Swiss Crypto Accounting Setup: CHF 100K AG vs CHF 20K GmbH

- Mar 1

- 12 min read

Switzerland’s approach to crypto regulation surprises many entrepreneurs. Rather than creating restrictive blockchain laws, FINMA applies existing financial regulations through a technology-neutral, function-based framework. This pragmatic model offers clarity while allowing flexibility, making Switzerland a top destination for crypto ventures. Understanding how to navigate Swiss accounting standards, entity structures, and compliance requirements is essential for foreign entrepreneurs establishing crypto businesses here.

Table of Contents

Key Takeaways

Point | Details |

Function-based regulation | FINMA regulates crypto activities based on economic function, not technology, ensuring adaptable oversight |

Entity capital requirements | AG requires CHF 100,000 minimum capital and suits licensing needs; GmbH requires CHF 20,000 and fits smaller startups |

Crypto as assets | Swiss accounting treats cryptocurrencies as assets under Code of Obligations, not cash equivalents |

Cantonal tax variation | Corporate tax rates differ significantly by canton, affecting profitability and strategic location choice |

Mandatory AML compliance | Anti-money laundering and KYC procedures required from day one to avoid penalties and maintain operations |

Introduction to Swiss Crypto Business Environment

Switzerland regulates crypto businesses with a pragmatic, technology-neutral, function-based model led by FINMA. This distinctive approach has positioned the country as a global crypto hub. Rather than enacting standalone blockchain legislation, Swiss authorities apply existing financial laws flexibly to crypto activities.

FINMA serves as the primary regulatory authority, focusing on the economic function a crypto business performs rather than the underlying technology. This functional approach means your business model determines regulatory requirements, not whether you use blockchain. The framework evaluates whether your activity resembles banking, securities trading, asset management, or payment services.

Several factors make Switzerland attractive for crypto ventures:

Political and economic stability provides a secure foundation for long-term operations

Robust financial infrastructure supports banking relationships and institutional partnerships

Government support for financial innovation creates a welcoming environment

Clear regulatory guidance reduces uncertainty and compliance risk

Technology neutrality allows businesses to innovate without regulatory obsolescence

This environment enables sustainable crypto business operations. Regulatory clarity means you can build compliance frameworks from the start rather than adapting to shifting rules. The Swiss model balances innovation with investor protection, creating conditions where legitimate crypto businesses can thrive while maintaining market integrity.

Legal Structures for Crypto Businesses in Switzerland

Choosing between AG and GmbH structures significantly impacts your crypto business trajectory. The decision affects capital requirements, licensing eligibility, investor confidence, and operational flexibility. Understanding these differences helps you choose the right Swiss company structure aligned with your business goals.

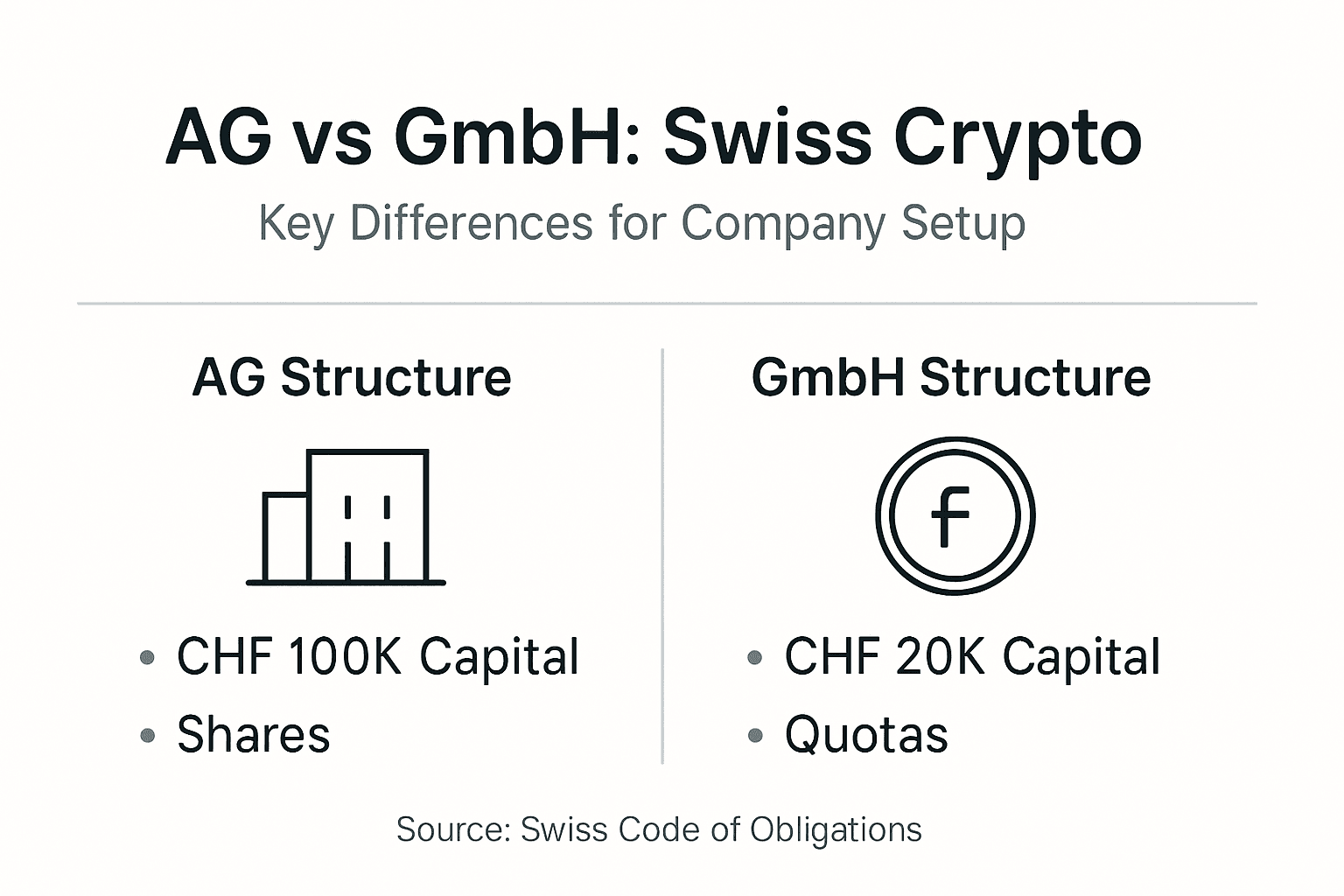

AG (Aktiengesellschaft) requires CHF 100,000 minimum share capital, with at least CHF 50,000 paid in at formation. GmbH (Gesellschaft mit beschränkter Haftung) requires CHF 20,000 minimum capital, fully paid at formation. Crypto assets contributed as in-kind capital must be valued at fair market price, meeting the same minimum thresholds.

Key structural differences include:

AG shares are freely transferable; GmbH shares require member consent for transfers

AG suits institutional investors expecting liquidity; GmbH fits closely held ventures

AG enables stock exchange listing; GmbH remains private

AG governance includes board and shareholders meeting; GmbH allows simpler structures

AG administration requires more formality; GmbH offers operational flexibility

Feature | AG | GmbH |

Minimum Capital | CHF 100,000 | CHF 20,000 |

Capital Paid In | CHF 50,000 minimum | CHF 20,000 (full) |

Share Transferability | Freely transferable | Restricted |

Licensing Suitability | Preferred for FINMA licenses | Suitable for simpler activities |

Investor Appeal | High (institutional) | Moderate (private) |

For crypto businesses seeking FINMA authorization, AG structure is typically preferred. Regulators and institutional partners view AG as more credible for licensed activities like custody, exchange operations, or asset management. The higher capital requirement demonstrates financial substance. The GmbH vs AG comparison reveals GmbH works well for consulting, software development, or advisory services not requiring licensing.

Pro tip: If you anticipate needing FINMA authorization within two years, start with AG despite higher costs. Converting GmbH to AG later involves significant legal fees, notarization, and registration expenses exceeding the initial savings.

Crypto contributions as capital require careful valuation. You must obtain an independent fair market assessment and document the valuation methodology. The notary verifies the valuation before registration. This process legitimizes your crypto holdings while meeting Swiss company formation legal requirements.

Swiss Regulatory Framework and Licensing by FINMA

FINMA’s function-based approach evaluates the economic substance of your crypto activities. This means identical technology applications can face different regulatory treatment based on how they function. Understanding this framework is crucial because it determines whether you need authorization and which rules apply.

FINMA classifies tokens into three categories:

Payment tokens function as means of payment or value transfer, similar to cryptocurrencies like Bitcoin

Utility tokens provide digital access to applications or services via blockchain infrastructure

Asset tokens represent rights such as ownership stakes, debt claims, or income streams

Many tokens combine characteristics from multiple categories. FINMA analyzes the predominant function to determine classification. This assessment drives regulatory requirements.

Licensing requirements depend on activities performed:

Crypto custody for third parties typically requires banking or securities dealer authorization

Crypto exchanges facilitating trading may need securities dealer or trading platform licenses

Asset management using client crypto assets requires asset manager authorization

Payment services accepting crypto payments may trigger payment system oversight

Issuing asset tokens can require prospectus approval or securities dealer licensing

Not all crypto businesses require FINMA authorization. Software developers, consultants, miners, and businesses holding crypto solely for their own account often operate without licenses. The critical factor is whether you perform regulated functions like accepting client assets, facilitating trades, or managing investments.

Early assessment of your business model against FINMA’s framework prevents costly surprises. Applying for authorization takes months and requires detailed documentation of business plans, compliance frameworks, qualified personnel, and adequate capital. Structuring your Swiss company with licensing in mind from inception streamlines the process.

FINMA expects ongoing compliance after authorization. You must maintain minimum capital, submit regular reports, undergo audits, and notify regulators of material changes. Building robust compliance systems from the start positions your business for sustainable growth within regulatory boundaries.

Accounting Standards and Treatment of Cryptocurrencies

Swiss law treats cryptocurrencies as assets, not cash equivalents. This fundamental classification shapes how you record, value, and report crypto holdings. Swiss accounting frameworks applicable to crypto include Swiss Code of Obligations and optionally Swiss GAAP FER, IFRS or US GAAP depending on company size.

The Swiss Code of Obligations mandates statutory accounting for all companies. This creates your legal books used for tax reporting, dividend calculations, and capital adequacy verification. Most small to medium crypto businesses use Code of Obligations standards exclusively, sometimes supplemented with Swiss GAAP FER for enhanced transparency.

Larger crypto firms or those seeking international credibility may adopt IFRS or US GAAP. These frameworks provide detailed guidance for complex instruments but require more extensive documentation and expertise. The choice affects how you present financial statements to investors, partners, and regulators.

Key accounting principles for crypto assets:

Cryptocurrencies appear on balance sheets as current or non-current assets based on holding intent

Trading portfolios typically use fair value measurement with changes through profit and loss

Long-term holdings may use cost less impairment under certain frameworks

Mining creates inventory recorded at production cost until sold

Staking rewards represent income when received and measurable

Valuation methodology depends on your business model and asset classification. Active traders mark positions to market regularly, recognizing gains and losses immediately. Long-term holders may carry assets at cost, testing for impairment when market values decline significantly below book value.

Consistent application matters more than which specific method you choose. Swiss authorities expect documented policies applied uniformly across reporting periods. Switching methods requires justification and restatement of comparative figures. Establishing proper Swiss accounting practices early prevents reconstruction headaches during audits or due diligence.

Documentation requirements extend beyond traditional accounting. You must maintain records linking wallet addresses to accounting entries, tracking cost basis for each crypto acquisition, and evidencing fair values used for measurement. Blockchain transparency helps verification but requires systems connecting on-chain activity to off-chain books.

Taxation and Cantonal Variations for Crypto Businesses

Switzerland’s federal structure creates tax complexity and opportunity. Corporate income faces federal tax around 8.5% plus cantonal and municipal taxes varying dramatically by location. Combined rates range from approximately 11% in low-tax cantons like Zug to over 20% in higher-tax regions.

Cantonal differences affect more than just rates:

Some cantons offer preferential treatment for qualifying intellectual property income

Innovation incentives reduce tax burdens for research-intensive crypto businesses

Holding company regimes provide relief for investment entities

Local authorities negotiate advance tax rulings clarifying treatment of novel crypto activities

Municipal variations within cantons add another layer of optimization opportunity

Proper accounting enables tax optimization. Accurate categorization of crypto income determines taxable amounts. Capital gains on crypto held as private wealth are generally tax-free in Switzerland, but gains from trading activity constitute taxable business income. The distinction depends on factors like trading frequency, leverage use, and holding periods.

Crypto businesses benefit from several tax-planning strategies. Structuring intellectual property ownership, allocating expenses across jurisdictions, and timing asset realization all influence tax outcomes. However, substance requirements have tightened. You need genuine economic activity and decision-making in Switzerland to justify tax positions.

Value-added tax applies to most business activities at 8.1% currently. Crypto exchanges may qualify for VAT exemption as financial services. Pure crypto-to-crypto exchanges typically escape VAT, while crypto-to-fiat transactions may trigger obligations. The Federal Tax Administration issues guidance on crypto VAT treatment, but gray areas remain.

Choosing your canton wisely enhances profitability. Beyond tax rates, consider regulatory environment, talent availability, infrastructure quality, and international connectivity. Zug’s Crypto Valley offers ecosystem benefits offsetting any premium over the absolute lowest-tax locations. The decision balances immediate tax savings against long-term strategic advantages.

Accounting Challenges and Practical Setup for Crypto Transactions

Crypto accounting complexity arises from diverse transaction types needing precise categorization and documentation. Your crypto business likely engages in multiple activities simultaneously, each with distinct accounting treatment. Staking generates income. Swaps trigger realization events. Airdrops create assets requiring valuation. NFT transactions involve unique identification challenges.

Common transaction categories requiring different treatment:

Spot purchases and sales establish cost basis and realize gains or losses

Staking rewards represent income at fair value when received

Liquidity provision creates complex positions requiring component tracking

Token swaps constitute taxable exchanges unless qualifying for specific relief

Airdrops and forks generate assets valued at receipt with zero or nominal cost basis

Gas fees represent transaction costs added to asset basis or expensed currently

Volatility compounds accounting difficulty. Fair values fluctuate dramatically between transaction and reporting dates. You need robust systems capturing real-time pricing from reliable sources. Manual tracking becomes impractical beyond minimal transaction volumes.

Specialized crypto accounting software is recommended to handle multiple wallets and regulatory reporting efficiently. Quality platforms integrate with exchanges and wallets, automatically importing transactions. They calculate cost basis using methods like FIFO, LIFO, or specific identification. They generate reports formatted for Swiss tax authorities.

Key software capabilities to prioritize:

Multi-wallet and exchange integration reducing manual data entry

Real-time pricing from multiple sources ensuring accurate valuations

Swiss-specific tax reporting templates aligned with cantonal requirements

Audit trails documenting every calculation and adjustment

Reconciliation tools identifying discrepancies between blockchain and books

Pro tip: Implement accounting systems before launching operations, not after accumulating transaction history. Retroactive reconstruction costs multiples of ongoing maintenance and introduces errors that haunt future audits.

Continuous monitoring prevents year-end surprises. Monthly reconciliations catch errors while corrections remain simple. Regular reviews identify optimization opportunities like loss harvesting or timing strategies. Building systematic accounting workflows establishes discipline supporting compliance and strategic decision-making.

Documentation extends beyond software. Maintain policies explaining your accounting choices, valuation methodologies, and internal controls. These policies demonstrate professionalism to auditors, investors, and regulators. They also ensure consistency as your team grows and personnel change.

AML Compliance and Ongoing Regulatory Obligations

Anti-money laundering and know-your-customer procedures are mandatory from business start for crypto firms. Swiss law imposes these obligations broadly, covering not just licensed entities but many crypto businesses operating without FINMA authorization. Failure to comply risks penalties and license revocation if you later seek authorization.

Core AML requirements include:

Customer identification and verification before establishing business relationships

Beneficial ownership determination for corporate clients and complex structures

Ongoing transaction monitoring detecting unusual patterns or suspicious activity

Suspicious activity reporting to MROS, Switzerland’s financial intelligence unit

Record retention for at least ten years covering customer data and transactions

Employee training ensuring staff recognize red flags and follow procedures

FINMA expects robust compliance frameworks aligned with risk profiles. High-risk activities like large-value custody or cross-border payment services demand more intensive controls than lower-risk consulting. Your framework should include written policies, designated compliance officers, independent testing, and continuous improvement processes.

Transaction monitoring presents technical challenges in crypto contexts. Blockchain transparency enables detailed tracking but generates massive data volumes. You need systems filtering normal activity from suspicious patterns. Thresholds and rules require regular calibration as business and threat landscapes evolve.

Suspicious activity indicators in crypto contexts include:

Structuring transactions to avoid reporting thresholds

Using mixers or privacy coins obscuring transaction origins

Rapid movement of large values through accounts without clear business purpose

Customers from high-risk jurisdictions lacking legitimate explanations

Transaction patterns inconsistent with stated business activities

Integrating AML early reduces operational disruptions. Building compliance into onboarding workflows, transaction systems, and reporting processes makes it routine rather than burdensome. Retrofitting compliance after establishing processes and customer relationships proves far more expensive and disruptive.

Ongoing obligations extend beyond AML. Licensed entities submit regular financial reports, undergo annual audits, notify regulators of material changes, and maintain minimum capital ratios. Even unlicensed crypto businesses face annual tax filings, statutory audits if exceeding size thresholds, and commercial register updates for corporate changes.

Common Misconceptions and Practical Considerations

Several myths about Swiss crypto regulation persist despite available guidance. Dispelling these misconceptions helps you make informed decisions and avoid costly mistakes.

Misconception 1: All crypto businesses need FINMA licensing. Reality depends on activities performed. Software developers, consultants, and businesses holding crypto solely for their own operations often require no authorization. Licensing applies when you custody client assets, facilitate trading, or manage investments.

Misconception 2: Cryptocurrencies count as cash in accounting. Swiss standards treat crypto as assets, not cash equivalents. This classification affects financial statement presentation, liquidity ratios, and capital adequacy calculations.

Misconception 3: GmbH and AG are interchangeable for crypto ventures. GmbH suits small firms without licensing needs. AG becomes necessary for FINMA authorization, institutional investors, or future token offerings. Choosing the right structure upfront avoids expensive conversions later.

Misconception 4: You can sort out compliance after launching. Early licensing assessment and AML integration prevent situations where you’ve built a business model that can’t achieve compliance. Regulators view retroactive compliance attempts skeptically.

Practical considerations for success:

Budget adequate time for licensing applications if required, often six to twelve months

Establish banking relationships early, as crypto businesses face enhanced scrutiny

Document everything, creating audit trails that satisfy regulators and investors

Invest in proper accounting systems from day one rather than fixing problems later

Engage Swiss legal and accounting advisors familiar with crypto-specific issues

Market credibility matters as much as legal compliance. Institutional partners, investors, and enterprise clients evaluate your regulatory posture. Operating without required licenses destroys credibility permanently. Maintaining licenses through compliant operations builds reputation as a trusted market participant.

Set Up Your Swiss Crypto Business with RPCS Solutions

Navigating Swiss crypto regulations and accounting requirements demands specialized expertise. RPCS offers comprehensive support for foreign entrepreneurs establishing compliant crypto businesses in Switzerland. We guide you through entity selection, ensuring your structure aligns with business goals and regulatory requirements.

Our Swiss company formation services streamline the incorporation process for both AG and GmbH structures. We handle legal documentation, notarization, commercial register filings, and initial compliance setup. For crypto ventures, we help structure capital contributions using digital assets and coordinate valuations meeting Swiss legal standards.

Beyond formation, our Swiss crypto accounting services provide ongoing support tailored to blockchain businesses. We implement specialized software, establish compliant accounting policies, and deliver regular reporting meeting Swiss standards. Whether you need help setting up a GmbH in Switzerland or navigating complex licensing requirements, RPCS delivers the expertise and support ensuring your crypto venture thrives in Switzerland’s dynamic regulatory environment.

Frequently Asked Questions

Who needs a FINMA license for crypto activities in Switzerland?

Licensing depends on functions performed, not technology used. Businesses providing crypto custody for clients, operating exchanges, managing digital assets, or issuing certain tokens typically require FINMA authorization. Software developers, consultants, and companies holding crypto solely for their own accounts often operate without licenses. Early assessment of your specific business model against FINMA’s functional criteria determines requirements.

Can I use my crypto holdings as capital to start my company?

Yes, Switzerland accepts crypto as in-kind capital contributions for both AG and GmbH formation. You must obtain an independent fair market valuation and meet minimum capital thresholds of CHF 100,000 for AG or CHF 20,000 for GmbH. The notary verifies valuation methodology before registration. This approach legitimizes your digital assets while satisfying Swiss legal capital requirements.

What accounting software is best for Swiss crypto firms?

Specialized crypto accounting platforms that integrate multiple wallets and exchanges work best. Look for software offering Swiss tax reporting templates, real-time pricing from reliable sources, and audit trail documentation. Quality platforms automate transaction imports, calculate cost basis accurately, and generate reports formatted for cantonal tax authorities. Implementing proper systems before launching operations prevents expensive retroactive reconstruction.

How do cantonal taxes affect my crypto business’s profitability?

Combined federal and cantonal corporate tax rates vary from approximately 11% in low-tax cantons like Zug to over 20% in higher-tax locations. Beyond rates, cantons differ in innovation incentives, advance ruling availability, and regulatory environments. Choosing your location strategically balances immediate tax savings against ecosystem benefits, talent access, and infrastructure quality affecting long-term success.

What AML steps are essential before starting operations?

Establish written AML policies, designate a compliance officer, and implement customer identification procedures before onboarding your first client. Set up transaction monitoring systems appropriate to your risk profile and train employees to recognize suspicious activity. Register with authorities if required for your business type. Integrating compliance from day one costs far less than retrofitting systems and relationships later.

Recommended

Comments