What Is an AG in Switzerland – Key Facts for Investors

- Dec 12, 2025

- 7 min read

Updated: Dec 29, 2025

Most American investors discover that setting up a Swiss AG involves far more complexity than forming a typical limited liability company in the United States. With over 40,000 active Swiss AGs in Switzerland, this business structure remains a popular choice for those seeking legal protection, international credibility, and robust shareholder safeguards. Understanding the unique requirements and clearing up common misconceptions about Swiss AGs can prevent costly mistakes and help investors confidently navigate Swiss corporate law.

Table of Contents

Key Takeaways

Point | Details |

Swiss AG Structure | A Swiss Aktiengesellschaft (AG) provides limited liability for shareholders and requires a minimum capital of 100,000 Swiss francs. |

Incorporation Requirements | The incorporation process involves detailed legal steps, including securing initial capital and appointing a Swiss resident director. |

Shareholder Rights | Shareholders enjoy specific rights, such as voting at meetings and participating in governance, ensuring transparency and corporate accountability. |

Tax Considerations | Both AGs and GmbHs face distinct tax structures, affecting establishment costs and ongoing obligations requiring careful financial planning. |

Defining a Swiss AG and Common Misconceptions

A Swiss Aktiengesellschaft (AG) represents a sophisticated corporate structure designed for serious investors seeking legal protection and strategic business advantages. Unlike other business entities, an AG provides shareholders with limited liability and a robust framework for corporate operations. Swiss AG incorporation processes require careful understanding of specific regulatory requirements.

The Swiss AG functions as a distinct legal entity with shareholders who bear responsibility only up to their invested capital. This structure differentiates itself from partnerships by offering clear separation between personal and corporate assets. According to research from Swiss administrative sources, AGs must maintain a minimum share capital of 100,000 Swiss francs, with at least 20% paid in during initial registration. Shareholders can be individuals or corporate entities, providing significant flexibility for international investors.

Common misconceptions about Swiss AGs often stem from misunderstanding their operational dynamics. Many foreign entrepreneurs incorrectly assume that AGs are identical to limited liability structures in other countries. In reality, Swiss AGs have unique characteristics such as mandatory board representation, specific reporting requirements, and stringent corporate governance standards. The Swiss incorporation timeline involves multiple precise steps that differ substantially from simpler business registration processes in other jurisdictions.

Key distinctions between Swiss AGs and other corporate forms include:

Mandatory minimum capital requirements

Potential for public share trading

Complex governance structures

Strong legal and financial transparency

Significant protection for shareholder investments

Investors considering a Swiss AG must recognize that while these entities offer substantial benefits, they also demand meticulous compliance with Swiss commercial regulations. Professional guidance becomes essential to navigate the nuanced landscape of Swiss corporate law effectively.

Key Features of the Swiss AG Structure

The Swiss AG structure represents a sophisticated corporate framework designed to provide robust legal and financial protection for investors. With its unique characteristics, an AG offers significant advantages for businesses seeking stability and credibility in the international market. Swiss company registration processes demand meticulous attention to specific structural requirements that distinguish these entities from other corporate forms.

Key structural features of a Swiss AG include comprehensive governance mechanisms and financial transparency. The entity requires a minimum share capital of 100,000 Swiss francs, with shareholders bearing limited liability proportional to their investment. Board composition is critical, mandating at least one Swiss resident director and requiring clear delineation of executive and supervisory responsibilities. This structure ensures professional management and provides international investors with confidence in corporate oversight.

Financial and operational characteristics further distinguish the Swiss AG from alternative business entities. These corporations must maintain rigorous accounting standards, submit annual financial reports, and adhere to Swiss commercial regulations. Shareholders enjoy significant flexibility, with the ability to transfer shares and modify corporate structures while maintaining legal protections. The company formation checklist for Swiss AGs highlights the complexity and strategic advantages of this corporate model.

Primary features of the Swiss AG include:

Minimum capital requirement of 100,000 Swiss francs

Limited shareholder liability

Potential for public share trading

Mandatory professional corporate governance

Strong legal and financial transparency

Ability to operate across international markets

Investors considering a Swiss AG must recognize that while these entities offer substantial benefits, they also require sophisticated management and strict regulatory compliance. Professional guidance becomes essential in navigating the intricate landscape of Swiss corporate law and maximizing the strategic potential of this robust business structure.

Formation Requirements and Incorporation Process

Forming a Swiss AG involves a comprehensive series of legal and administrative steps designed to ensure rigorous corporate establishment standards. International investors must navigate a complex landscape of regulatory requirements that demand precision and professional expertise. Swiss incorporation timeline highlights the multiple stages entrepreneurs must successfully complete to establish their corporate entity.

The incorporation process begins with fundamental prerequisites that require meticulous preparation. Prospective AG founders must secure a minimum share capital of 100,000 Swiss francs, with at least 20% paid in during initial registration. Key initial steps include developing a detailed business plan, selecting a unique company name approved by Swiss commercial registries, and identifying at least one Swiss resident director. Founders must also draft comprehensive articles of incorporation and establish clear governance structures that comply with Swiss corporate regulations.

Documentation and legal compliance represent critical components of the Swiss AG formation process. Entrepreneurs must prepare and submit several mandatory documents, including:

Notarized articles of incorporation

Proof of initial capital contribution

Detailed business plan

Identification documents for all shareholders

Confirmation of Swiss resident director appointment

Bank statement verifying capital deposit

The registration process typically involves multiple governmental agencies, including cantonal commercial registries and federal tax authorities. Professional legal and accounting support becomes essential in navigating these complex administrative requirements. Investors should anticipate a formation timeline ranging from four to eight weeks, depending on the complexity of their corporate structure and the completeness of submitted documentation.

Successful Swiss AG incorporation requires more than merely completing administrative tasks. Investors must demonstrate a commitment to transparency, corporate governance, and ongoing compliance with Swiss commercial regulations. This approach ensures not only legal establishment but also positions the company for long-term operational success in Switzerland’s sophisticated business environment.

Shareholder Rights, Duties, and Corporate Governance

The Swiss AG governance model provides a sophisticated framework that carefully balances shareholder rights with robust corporate accountability. Investors in Swiss corporations benefit from a structured approach that ensures transparency, protection, and clear mechanisms for corporate decision-making. Swiss incorporation timeline reflects the comprehensive legal infrastructure that underpins these shareholder protections.

Shareholders in a Swiss AG possess distinct rights that safeguard their investments and provide meaningful corporate participation. These fundamental rights include voting at general meetings, accessing company financial reports, and participating in strategic decision-making processes. The Swiss legal framework mandates that shareholders receive equal treatment, with voting rights typically proportional to their share ownership. Key rights encompass:

Electing and removing board members

Approving annual financial statements

Participating in capital increases or reductions

Receiving dividend distributions

Challenging corporate decisions through legal mechanisms

Corporate governance in Swiss AGs demands rigorous standards of transparency and accountability. Companies must maintain detailed records, conduct annual general meetings, and provide comprehensive financial reporting. The board of directors carries significant fiduciary responsibilities, including strategic planning, risk management, and ensuring compliance with Swiss commercial regulations. Shareholders are protected by strict regulatory oversight that prevents potential misconduct and promotes long-term corporate stability.

The intricate balance between shareholder rights and corporate responsibilities requires professional management and legal expertise. International investors must understand that while Swiss AGs offer substantial protections, they also impose significant governance obligations. Successful navigation of these requirements demands a thorough understanding of Swiss corporate law, commitment to transparency, and proactive approach to corporate management.

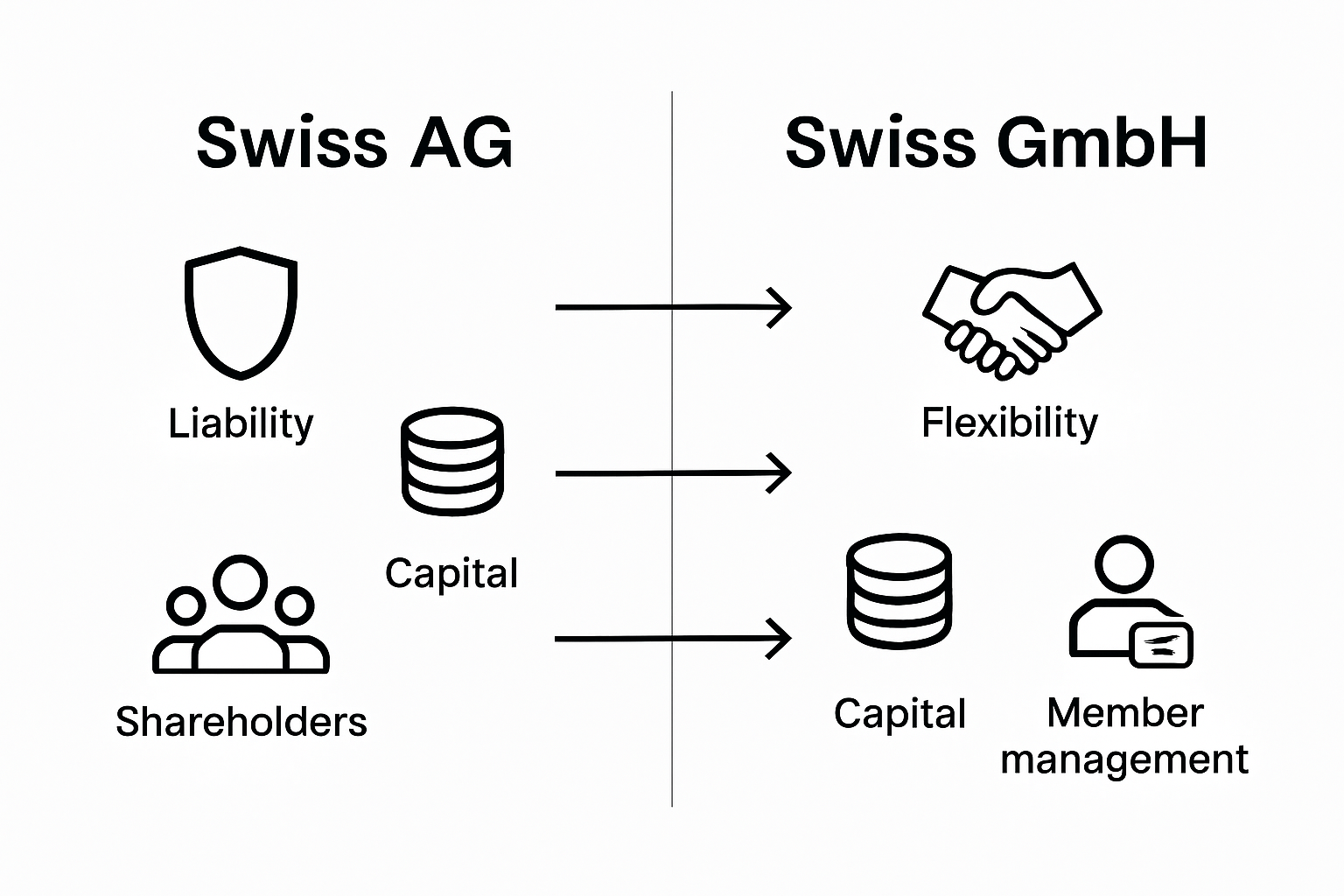

Taxation, Costs, and Comparison With GmbH

Taxation represents a critical consideration for investors evaluating Swiss corporate structures, with AGs and GmbHs presenting distinct financial characteristics. Advantages of Swiss GmbH highlight the nuanced differences between these two prominent business entities, particularly in terms of tax implications and operational costs.

Both Swiss AGs and GmbHs are subject to comprehensive corporate taxation frameworks that demand meticulous financial planning. The primary tax considerations include:

Corporate income tax at federal, cantonal, and municipal levels

Potential withholding taxes on dividend distributions

Capital taxes varying by canton

Wealth tax assessments

Additional social security contributions

Structural differences between AGs and GmbHs significantly impact their financial performance and tax efficiency. AGs typically require higher initial capital investments of 100,000 Swiss francs compared to GmbHs, which can be established with lower minimum capital. This variation directly influences establishment costs, ongoing financial obligations, and potential tax strategies. The Swiss accounting requirements further underscore the complexity of maintaining these corporate structures.

Key comparative aspects between Swiss AGs and GmbHs include:

Minimum capital requirements

Shareholder liability structures

Reporting and compliance obligations

Flexibility in corporate governance

Tax optimization potential

International investors must recognize that while both entities offer robust legal protections, the choice between an AG and GmbH depends on specific business objectives, anticipated growth trajectories, and long-term strategic goals. Professional tax advisory becomes crucial in navigating the intricate landscape of Swiss corporate taxation and selecting the most advantageous structure for individual business needs.

Navigate Swiss AG Formation With Confidence and Expert Support

Understanding the complexities of a Swiss AG, including mandatory capital requirements, governance standards, and regulatory compliance can feel overwhelming for international investors. Key challenges such as securing the minimum share capital, appointing a Swiss resident director, and maintaining transparent corporate governance demand precision and local expertise. Avoid costly delays or legal pitfalls by leveraging professional guidance that simplifies each step of your company formation journey.

Discover how expert legal and administrative support at RPCS can streamline your Swiss AG incorporation and ongoing management. Benefit from a trusted partner that handles everything from notarizing your articles of incorporation and securing bank accounts to ensuring full compliance with Swiss corporate law. Act now to secure your position in Switzerland’s stable and transparent business environment. Visit https://rpcs.ch to start your Swiss company registration process with confidence and turn your investment goals into lasting success.

Frequently Asked Questions

What is a Swiss AG?

A Swiss Aktiengesellschaft (AG) is a type of corporate structure that offers shareholders limited liability and protects personal assets while allowing for strategic business operations.

What are the minimum capital requirements for a Swiss AG?

To establish a Swiss AG, a minimum share capital of 100,000 Swiss francs is required, with at least 20% paid in at the time of registration.

What are the key governance features of a Swiss AG?

A Swiss AG has mandatory board representation, detailed reporting obligations, and requires at least one Swiss resident director to ensure effective corporate governance and accountability.

How does a Swiss AG differ from a Swiss GmbH?

The main differences between a Swiss AG and a GmbH include minimum capital requirements, shareholder liability structures, and specific governance and reporting obligations, making an AG generally suited for larger, more complex enterprises.

Recommended

Comments