Swiss Company Annual Reporting: Key Steps for Compliance

- Dec 29, 2025

- 7 min read

Most American founders launching a Swiss GmbH discover that annual reporting brings more than just paperwork. With Switzerland’s rigorous accounting rules and multi-layered tax requirements, compliance mistakes can quickly lead to heavy fines. For international entrepreneurs, understanding what authorities expect from your financial statements is essential for building trust and protecting your new business. You will see how clear guidelines and smart planning keep your Swiss company compliant while supporting long-term growth.

Table of Contents

Key Takeaways

Point | Details |

Importance of Compliance | Swiss companies must adhere to stringent financial reporting standards to maintain transparency and avoid penalties. |

Mandatory Financial Documents | Companies are required to prepare key documents such as balance sheets and income statements within six months of year-end. |

Varied Reporting Requirements | Reporting obligations differ based on company size and type, with public corporations facing the most stringent standards. |

Common Mistakes to Avoid | Companies should avoid using incorrect standards, incomplete disclosures, and missed deadlines to ensure compliance and protect their reputation. |

Swiss Company Annual Reporting Basics

Annual reporting for Swiss companies is a critical compliance requirement that demands meticulous attention to financial documentation and regulatory standards. Companies must navigate a complex landscape of accounting principles and disclosure requirements to maintain legal and financial transparency. The primary objective is presenting a comprehensive and accurate representation of the organization’s financial health.

Switzerland follows robust accounting standards embodied in the Swiss GAAP FER framework, which provides comprehensive guidelines for financial reporting. These standards are designed to ensure consistency, comparability, and clarity across different organizations. Key components include detailed financial statements, performance reports, and comprehensive disclosures that offer stakeholders a transparent view of the company’s economic situation.

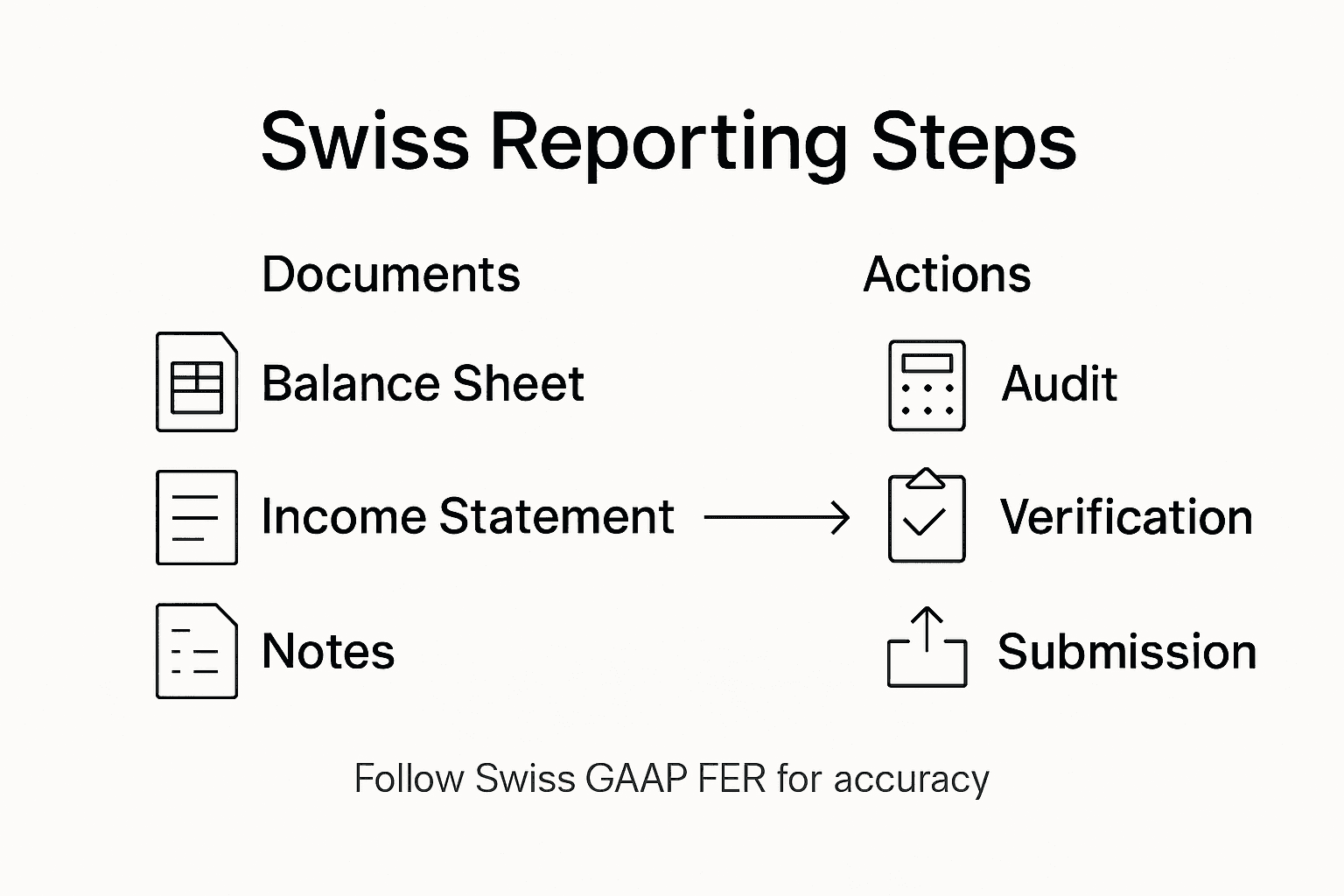

The reporting process typically involves preparing several mandatory documents: the balance sheet, income statement, cash flow statement, and notes to the financial statements. Listed public companies face additional requirements, such as complying with integrated reporting standards that go beyond traditional financial metrics to include sustainability and governance information. This holistic approach helps investors and stakeholders understand the company’s long-term value creation strategy.

Key reporting requirements vary depending on the company’s structure, with different standards applied to small businesses, medium enterprises, and publicly traded corporations. Companies must submit their annual reports within six months of the financial year-end, ensuring timely and accurate financial communication.

Pro tip: Engage a local Swiss accounting professional who understands the nuanced reporting requirements to ensure full compliance and avoid potential regulatory penalties.

Required Reporting Documents and Deadlines

Swiss companies must prepare a comprehensive set of financial documents that provide a transparent and accurate representation of their financial performance. The Swiss GAAP FER standards outline specific requirements for different types of organizations, ensuring consistent and reliable financial reporting across various business structures.

The core reporting documents typically include:

Balance Sheet: A snapshot of the company’s financial position at the end of the fiscal year

Income Statement: Detailing revenue, expenses, and overall financial performance

Cash Flow Statement: Demonstrating the movement of financial resources

Notes to Financial Statements: Providing additional context and detailed explanations of financial entries

For listed public companies, there are additional reporting requirements under international standards, which mandate more extensive disclosures. These include comprehensive information about corporate governance, sustainability efforts, and long-term strategic objectives. The reporting framework varies based on company size and type, with small businesses following simplified standards and public corporations facing more rigorous reporting obligations.

Deadline compliance is critical in Swiss financial reporting. Most companies must submit their annual reports within six months of the fiscal year-end, with specific deadlines varying depending on the company’s legal structure and listing status. Publicly traded companies often face more stringent timeline requirements, typically needing to file within three to four months after the financial year concludes.

Here is a comparison of Swiss annual reporting requirements by company type:

Company Type | Documentation Level | Audit Requirement | Reporting Deadline |

Small Entity | Simplified financials | Typically not required | 6 months after year-end |

Medium Enterprise | Standard disclosures | Mandatory annual audit | 6 months after year-end |

Public Corporation | Extensive integrated report | Strict external audit | 3-4 months after year-end |

Pro tip: Maintain a detailed annual reporting calendar and set internal deadlines at least one month before the official submission date to allow ample time for comprehensive document preparation and external auditing.

Legal Framework and Compliance Standards

The Swiss financial reporting landscape is governed by a robust and comprehensive legal framework that ensures transparency, accuracy, and accountability for businesses operating within the country. The Swiss Code of Obligations serves as the primary legislative foundation, establishing detailed requirements for corporate financial reporting and governance across different business structures.

Key compliance standards are structured based on company size and type:

Small Entities: Simplified reporting requirements

Medium-Sized Companies: Moderate disclosure and documentation standards

Public Corporations: Most extensive reporting obligations

The Swiss GAAP FER standards provide a comprehensive regulatory framework that complements legal requirements. These standards define specific accounting principles, ensuring consistent financial reporting across different organizations. Public companies face additional scrutiny, with the SIX Exchange Regulation imposing more stringent reporting and disclosure requirements to protect investor interests.

Companies must adhere to multiple layers of regulatory oversight, including annual audits, financial statement verifications, and compliance checks. Foreign-owned businesses operating in Switzerland must navigate these complex regulations while ensuring full alignment with local legal standards. Failure to comply can result in significant financial penalties, legal consequences, and potential suspension of business operations.

Pro tip: Engage a local Swiss legal and accounting expert to conduct a comprehensive compliance audit annually, ensuring your company remains fully aligned with the latest regulatory requirements.

Taxation, Costs, and Financial Transparency

Switzerland’s tax system represents a complex and nuanced framework that demands careful navigation by businesses and investors. Taxation in Switzerland operates through a multilayered system involving federal, cantonal, and municipal tax authorities, each contributing to the overall fiscal landscape.

Key tax considerations for businesses include:

Corporate Income Tax: Levied at federal, cantonal, and municipal levels

Capital Tax: Applied to a company’s net equity

Value-Added Tax (VAT): Standard rate of 7.7% for most business transactions

Withholding Tax: Applicable to certain dividend, interest, and royalty payments

The Swiss tax system is characterized by significant regional variations, with cantonal authorities enjoying substantial autonomy in setting tax rates. This decentralized approach creates opportunities for strategic tax planning, allowing businesses to optimize their tax positioning by carefully selecting their corporate domicile. Public corporations face more rigorous reporting requirements, with a focus on transparent financial disclosures that provide comprehensive insights into their fiscal structure.

Foreign-owned businesses must pay special attention to complex transfer pricing regulations and international tax treaties. The classical corporate tax system means that corporations and shareholders are taxed separately, which can lead to potential economic double taxation. Companies must maintain meticulous financial records and prepare detailed tax documentation to ensure full compliance and avoid potential penalties.

Pro tip: Consult with a specialized Swiss tax advisor who understands the nuanced cantonal tax differences to develop a strategic tax optimization approach for your specific business structure.

Common Reporting Mistakes to Avoid

Navigating the complex landscape of Swiss financial reporting requires meticulous attention to detail and a comprehensive understanding of regulatory requirements. Principles of effective business reporting emphasize the critical importance of avoiding common pitfalls that can compromise financial transparency and compliance.

Key reporting mistakes that companies frequently encounter include:

Incorrect Standard Application: Failing to use the appropriate Swiss GAAP FER standards for the company’s specific size and structure

Incomplete Disclosures: Omitting critical information in financial statement notes

Missed Deadlines: Not submitting reports within prescribed timelines

Inconsistent Accounting Practices: Shifting between accounting methods without proper justification

The Swiss GAAP FER framework provides a modular approach to financial reporting, but many companies struggle with precise implementation. Public corporations face additional scrutiny, with more complex reporting requirements that demand exceptional attention to detail. Misstatements in asset valuation, liability reporting, or inadequate documentation can lead to significant regulatory penalties and damage to the company’s financial reputation.

Foreign-owned businesses are particularly vulnerable to reporting errors due to differences in international accounting standards. Comprehensive documentation, consistent application of Swiss accounting principles, and proactive internal review processes are essential to mitigate risks associated with financial reporting mistakes. Companies must invest in ongoing training and maintain robust internal control systems to ensure full compliance with Swiss regulatory requirements.

This overview summarizes common reporting mistakes and how businesses can mitigate them:

Common Mistake | Business Impact | Preventative Action |

Using wrong standards | Legal penalties, restatements | Follow Swiss GAAP FER guidance |

Incomplete disclosures | Loss of stakeholder trust | Maintain detailed notes |

Missed deadlines | Fines, reputational damage | Set early internal deadlines |

Inconsistent practices | Audit issues, compliance risks | Standardize accounting procedures |

Pro tip: Conduct a comprehensive internal audit at least quarterly and engage an independent Swiss accounting expert to review your financial reporting processes before final submission.

Simplify Your Swiss Annual Reporting with Expert Support

Navigating the complex requirements of Swiss company annual reporting can be overwhelming, especially when dealing with compliance, auditing, and diverse financial documentation under Swiss GAAP FER standards. Whether you are a foreign entrepreneur or an international investor, fulfilling timely deadlines and avoiding common reporting mistakes are critical to protect your company’s reputation and legal standing.

Take control of your company’s financial transparency today by partnering with professionals who understand the nuances of Swiss reporting requirements. At RPCS, we specialize in comprehensive Swiss company services including legal formation, accounting, and ongoing compliance support. Our team guides you through every step—from preparing accurate financial statements to meeting strict audit standards—giving you peace of mind and allowing you to focus on growing your business.

Discover how our tailored solutions can ensure your Swiss annual reports are accurate, complete, and submitted on time. Visit RPCS to start your journey toward seamless compliance and enjoy the confidence that comes with expert assistance.

Frequently Asked Questions

What are the main documents required for annual reporting of a Swiss company?

The key documents required for annual reporting include the balance sheet, income statement, cash flow statement, and notes to the financial statements.

What is the deadline for submitting annual reports in Switzerland?

Most companies must submit their annual reports within six months of the fiscal year-end, while publicly traded companies have more stringent requirements, typically needing to file within three to four months after the fiscal year concludes.

How does the size of a company affect its annual reporting requirements in Switzerland?

The reporting requirements vary based on the company’s size, with small entities following simplified standards, medium-sized enterprises facing moderate disclosure requirements, and public corporations having extensive reporting obligations.

What are some common mistakes to avoid in Swiss annual reporting?

Common mistakes include using the incorrect accounting standards, incomplete disclosures, missed deadlines, and inconsistent accounting practices. Companies should implement robust internal controls and regular audits to mitigate these risks.

Recommended

Comments