domestic income |

Royalties and interest | Credit method | No carry-forward of unused credits |

Income from non-DTA countries | Limited deduction only | No credit or exemption available |

Pro Tip: Swiss withholding tax refund procedures require separate administrative filings. Treaty claimants must follow the correct process to obtain reduced withholding or refunds. Missing these deadlines forfeits the relief entirely.

How do Swiss permanent establishment rules affect double taxation?

Permanent Establishment (PE) is the legal concept that determines whether a foreign company has created a taxable business presence in Switzerland. PE status triggers local tax filing obligations and Swiss corporate tax liabilities, regardless of what treaty protections the parent company might otherwise enjoy.

PE can arise in ways that are not always obvious to foreign investors:

Maintaining a fixed place of business in Switzerland, such as an office or workshop

Having a dependent agent in Switzerland who habitually concludes contracts on the company’s behalf

Operating a construction site in Switzerland beyond the treaty’s time threshold, typically 12 months under OECD model rules

Providing services through employees present in Switzerland for extended periods

The risk is significant. Most foreign enterprises focus on treaty benefits and overlook PE exposure, which can result in unexpected Swiss tax filings and back-tax liabilities. A company that unintentionally creates a PE in Switzerland may owe Swiss corporate tax on profits attributable to that PE, even if the parent company is resident in a treaty partner country.

PE status also affects treaty benefits. Once a PE exists, the profits attributable to it are taxed in Switzerland under domestic corporate tax rules. The treaty then governs how the other country treats those same profits to avoid double taxation at the group level.

Pro Tip: Review your Swiss operations annually against the PE definition in the relevant bilateral treaty. A single employee with signing authority can create PE exposure. Early identification allows you to restructure before a tax authority makes the determination for you.

For investors considering Swiss company formation, understanding PE rules upfront prevents costly restructuring later. A properly formed Swiss entity, with a resident director and registered address, provides a clean legal structure that avoids accidental PE creation in the parent company’s home jurisdiction.

What options exist if taxpayers face unresolved double taxation under Swiss treaties?

When treaty application fails to eliminate double taxation, formal dispute resolution mechanisms are available. The process is structured but requires active participation from the taxpayer.

Identify the conflict: The taxpayer must determine that both Switzerland and the treaty partner have taxed the same income in the same period, contrary to the treaty’s allocation rules.

Apply for MAP: The taxpayer submits a written application to the Swiss State Secretariat for International Finance (SIF). SIF then contacts the competent authority in the partner country to initiate negotiations. The application must typically be filed within the time limit specified in the relevant treaty, often two to three years from the first notification of the disputed taxation.

Competent authority negotiations: The two tax authorities negotiate directly. The taxpayer is not a party to these discussions but may be asked to provide documentation or clarification. Outcomes range from full relief to partial adjustment to no agreement.

Administrative refund claims: Separately from MAP, taxpayers can file administrative claims for refunds of excess withholding tax under treaty provisions. These claims follow specific national procedures and deadlines set by each country.

Documentation requirements: Strong documentation is the foundation of any successful MAP or refund claim. This includes tax assessments from both countries, proof of income, treaty analysis, and correspondence with tax authorities.

Seeking qualified Swiss tax counsel before filing a MAP application is the most effective way to protect the claim. The Swiss tax advantages available through proper treaty application are substantial, but they require precise procedural compliance to access.

Key takeaways

Switzerland’s treaty network of over 100 DTAs, combined with the exemption and credit relief methods, makes it one of the most effective jurisdictions in the world for managing cross-border tax exposure.

Point | Details |

DTAs allocate, not create, tax rights | Treaties restrict each country’s taxing rights but do not override domestic law as the basis for taxation. |

Credit method has a hard cap | Foreign tax credits are limited to the Swiss tax due on that income, with no carry-forward for excess credits. |

PE risk is often underestimated | A dependent agent or fixed office can trigger Swiss corporate tax obligations regardless of treaty status. |

Non-DTA income gets limited relief | Income from countries without a Swiss DTA receives only a limited pre-tax deduction, not a full credit or exemption. |

MAP resolves treaty disputes formally | Taxpayers can apply to SIF to initiate competent authority negotiations when double taxation persists. |

Switzerland’s treaty network: what the numbers do not tell you

I have worked with international investors who arrive in Switzerland focused entirely on the headline corporate tax rates and the treaty list. They see 100-plus DTAs and assume the problem is solved. It is not.

The treaties allocate rights. They do not guarantee outcomes. What actually determines your tax position is the interaction between the treaty text, Swiss domestic law, your company’s structure, and the behavior of your employees and agents on the ground. I have seen holding structures that looked perfect on paper generate PE exposure because one director was signing contracts from a Swiss address without anyone noticing.

The credit method’s no-carry-forward rule is another point that catches investors off guard. If your foreign withholding tax exceeds your Swiss tax liability in a given year, that excess disappears. You cannot bank it. This makes income timing and structure genuinely important, not just theoretically interesting.

My strongest recommendation is to treat PE monitoring as an ongoing operational task, not a one-time legal review. Tax authorities in both Switzerland and partner countries are increasingly focused on substance requirements. A Swiss entity with a resident director and genuine local management activity is far more defensible than a letterbox structure with a Swiss address and no real presence.

Declare all global income fully. Incomplete declaration of worldwide income in Switzerland can be classified as tax fraud under Swiss law, regardless of whether that income was taxed abroad. The treaty does not protect you from that consequence.

— Rolands

How Rpcs supports Swiss company formation and tax compliance

International investors who want to access Switzerland’s treaty network need the right corporate structure in place first. A properly formed Swiss AG or GmbH, with a qualified resident director and a registered business address, is the foundation for claiming treaty benefits, managing PE risk, and meeting Swiss tax obligations.

Rpcs provides end-to-end Swiss company formation services covering legal documentation, notarization, registration, banking setup, and ongoing accounting and compliance support. For investors who need a Swiss resident director to satisfy local law requirements, Rpcs offers nominee director services that meet Swiss regulatory standards. Whether you are establishing a holding structure, a trading company, or a service entity, Rpcs delivers the legal and administrative infrastructure that makes treaty-compliant operations possible from day one.

FAQ

What is double taxation in Switzerland?

Double taxation in Switzerland occurs when both Switzerland and another country tax the same income or capital in the same period. Switzerland resolves this through over 100 bilateral DTAs that allocate taxing rights between the two countries.

How does the credit method work for Swiss investors?

The credit method allows Swiss residents to offset foreign taxes paid on dividends, interest, and royalties against their Swiss tax liability on that same income. The credit is capped at the actual Swiss tax due, and unused credits cannot be carried forward to future years.

What triggers a permanent establishment in Switzerland?

A permanent establishment arises when a foreign company maintains a fixed place of business in Switzerland or uses a dependent agent who habitually concludes contracts there. PE status triggers Swiss corporate tax obligations on profits attributable to that presence.

Can double taxation be resolved if treaty relief fails?

Yes. Taxpayers can apply to the Swiss State Secretariat for International Finance to initiate a Mutual Agreement Procedure. MAP enables competent authorities from both countries to negotiate a resolution without litigation.

Does Switzerland offer relief for income from non-DTA countries?

Switzerland does not provide a credit or exemption for income from countries without a bilateral DTA. A limited pre-tax deduction for irrecoverable foreign taxes may apply under Swiss domestic law, but this delivers significantly less relief than a full treaty credit.

Recommended

Comments