Why Switzerland Is the Top Choice for Holding Structures

- 2 days ago

- 10 min read

TL;DR:

Switzerland offers a globally respected, stable environment with a participation exemption regime that can significantly reduce taxes on qualifying dividends and capital gains. Its legal certainty, network of double tax treaties, and regional tax advantages make it a preferred choice for long-term international holding structures despite high setup costs. Proper compliance with thresholds and local substance requirements is essential to fully unlock these benefits and ensure long-term success.

Switzerland sits in an unusual position for global entrepreneurs: a high-cost, highly regulated European nation that can, under the right conditions, effectively reduce your corporate tax on dividends and capital gains to close to zero. Most international business owners assume Europe’s tax environment is uniformly punishing for holding structures. Switzerland defies that assumption. Its participation exemption regime, combined with political stability and an unmatched global reputation, makes it a serious contender for your next holding structure, provided you understand the specific rules that unlock those advantages.

Table of Contents

Key Takeaways

Point | Details |

Near-zero tax on qualifying income | Swiss holding companies can achieve almost zero tax rates on qualifying dividends and capital gains when participation thresholds are met. |

Strict eligibility criteria | Only companies meeting certain shareholding percentages or values, and holding periods, benefit from the participation exemption. |

Non-qualifying income taxed | Regular Swiss corporate taxes still apply to non-participation income, with rates varying by region. |

Watch for losses and holding periods | Offsets like tax loss carryforwards and short holdings can undermine the expected exemption. |

Global reputation and stability | Switzerland’s predictable legal framework and business stability are major advantages beyond tax. |

How Swiss holding structures work: Core concepts

Now that you have a sense of the overall allure, let’s break down what really sets Swiss holding structures apart.

A holding company is simply a legal entity whose primary purpose is to own shares or interests in other companies rather than to operate a business directly. In Switzerland, this structure becomes especially powerful because of the country’s participation exemption, a tax rule that reduces or eliminates corporate tax on income earned from qualifying shareholdings.

The tax benefits of Swiss holdings are rooted in this exemption. When your Swiss company holds a meaningful stake in a subsidiary, dividends received and capital gains on the sale of those shares can be largely excluded from taxable income. That is the core mechanic. But it only applies under precise conditions, which we will cover in detail shortly.

Typical features of a Swiss holding company:

Incorporated as an AG (Aktiengesellschaft) or GmbH (Gesellschaft mit beschränkter Haftung), two of the most common Swiss company structures

Primary purpose is ownership of equity stakes in subsidiaries, not direct business operations

Registered in Switzerland with a local address and at least one local director in most cases

Subject to ordinary Swiss corporate income tax on non-qualifying income

Eligible for double tax treaty benefits with over 100 countries

Can hold domestic and foreign subsidiaries simultaneously

Participation exemption qualification thresholds:

Criterion | Minimum requirement |

Minimum shareholding percentage | 10% of share capital |

OR minimum fair market value | CHF 1,000,000 |

Holding period for capital gains | At least 1 year |

Type of income covered | Dividends, qualifying capital gains |

When you choose among the available legal entity options, the AG is the most widely used for international holding structures because it allows broader share capital flexibility and is more recognized by foreign banks and investors.

Pro Tip: Many entrepreneurs overlook that non-qualifying income earned by the holding company is still fully subject to ordinary Swiss corporate taxation. The exemption is not a blanket rule for all profits.

Tax advantages: Participation exemption and its impact

Understanding the concept is useful, but the practical tax impact is what truly attracts global investors.

The Swiss participation exemption covers dividends and capital gains from qualifying shareholdings. When those thresholds are met, the exemption does not fully zero out the tax mathematically. Instead, it proportionally reduces the taxable base in a way that results in an extremely low effective rate on that income. In practice, many well-structured Swiss holding companies achieve effective rates on qualifying participation income that are negligible.

Comparison: Swiss participation exemption vs. standard holding regimes

Jurisdiction | Participation exemption threshold | Effective rate on dividends | Capital gains exemption |

Switzerland | 10% or CHF 1M, 1-year hold | Near zero | Yes, with conditions |

Netherlands | 5% (subject to conditions) | Exempt (participation exemption) | Generally exempt |

Luxembourg | 10% or EUR 1.2M, 12-month hold | Exempt (conditions apply) | Exempt (conditions apply) |

Singapore | No formal threshold (exemptions apply) | Exempt (one-tier system) | Generally no CGT |

Germany | 10% minimum | 95% exempt (5% taxable) | 95% exempt |

Switzerland’s regime stands out not necessarily because the headline exemption is more generous than every alternative, but because the broader package, including political stability, treaty access, and regulatory predictability, is hard to match. In terms of the Swiss tax system for companies, the cantonal layer matters too. Some cantons, such as Zug and Nidwalden, have substantially lower base corporate tax rates, meaning even non-qualifying income faces a lighter burden than it would in most European countries.

Practical implications for international investors:

Dividends flowing up from operating subsidiaries in high-tax countries can be received largely tax-free at the Swiss holding level

Capital gains on the eventual sale of a subsidiary stake are effectively exempt if the one-year holding requirement is satisfied

Swiss holding companies can access over 100 double tax treaties, reducing withholding taxes on inbound dividends

Cantonal tax competition means you can optimize by choosing the right location within Switzerland

The tax strategies in Switzerland that work best are those built around the participation exemption from the start, not retrofitted later.

Pro Tip: The effective near-zero rate on qualifying income depends entirely on meeting the participation thresholds. If your holding company also carries prior-year tax losses, those losses can offset the qualifying participation income, which sounds good but actually means the exemption mechanism is wasted rather than applied cleanly. Structure your finances carefully.

Legal rules, edge cases, and common misconceptions

While the advantages are significant, the rules can be nuanced, and missing a detail can eliminate the expected savings.

Steps to ensure compliance for qualifying participations:

Confirm the shareholding percentage. You must hold at least 10% of the share capital of the subsidiary. Holding less, even 9.9%, removes the participation exemption entirely for that stake.

Check the fair market value alternative. If you hold less than 10% but the market value of the participation is at least CHF 1,000,000, you may still qualify. This threshold must be met at the time income is received.

Satisfy the one-year holding period for capital gains. Dividends can qualify without a holding period, but capital gains on the sale of the participation require a minimum one-year hold.

Categorize the income correctly. Not all returns from a subsidiary qualify. Interest income, royalties, and management fees are generally not covered by the participation exemption and are taxed at standard rates.

Monitor your loss carryforward position. Prior-year tax losses at the holding company level can reduce or eliminate the benefit you expect to receive from the participation exemption.

File correctly at both federal and cantonal levels. Switzerland operates a two-tier corporate tax system, federal plus cantonal, and participation exemption applications must align with the rules at both levels.

“The most common mistake we see is entrepreneurs who assume that once they meet the 10% threshold, all income from the subsidiary is tax-free. That is simply not true. Only dividends and qualifying capital gains fall under the exemption. Everything else is taxed. And if you have losses sitting on your books, those losses consume the benefit before you can use it.”

Incorporation best practices emphasize getting a tax opinion before you transfer shares into a Swiss holding structure. Moving assets in without proper planning can trigger recognition events and offset the very savings you were hoping to achieve.

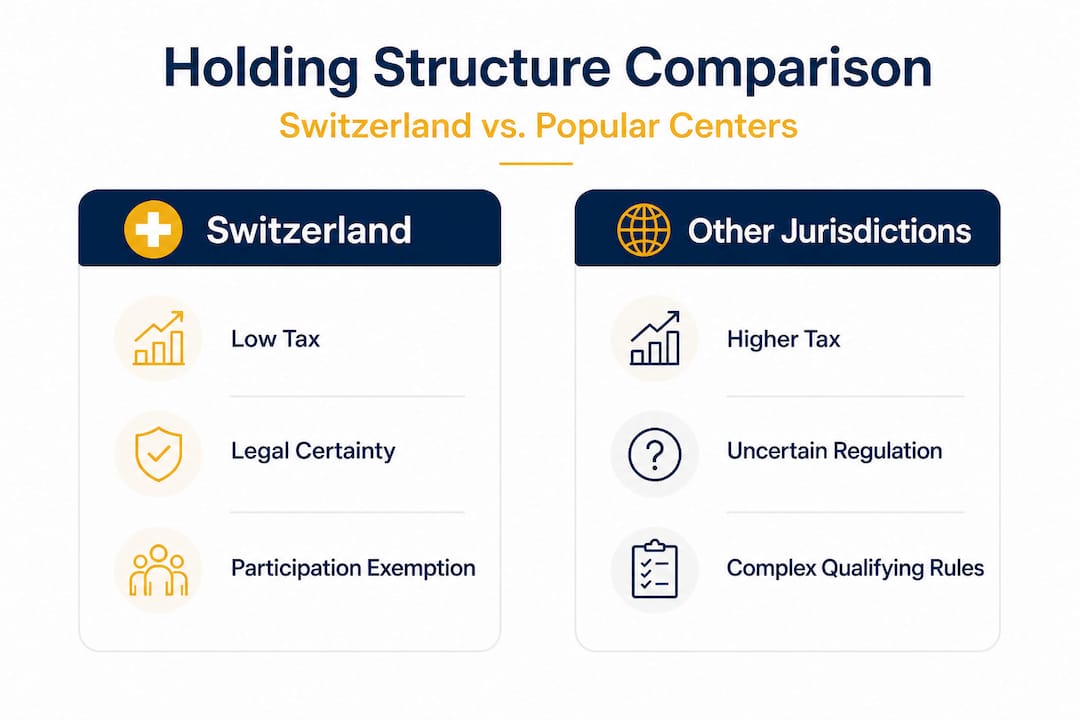

Swiss holding structures in the global context: How do they compare?

For international entrepreneurs, the decision is rarely “Switzerland or nothing,” so let’s see how it measures up against alternatives.

Switzerland is not the only place that offers participation exemptions. The Netherlands, Luxembourg, Singapore, and even Ireland have competing regimes. What distinguishes Switzerland is the combination of factors rather than any single element.

Switzerland’s unique advantages:

Political and monetary stability. Switzerland has not had a government crisis or a major banking regulatory overhaul in decades. That kind of predictability has real financial value when you are planning a 10 or 20-year holding structure.

Legal certainty. Swiss contract law and corporate law are well established, clearly codified, and enforced consistently. Disputes are resolved in a reliable judicial framework.

Reputation with banks and counterparties. A Swiss AG or GmbH holding company is recognized and trusted globally. Many banks and institutional investors apply different, more favorable standards when they see a Swiss structure versus, say, a holding company from a jurisdiction perceived as a tax haven.

Tax transparency. Switzerland has signed the OECD Common Reporting Standard and Base Erosion and Profit Shifting frameworks. It is not on any major blacklist. This matters enormously for your downstream operating companies and their relationships with tax authorities.

Access to double tax treaties. With over 100 active treaties, near-exempt treatment for qualifying participations combines with reduced withholding taxes to create a genuinely efficient structure.

Comparison: Switzerland vs. other popular holding destinations

Factor | Switzerland | Netherlands | Luxembourg | Singapore |

Participation exemption | Yes (10% or CHF 1M) | Yes (5%) | Yes (10% or EUR 1.2M) | Partial |

Political stability | Very high | High | High | High |

Treaty network | 100+ | 100+ | 85+ | 90+ |

OECD/FATF compliance | Full | Full | Full | Full |

International reputation | Exceptional | Strong | Strong | Strong |

Minimum local substance | Required | Required | Required | Required |

Understanding where global companies choose to headquarter helps illustrate this point. Major multinationals including Google, Johnson and Johnson, and Nestlé maintain significant Swiss operations precisely because the combination of legal, tax, and reputational factors makes Switzerland their preferred base.

Trade-offs to be aware of:

Local substance requirements mean you cannot just register a mailbox company. You need a genuine local presence.

Setup costs and ongoing compliance costs in Switzerland are higher than in some competitors.

Swiss corporate governance standards require real documentation, proper board meetings, and formal accounting.

Setting up a Swiss holding company: The practical steps

Armed with the context and caveats, here is how you can move forward to leverage Swiss benefits while minimizing risk.

Key setup steps:

Choose your legal entity. For holding purposes, the AG is generally preferred for international investors due to its share capital flexibility (minimum CHF 100,000) and broader investor recognition. The GmbH is simpler to manage but less flexible for complex shareholder structures.

Prepare documentation. Articles of association, shareholder identification, proof of capital, and the intended corporate purpose must all be prepared and notarized before registration.

Register with the cantonal commercial registry. Choose your canton strategically. Zug, Schwyz, and Nidwalden consistently rank among the most tax-efficient for holding structures.

Open a corporate bank account. Swiss banks perform thorough due diligence on holding companies. You will need to demonstrate the source of capital, the business purpose, and the ultimate beneficial owners.

Ensure the 10% shareholding threshold is met from day one. If your holdings fall below the qualifying percentage, plan to acquire additional shares or structure around the CHF 1 million fair market value alternative.

Establish local substance. Appoint a local director or use a reputable fiduciary service. Ensure the holding company can demonstrate genuine decision-making activity in Switzerland.

Engage local tax and legal advisors. Filing for the participation exemption at both the federal and cantonal levels requires specialist knowledge that foreign advisors often lack.

Pro Tip: Many of the errors in Swiss holding structures relate to the transfer of existing subsidiary shares into the new holding company. This step often triggers capital gains or stamp duty implications that are underestimated. The IP holding benefits available in Switzerland also deserve attention if your subsidiaries hold intellectual property, as separate favorable regimes exist for IP-generating companies.

Why most entrepreneurs overlook the real strengths of Swiss holding structures

To round out our guide, let’s look at what truly makes Switzerland stand out. It is more than just tax numbers.

Most entrepreneurs focus almost entirely on the participation exemption rate when evaluating Switzerland. That focus is understandable, but it misses the bigger picture. The near-zero tax rate is attractive. However, the reason established, sophisticated investors consistently choose Switzerland is the legal and regulatory environment, not just the headline number.

Consider this: a holding structure that saves you tax today but creates uncertainty, compliance risk, or reputational damage tomorrow is a bad deal. Switzerland’s track record of regulatory consistency is genuinely rare. The rules that applied to holding structures 20 years ago are largely the same rules that apply today. That predictability has enormous value when you are planning long-term capital allocation or considering an eventual exit.

“Switzerland’s advantage over most competing jurisdictions is not that it offers the absolute lowest tax rate. It is that it offers a credible, stable, internationally respected environment where you can build a structure today and trust it will still function the way you expect it to in 15 years.”

Short-term cost-cutting through lower-cost jurisdictions often backfires. We have seen entrepreneurs establish holding structures in cheaper domiciles, only to face pushback from institutional investors, banks, and acquiring companies who view those jurisdictions skeptically. The cost of restructuring into a more credible jurisdiction later typically exceeds the savings made upfront.

The Swiss corporate tax perspective that we consistently advocate is this: treat Switzerland not as a tax hack but as a long-term strategic platform. When you approach it that way, the setup costs, the substance requirements, and the compliance obligations all make perfect sense as investments rather than burdens.

Unlock Swiss advantages with expert guidance

Switzerland’s participation exemption and stable legal framework create a genuinely compelling case for international investors seeking long-term holding structures. Getting the setup right from day one, choosing the correct entity, the right canton, and meeting participation thresholds precisely, requires experienced local support.

At RPCS, we specialize in guiding international entrepreneurs through every step of Swiss company formation, from entity selection and documentation to registration and ongoing compliance. We also assist with Swiss bank account setup, a critical and often underestimated step for foreign-owned holding companies. If you are ready to explore whether a Swiss holding structure fits your international business goals, our team is here to make the process efficient, compliant, and straightforward.

Frequently asked questions

What is the Swiss participation exemption and who qualifies?

The Swiss participation exemption allows holding companies with at least 10% shareholding or a CHF 1 million investment in subsidiaries to receive near-zero tax on dividends and some capital gains, provided specific conditions such as the minimum holding period are met.

Are all Swiss holding company profits tax-exempt?

No. Only qualifying participation income is near-exempt. Non-qualifying income such as interest, royalties, and management fees is taxed at regular corporate rates, which vary by canton and municipality.

What are the main risks or pitfalls of Swiss holding structures?

Common pitfalls include failing minimum participation thresholds, not holding shares for at least one year before a capital gains event, or carrying prior-year losses that offset and effectively eliminate the expected tax benefits.

How does Switzerland compare to other European holding company centers?

Switzerland typically offers more predictable, near-exempt treatment for qualifying participations and stronger long-term legal stability, though establishing local substance and managing compliance tends to require more investment than in some alternative domiciles.

Recommended

Comments