Swiss VAT Explained: A 2026 Guide for Entrepreneurs

- a few seconds ago

- 8 min read

TL;DR:

Swiss VAT is a federal consumption tax paid by the end consumer and collected by businesses. It applies at three rates and requires registration for companies exceeding CHF 100,000 in worldwide turnover, with exemptions for health, education, and cultural services. Proper management of input and output VAT ensures compliance and prevents costly errors for foreign and domestic businesses operating in Switzerland.

Swiss VAT is a federal value-added tax applied to goods and services across Switzerland, functioning as a consumption tax ultimately paid by the end consumer. If you are setting up or running a business in Switzerland, understanding what is Swiss VAT and how it affects your operations is not optional. It is a legal obligation. Swiss VAT contributes approximately CHF 28 billion annually to the federal budget, funding welfare, transport, education, and national defense. That scale alone tells you how central this tax is to the Swiss economy.

What is Swiss VAT and how does it work?

Swiss VAT is defined as a federal consumption tax levied on goods and services at each stage of production and distribution. The formal term used by Swiss authorities is Mehrwertsteuer, abbreviated as MWST. Businesses collect VAT on behalf of the government, making them tax intermediaries rather than the final payers. The tax burden falls entirely on the end consumer.

The system operates on a neutrality principle. Businesses collect output VAT on their sales and reclaim input VAT on their purchases, then pay the net difference to the Federal Tax Administration. This means VAT does not become a cost for the business itself, as long as the business manages its records correctly. A manufacturer buying raw materials, processing them, and selling finished goods pays VAT at each step but recovers what it paid at the previous step.

Pro Tip: Keep your input and output VAT records separate from the start. Mixing them with general expenses is the most common accounting error that triggers audits from the Federal Tax Administration.

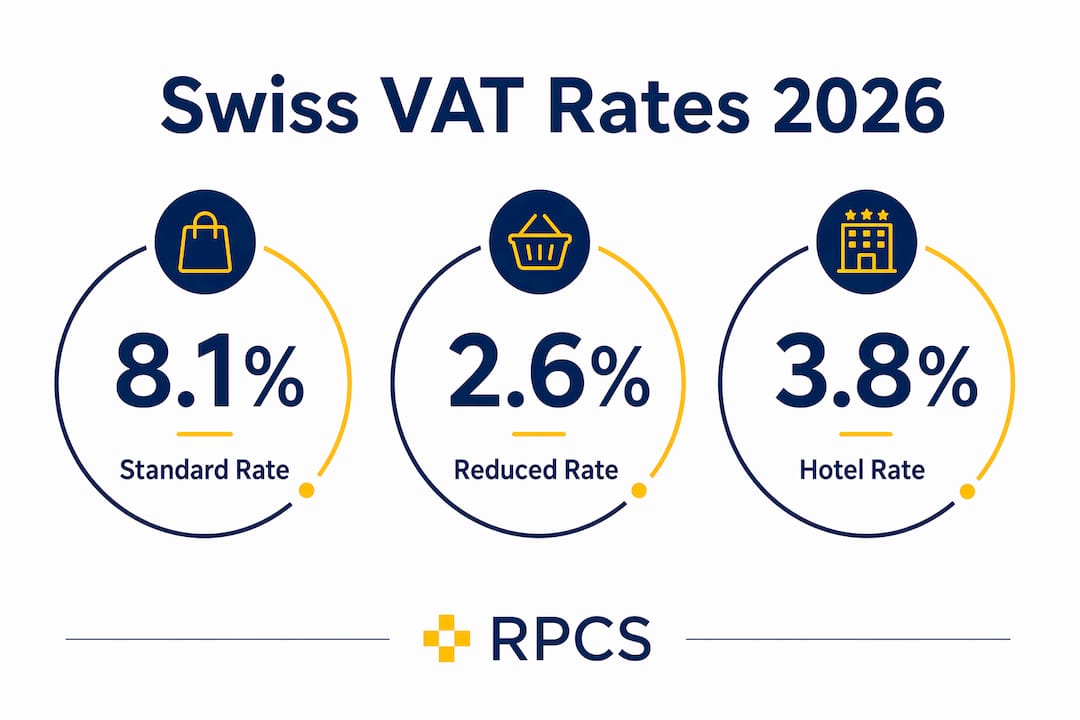

What are the current Swiss VAT rates?

Switzerland uses three VAT rates, each applying to a distinct category of goods and services. The standard rate is 8.1%, covering most consumer goods and services. The reduced rate of 2.6% applies to essentials. The special rate of 3.8% applies exclusively to the hotel and accommodation industry.

Reduced rate: what qualifies

The 2.6% reduced rate covers food and non-alcoholic beverages, books and newspapers, medicines, and certain agricultural products. These are goods the Swiss government classifies as necessities. Applying the wrong rate to these categories is a common compliance error for new businesses.

Exempt categories

Certain sectors pay no VAT at all. Health services, education, and cultural activities are exempt from Swiss VAT. Exempt status means no VAT is charged on sales, but it also means the business cannot reclaim input VAT on its purchases. That distinction matters for your cash flow planning.

Category | VAT Rate |

Most goods and services | 8.1% |

Food, books, medicines | 2.6% |

Hotel and accommodation | 3.8% |

Health, education, culture | Exempt |

Who must register for Swiss VAT?

Businesses with annual turnover exceeding CHF 100,000 must register for VAT in Switzerland. This threshold applies to global turnover, not just Swiss revenue. A foreign company earning CHF 120,000 worldwide but selling into Switzerland crosses the threshold and must register.

The registration process involves these steps:

Determine whether your global turnover exceeds CHF 100,000.

Apply for registration with the Federal Tax Administration online.

Obtain your Unique Enterprise Identification Number, known as the UID, which serves as your VAT number on all invoices.

If you are a non-Swiss company, appoint a Swiss fiscal representative to act on your behalf.

Begin charging VAT on taxable supplies from your registration date.

Non-Swiss companies that surpass the threshold must register and often appoint a Swiss fiscal representative. That representative takes on legal responsibility for your VAT filings. Choosing a qualified representative is not a formality. It is a legal safeguard. You can find detailed guidance on this process in this VAT registration guide for entrepreneurs.

Smaller businesses below CHF 100,000 can register voluntarily. Voluntary registration makes sense if you purchase significant inputs and want to reclaim the VAT paid on them. For startups buying equipment or software before generating revenue, voluntary registration can produce a net cash benefit.

Pro Tip: If you expect to reach CHF 100,000 in turnover within your first 12 months, register proactively. Late registration creates back-dated VAT liability, which means you owe VAT on sales you already made without collecting it.

How does Swiss VAT work in practice for businesses?

The mechanics of Swiss VAT center on the difference between output tax and input tax. Output tax is the VAT you charge your customers. Input tax is the VAT you pay your suppliers. Quarterly VAT returns are filed with the Federal Tax Administration, and your UID must appear on every invoice you issue.

Here is a practical example. A Swiss GmbH buys office equipment for CHF 10,000 plus 8.1% VAT, paying CHF 810 in input tax. It then sells consulting services for CHF 50,000 plus 8.1% VAT, collecting CHF 4,050 in output tax. The net VAT payable to the government is CHF 4,050 minus CHF 810, which equals CHF 3,240. The business keeps nothing. It simply passes the net amount to the Federal Tax Administration.

Key invoicing and accounting rules include:

Every VAT invoice must display your UID number.

Invoices must show the VAT rate applied and the VAT amount separately.

Records must be retained for at least 10 years.

VAT returns are typically filed quarterly, though annual filing is available for smaller businesses.

Precise record keeping on imports, domestic sales, and cross-border services is required to optimize tax credits and manage cash flow. Businesses that handle cross-border services also need to understand the reverse-charge mechanism, which shifts VAT liability from the foreign supplier to the Swiss recipient. For a deeper look at compliance best practices, the Swiss accounting guide for 2025 covers the reporting obligations in detail.

What is the territorial scope of Swiss VAT?

Swiss VAT applies to a defined domestic territory that extends beyond Switzerland’s political borders. For VAT purposes, the Principality of Liechtenstein, the German municipality of Büsingen am Hochrhein, and the Italian enclave of Campione d’Italia are all treated as Swiss domestic territory. Supplies within these areas follow Swiss VAT rules, not the rules of Germany or Italy.

Certain areas carry special exemptions:

The Samnaun valley and Sampuoir in Graubünden are customs-free zones and have special VAT treatment.

Duty-free warehouses operate under distinct rules that affect import VAT.

Goods imported into Switzerland from outside the domestic territory are subject to import VAT, which is separate from domestic VAT.

This territorial complexity matters for businesses with supply chains that cross these borders. A company shipping goods from Germany into Büsingen am Hochrhein is not making an export for Swiss VAT purposes. It is making a domestic supply. Getting this wrong creates double taxation or missed input tax claims. Understanding corporate ownership structures across borders can also affect how VAT obligations are assigned within a group.

Pro Tip: If your business operates near any of these territorial boundaries, map your supply chain against the Swiss VAT domestic territory definition before you file your first return. Corrections after the fact are costly.

What exemptions and special rules apply under Swiss VAT?

Some supplies are exempt or zero-rated under Swiss VAT law. The distinction between exempt and zero-rated matters significantly for input tax recovery.

Key exemptions and special rules include:

Health services: Medical treatments, hospital care, and related services are exempt. Providers cannot reclaim input VAT.

Education: Schools, universities, and training providers are generally exempt from VAT.

Cultural activities: Museums, theaters, and certain cultural events do not charge VAT.

Exports: Goods exported outside Swiss territory are zero-rated. The supplier charges no VAT but can still reclaim input VAT paid on related purchases.

Reverse-charge mechanism: When a Swiss business receives services from a foreign supplier, the Swiss business accounts for VAT itself rather than the foreign supplier charging it. This applies to digital services, consulting, and other cross-border supplies.

Startups and non-profit organizations may qualify for different treatment depending on their activities. A non-profit running educational programs is likely exempt, but one selling merchandise is not. The Federal Tax Administration publishes sector-specific guidance, and consulting a Swiss VAT specialist before you launch saves significant correction costs later. For foreign entrepreneurs, the compliance requirements for VAT registration are a practical starting point.

Key Takeaways

Swiss VAT is a federal consumption tax with three rates, a CHF 100,000 registration threshold, and a neutrality principle that places the final tax burden on the consumer, not the business.

Point | Details |

Three VAT rates | Standard 8.1%, reduced 2.6% for essentials, and 3.8% for hotels. |

Registration threshold | Businesses with global turnover above CHF 100,000 must register with the Federal Tax Administration. |

Input tax deduction | Businesses reclaim VAT paid on purchases and remit only the net difference to the government. |

Territorial scope | Liechtenstein, Büsingen am Hochrhein, and Campione d’Italia count as Swiss domestic territory for VAT. |

Exemptions matter | Health, education, and cultural services are exempt but cannot reclaim input VAT on purchases. |

Swiss VAT: what I have learned from working with foreign entrepreneurs

The most common mistake I see foreign entrepreneurs make is treating Swiss VAT as a simple add-on to their existing tax setup. It is not. The Swiss system is built on a neutrality principle that only works if you manage the input-output flow with discipline. When businesses ignore this, they end up either overpaying or facing penalties for under-reporting.

The CHF 100,000 global turnover threshold catches many foreign companies off guard. A business earning most of its revenue outside Switzerland but making occasional Swiss sales can cross the threshold without realizing it. By the time the Federal Tax Administration sends a notice, back-dated liability has already accumulated.

The territorial scope rules are another area where I consistently see errors. Entrepreneurs assume Swiss VAT applies only within Switzerland’s political borders. When they discover that Liechtenstein and Büsingen am Hochrhein are treated as domestic territory, their supply chain assumptions fall apart. Fixing this retroactively is expensive and time-consuming.

My practical advice: treat VAT planning as part of your company formation process, not an afterthought. The moment you decide to operate in Switzerland, map your revenue streams against the registration threshold, identify which rate applies to your products, and determine whether any of your supplies qualify for exemption. That upfront work saves months of corrections later.

— Rolands

Swiss company formation and VAT compliance with Rpcs

Setting up a Swiss company involves more than registering a legal entity. VAT registration, fiscal representation, and ongoing compliance are part of the operational reality from day one.

Rpcs provides Swiss company formation services that cover the full setup process, including VAT registration support, UID application, and accounting structure. For entrepreneurs who need ongoing financial reporting, Rpcs also offers accounting services tailored to Swiss VAT obligations, from quarterly return preparation to input tax reconciliation. Whether you are forming a GmbH, registering as a foreign branch, or appointing a fiscal representative, Rpcs handles the compliance details so you can focus on running your business.

FAQ

What is the standard Swiss VAT rate in 2026?

The standard Swiss VAT rate is 8.1%, applying to most goods and services. A reduced rate of 2.6% covers essentials like food and medicines, and a special rate of 3.8% applies to hotel accommodation.

Who needs to register for VAT in Switzerland?

Any business with global annual turnover exceeding CHF 100,000 must register for Swiss VAT. Non-Swiss companies crossing this threshold must also register and typically appoint a Swiss fiscal representative.

Can a foreign company be liable for Swiss VAT?

Yes. Swiss VAT liability is based on global turnover, not just Swiss revenue. A foreign company that exceeds CHF 100,000 in worldwide turnover while making taxable supplies in Switzerland must register.

What is the reverse-charge mechanism in Swiss VAT?

The reverse-charge mechanism requires Swiss businesses to self-account for VAT on services received from foreign suppliers. The Swiss recipient reports the VAT rather than the foreign provider charging it.

Are health and education services subject to Swiss VAT?

Health services, education, and cultural activities are exempt from Swiss VAT. Exempt suppliers do not charge VAT on their services but also cannot reclaim input VAT on their business purchases.

Recommended