Switzerland Substance Requirements: A 2026 Business Guide

- 1 hour ago

- 8 min read

TL;DR:

Switzerland requires companies to demonstrate genuine economic presence through financial, physical, and functional criteria. Meeting these standards affects tax treaty benefits, withholding tax refunds, and cantonal tax rates. Proper documentation and real operational activities from the start are essential for compliance.

Switzerland’s substance requirement is defined as the obligation for a company registered in Switzerland to demonstrate genuine economic presence through financial, physical, and functional criteria. The Swiss Federal Tax Administration (SFTA) and cantonal tax offices enforce these rules to confirm that companies conduct real business activities locally, not just maintain a legal address. Meeting substance requirements in Switzerland determines whether your company qualifies for tax treaty benefits, withholding tax refunds, and favorable cantonal tax rates. For foreign entrepreneurs pursuing Swiss company formation, understanding these rules before incorporation is the single most important compliance step you will take.

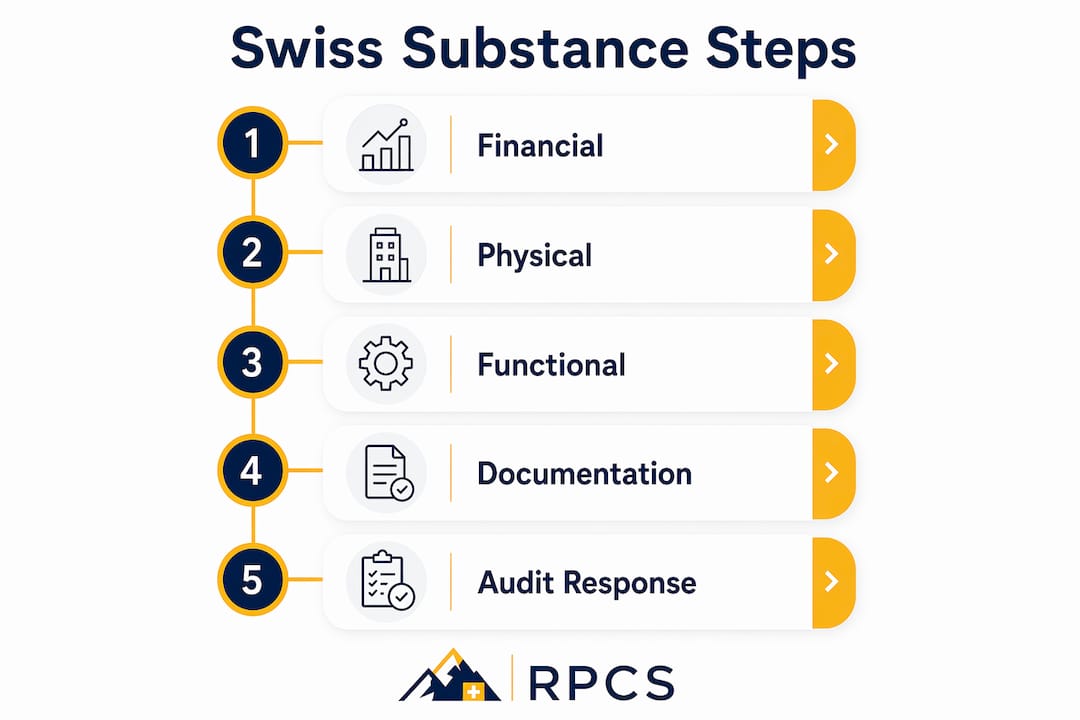

What is substance requirement Switzerland: the three core criteria

Switzerland substance regulations organize around three distinct criteria: financial substance, physical substance, and functional substance. The SFTA requires companies to satisfy at least one of these criteria under standard conditions. Higher-risk structures such as holding companies with indirect shareholders not entitled to treaty benefits must satisfy two criteria simultaneously. That distinction matters because it directly affects how you structure your equity, staffing, and governance from day one.

Swiss authorities treat substance as a functional reality, not a filing formality. A company that exists only on paper to access treaty benefits is precisely what the SFTA targets. The rules apply across GmbH and AG structures, holding companies, finance entities, and regional headquarters.

What does financial substance mean under Swiss regulations?

Financial substance is defined as maintaining a minimum equity ratio of approximately 30% relative to total assets, calculated using local GAAP book values. This threshold signals to cantonal tax offices that your company carries real economic risk and is not a shell funded entirely by intercompany loans.

The practical implications are significant. A holding company managing CHF 50 million in assets must maintain qualified staff and demonstrate adequate financing, not just file statutory accounts. Auditors reviewing financial substance will request:

Statutory financial statements showing equity levels

Proof of equity contributions and shareholder loans

Financing agreements that reflect arm’s-length terms

Balance sheet history covering multiple fiscal years

Different cantons interpret the 30% equity threshold with slight variations in documentation expectations. Zug tends to accept well-organized statutory accounts alongside staffing evidence. Geneva applies a more document-intensive review, often requesting three years of financial records in a single audit cycle.

Pro Tip: Set your equity structure before incorporation, not after. Retroactively recapitalizing a company to meet the 30% threshold raises red flags with cantonal auditors and complicates your tax treaty position.

For Swiss holding companies specifically, financial substance is the baseline criterion. Without it, no amount of physical presence will rescue your treaty eligibility.

What are the physical substance rules in Switzerland?

Physical substance requires a dedicated office space and qualified employees who perform work relevant to the company’s actual operations. Renting a desk in a shared space or registering a virtual office in Switzerland is considered a weak position by both the SFTA and Swiss banks. Authorities require demonstrable infrastructure directly linked to the entity’s activities.

The staffing requirement is equally specific. You need employees with qualifications matching your company’s business purpose, not just administrative support. A Swiss resident director who exercises real decision-making authority, not just signature authority, is a core component of physical substance. The following steps define a compliant physical presence:

Lease a dedicated office under the company’s name, with a formal lease agreement as documentary evidence.

Hire at least one full-time equivalent employee with qualifications relevant to the company’s core activities.

Appoint a Swiss resident director who attends board meetings in Switzerland and makes material decisions locally.

Maintain employment contracts, payroll records, and HR documentation showing genuine labor relationships.

Ensure the office contains working infrastructure: equipment, communication systems, and records storage tied to the entity.

For large holding companies with assets exceeding CHF 50 million, cantonal authorities in Zug expect at least one qualified FTE beyond board representation. That employee must have expertise relevant to the assets being managed, such as investment analysis or treasury management.

Pro Tip: Corporate service providers can handle administrative tasks, but they cannot substitute for a qualified employee on your payroll. Auditors distinguish between outsourced administration and genuine local staffing.

How does functional substance work in practice?

Functional substance is defined as the active performance of core business functions within Switzerland, including management, control, investment decisions, and strategic oversight. It is the hardest criterion to fake and the one the SFTA scrutinizes most closely during audits.

Swiss authorities examine whether your company’s strategic decisions are actually made in Switzerland or simply rubber-stamped there after being decided abroad. The difference between a compliant holding entity and a treaty-shopping vehicle often comes down to where the real power sits. Key indicators of functional substance include:

Board meetings held physically in Switzerland with documented agendas and minutes

Investment or financing decisions recorded as originating from Swiss-based management

Local management with authority to approve budgets, contracts, and group transactions

Active oversight of subsidiaries conducted from the Swiss office, not a foreign parent

Regular correspondence and reporting generated from the Swiss entity itself

Non-compliance with functional substance carries serious consequences. The SFTA may refuse withholding tax refunds and deny the declaration procedure entirely. Standard withholding tax rates apply, and treaty benefits are revoked. For a holding company receiving intragroup dividends, that outcome erases the primary financial rationale for the Swiss structure.

How do cantonal differences affect substance compliance?

Switzerland’s 26 cantons apply federal substance rules with meaningful local variations. The canton you choose for incorporation shapes both your tax rate and the documentation burden you will face during audits.

Canton | Substance focus | Documentation intensity | Key requirement |

Zug | Staffing and equity | Moderate | One qualified FTE, Swiss-resident director |

Geneva | Governance and contracts | High | Three years of board minutes, lease agreements, employment contracts |

Zurich | Economic rationale | Moderate to high | Clear link between Swiss entity and group operations |

Geneva’s cantonal tax administration routinely requests three years of documentation during substance audits, including board minutes, employment contracts, and lease agreements. That means you need to build your documentation system from the first month of operations, not the first month of an audit notice.

Zug applies informal guidelines that emphasize at least one qualified full-time employee and a Swiss-resident director. Its lower cantonal tax rate attracts holding and finance companies, but the SFTA applies federal scrutiny regardless of cantonal leniency. Zurich focuses on whether the Swiss entity has a genuine economic rationale within the group structure. A company that exists solely to route dividends through Switzerland without adding operational value will face challenge in Zurich regardless of its staffing levels.

Aligning your Swiss company registration with the right canton requires matching your business model to the local authority’s substance priorities, not just chasing the lowest tax rate.

Practical steps for documenting substance compliance

Substance compliance is built through consistent documentation, not assembled at audit time. The SFTA and cantonal offices treat gaps in records as evidence of insufficient substance, even when the underlying activities are genuine.

The most critical documents for any substance audit are:

Board minutes from every meeting held in Switzerland, recording specific decisions made locally

Lease agreements showing the company’s name, address, and term of occupancy

Employment contracts and payroll records for all Swiss-based staff

Statutory accounts demonstrating the equity ratio relative to total assets

Correspondence and contracts showing the Swiss entity as the active party

Meeting substance requirements involves both documented governance and real operational presence. Companies that treat board minutes as a formality, recording only generic resolutions, consistently fail audits because the minutes do not reflect actual Swiss decision-making.

Pro Tip: Schedule board meetings in Switzerland at least quarterly and record specific decisions, not just attendance. A minute that reads “the board reviewed operations” provides no substance evidence. A minute that reads “the board approved the CHF 2 million financing facility for Subsidiary X” does.

Responding to an SFTA audit request requires producing documents within the specified deadline. Delays or incomplete submissions signal non-compliance and accelerate escalation. Rpcs supports clients with corporate substance guidance that covers documentation systems, director appointments, and registered address solutions built for audit readiness.

Key Takeaways

Swiss substance requirements demand genuine financial, physical, and functional presence. Companies that treat substance as a checkbox exercise face withholding tax denial, treaty benefit revocation, and audit penalties from the SFTA.

Point | Details |

Three substance criteria | Financial, physical, and functional substance each require distinct evidence and documentation. |

30% equity threshold | Financial substance requires equity of approximately 30% of total assets under local GAAP. |

Two criteria for high-risk structures | Treaty-shopping risk or indirect shareholders without treaty rights trigger a dual-criterion requirement. |

Canton-specific documentation | Geneva requires three years of records; Zug emphasizes qualified staff and a Swiss-resident director. |

Documentation built from day one | Board minutes, lease agreements, and employment contracts must reflect real Swiss activities from incorporation. |

Why substance compliance is harder than most founders expect

Most entrepreneurs I work with underestimate how operational substance compliance actually is. They assume that appointing a Swiss director and renting an office covers the requirement. It does not. The SFTA looks at whether the director made real decisions in Switzerland, not whether they signed documents there.

The structures that fail audits most often are family offices and private equity holding entities that were set up efficiently but not operationally. The paperwork looks correct. The equity ratio is fine. But the board minutes are generic, the director is based abroad and visits quarterly, and the office is a serviced desk with no dedicated staff. That combination fails on functional substance every time.

My advice is to treat substance planning as part of your corporate strategy, not your compliance checklist. If your Swiss entity is a regional holding company, it should actually hold and manage regional investments from Switzerland. The management decisions, the investment approvals, the subsidiary oversight. All of it should happen here, be documented here, and be traceable to Swiss-based personnel.

Choosing the right canton matters too. If you are building a structure that will face SFTA scrutiny, Geneva’s documentation culture is actually an asset. It forces you to build proper records from the start. Zug’s informal approach can lead founders to under-document, which creates problems at the federal level even when the cantonal office is satisfied.

The one thing I see founders consistently skip is the business tax optimization step that connects substance planning to the broader group structure. Substance requirements do not exist in isolation. They interact with transfer pricing, dividend flows, and treaty positions across your entire group. Plan for all of it together.

— Rolands

How Rpcs helps you meet Swiss substance requirements

Building a compliant Swiss company structure requires more than legal registration. It requires the right office address, qualified resident directors, and documentation systems that hold up under SFTA scrutiny.

Rpcs provides Swiss company formation services that cover every element of substance compliance: GmbH and AG incorporation, Swiss resident director appointments, registered business addresses, and accounting services aligned with cantonal requirements. Foreign entrepreneurs get a complete setup that satisfies both federal and cantonal substance rules from day one. Rpcs also supports Swiss bank account opening, which banks require evidence of genuine substance before approving. Contact Rpcs to build a structure that meets Switzerland’s substance criteria and protects your treaty benefits long term.

FAQ

What is the substance requirement in Switzerland?

The substance requirement in Switzerland is the obligation for a company to demonstrate real economic presence through financial, physical, and functional criteria. The SFTA enforces these rules to prevent treaty shopping and ensure companies conduct genuine business activities locally.

How many substance criteria does a Swiss company need to meet?

Most Swiss companies must satisfy one substance criterion, but high-risk structures such as holding entities with indirect shareholders not entitled to treaty benefits must meet two criteria simultaneously.

Does a virtual office satisfy Swiss substance requirements?

A virtual office does not satisfy Swiss substance requirements. Authorities require dedicated office infrastructure and qualified staff directly linked to the company’s activities, not just a registered mailing address.

What happens if a Swiss company fails substance requirements?

The SFTA may deny withholding tax refunds, revoke tax treaty benefits, and apply standard tax rates. Non-compliant companies also face audit penalties and potential reclassification of their tax position.

Which Swiss canton has the strictest substance documentation rules?

Geneva applies the most document-intensive substance audits, routinely requesting three years of board minutes, employment contracts, and lease agreements. Zug and Zurich have moderate requirements but remain subject to federal SFTA scrutiny.

Recommended

Comments