Swiss bank onboarding workflow: step-by-step guide for companies

- Apr 22

- 8 min read

TL;DR:

Swiss bank onboarding is highly rigorous due to strict AML/KYC compliance standards.

Preparing complete, accurate documents and understanding regulations ensures smoother approval.

Digital tools like video ID and automation speed up onboarding but require proper setup.

Imagine launching your Swiss GmbH or AG, ready to transact globally, only to have your chosen bank request a mountain of certified documents, compliance questionnaires, and weeks of verification before you can move a single franc. This scenario is more common than most guides admit. Swiss bank onboarding is genuinely rigorous, driven by some of the world’s strictest anti-money laundering standards. But with the right preparation and a clear workflow, you can move through the process efficiently, avoid costly rejections, and get your business account operational without unnecessary setbacks. This guide walks you through every phase.

Table of Contents

Key Takeaways

Point | Details |

Swiss onboarding is compliance-driven | Swiss banks apply strict AML and KYC rules so entrepreneurs must prepare fully to avoid delays. |

Document preparation is critical | Gathering and certifying all required documents prevents common setbacks and speeds up approval. |

Digital tools can save time | Video identification, e-ID solutions, and automation can reduce onboarding time by up to 80 percent. |

Proactivity reduces friction | Responding quickly to bank queries and maintaining open communication assures smoother processing. |

Understand Swiss regulatory and workflow basics

Before you start gathering documents or choosing a bank, it is crucial to grasp the underlying regulatory framework and why the workflow is so rigorous.

Switzerland’s banking sector operates under some of the most demanding compliance standards globally. Every Swiss bank, whether a cantonal institution, a global private bank, or a fintech platform, must follow AML/KYC-driven protocols mandated by the Swiss Financial Market Supervisory Authority (FINMA) and the Swiss Bankers Association (SBA). These are not optional guidelines. They are enforceable rules with real consequences for banks that skip steps.

The onboarding process itself moves through several distinct phases. First, the bank performs an initial risk assessment of your company and its principals. Then comes due diligence, where your documents are verified against public records and internal watchlists. After that, the bank completes a final review and either approves or declines your application. Missing information at any stage can freeze the entire process.

“The Swiss banking system’s integrity depends on every institution applying consistent, thorough onboarding standards. There are no shortcuts, only well-prepared applicants.”

Here is a quick overview of how the major onboarding phases compare across bank types:

Phase | Traditional banks | Fintech/digital banks |

Risk assessment | Manual, detailed | Automated scoring |

Document verification | In-person or mail | Digital upload |

Due diligence depth | High, often extended | Standard to high |

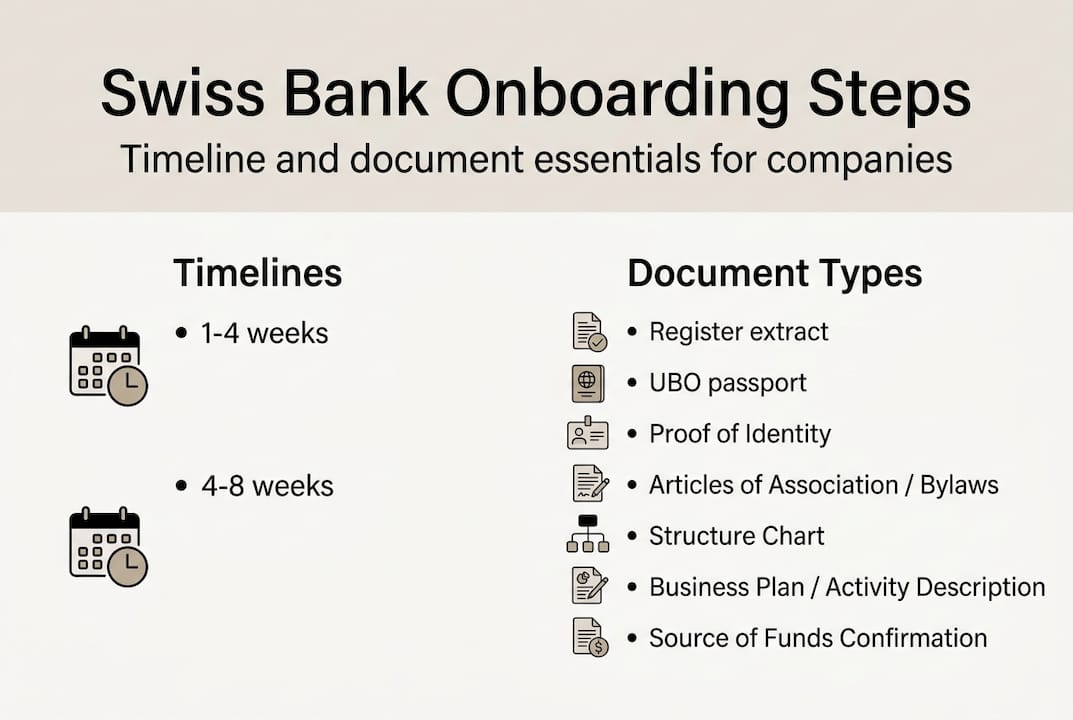

Typical timeline | 4 to 8 weeks | 1 to 4 weeks |

Video identification | Rare | Common |

Key regulatory requirements you need to know:

FINMA oversight: All banks must comply with FINMA’s digital onboarding amendments, which set technical standards for remote and video-based client identification.

SBA guidelines: The Swiss Bankers Association publishes detailed due diligence rules that all member banks follow.

UBO disclosure: Ultimate Beneficial Owners (UBOs) holding more than 25% of shares must be identified and verified without exception.

Source of funds: Banks must understand where your company’s capital originates, especially for international entrepreneurs.

Understanding Swiss banking requirements before you apply is not just helpful. It is the difference between a smooth process and a frustrating rejection.

Prepare all required documents and information

With the framework in mind, your next step is to gather every document Swiss banks require. Missing even one can set you back weeks.

Swiss banks maintain a strict document checklist, and they will not move forward until every item is verified. The core required documents include: certified articles of incorporation, a commercial register extract from Zefix dated within 30 days, valid passports or IDs for all UBOs and directors holding more than 25%, a shareholder register, a business plan, recent financial statements, and proof of address and source of funds for the company and its principals.

Beyond this baseline, banks often request additional supporting materials depending on your industry, country of origin, and the complexity of your ownership structure. High-risk sectors like crypto, real estate, or international trading typically face more scrutiny.

Here is a comparison of typical document requirements across bank types:

Document | Traditional bank | Fintech/digital bank |

Commercial register extract (Zefix) | Required, certified | Required, often via API |

Articles of incorporation | Certified copy | Certified copy |

UBO/director passports | Notarized copies | Scanned, liveness verified |

Business plan | Detailed, multi-page | Summary accepted |

Financial statements | 2 to 3 years preferred | Recent year or projections |

Source of funds declaration | Mandatory | Mandatory |

Proof of address | Utility bill or lease | Digital document accepted |

Additional items that commonly appear on bank request lists:

Corporate structure chart showing all entities and ownership percentages

Reference letters from existing banking relationships

Tax identification numbers for all key individuals

Contracts or invoices demonstrating business activity

You can use a company formation checklist to make sure your Swiss company documentation is complete before approaching any bank.

Pro Tip: If any of your documents are in a language other than German, French, Italian, or English, get certified translations prepared in advance. Banks will not accept uncertified translations, and waiting for a translator mid-process can add two to three weeks to your timeline.

Review your Swiss company document essentials early so nothing catches you off guard during the bank’s review.

Step-by-step overview of the Swiss bank onboarding process

Armed with your complete dossier, you are ready to move through the onboarding workflow itself. Here is each step laid out clearly.

Select the right bank. Match your company profile to the bank’s client focus. Fintech platforms suit lean startups; private banks suit high-net-worth structures. Research banking options for Swiss firms before committing.

Submit a preliminary inquiry. Many banks run a soft pre-screen before accepting a formal application. Use this to confirm eligibility and identify any immediate red flags.

Complete the formal application. Submit your full dossier, including all documents from the checklist above. Accuracy here is critical.

Preliminary compliance check. The bank’s compliance team reviews your application against internal risk criteria and external watchlists. This step can trigger requests for additional information.

Risk profiling. The bank assigns your company a risk category based on industry, geography, ownership structure, and transaction volume. Higher risk means more scrutiny.

Enhanced due diligence (EDD). If your company is flagged as higher risk, expect deeper investigation into source of funds, business relationships, and ownership chains.

Identity verification. This is where video identification (video ID) or in-person verification happens. Digital banks often use liveness detection and NFC passport scans.

Final approval and account activation. Once all checks pass, the bank issues your account details and you can begin transacting.

Onboarding timelines range from 1 to 4 weeks for fintech and retail banks, 4 to 8 weeks for traditional banks, and up to 3 months for fully manual compliance processes. Automation can reduce these timelines by as much as 80 percent, but only when your documents are complete and accurate from the start.

Steps 4, 5, and 6 are where most delays occur. Incomplete documents, inconsistent ownership data, or vague source of funds explanations are the most common triggers for follow-up requests.

Pro Tip: Assign one point of contact within your team to handle all bank communications. Inconsistent responses from multiple people raise compliance flags and slow everything down. When you open a Swiss business account, treat every bank interaction as a formal compliance event.

Digital onboarding: video ID, automation, and latest trends

With traditional and digital workflows often blending, it is vital to understand the latest technology and evolving compliance rules shaping modern onboarding.

Swiss banks are increasingly adopting digital tools to speed up client onboarding without reducing compliance rigor. Digital onboarding options now include video identification per FINMA Circular 2016/7 (updated for 2026), Zefix API data extraction for real-time company verification, liveness detection and NFC passport checks, and reverse transfer proofs to confirm account ownership.

FINMA’s evolving rules set technical requirements for digital identification, including minimum video quality, data encryption standards, and requirements for liveness detection to prevent identity fraud. Banks that offer digital onboarding must meet these standards, which means the experience is increasingly consistent across platforms.

Tool | Traditional bank | Digital/fintech bank |

Video identification | Rarely offered | Standard |

NFC passport scan | Not available | Widely used |

Zefix API integration | Manual lookup | Automated |

Liveness detection | Not used | Required |

E-signature | Limited | Fully supported |

To ensure your digital onboarding goes smoothly:

Test your internet connection before any video identification session. A dropped call can invalidate the session.

Prepare your documents digitally in advance, including high-resolution scans of passports and certified copies.

Confirm eligibility for digital onboarding with your chosen bank before starting, as some institutions still require in-person steps for certain company types.

Check your NFC-enabled passport works with the bank’s app if required.

“The question is not whether to automate onboarding, but how to automate it responsibly while keeping human judgment in the loop for complex cases.”

If your company involves a Swiss branch office or a more complex corporate structure, digital onboarding alone may not be sufficient. Some structures require additional manual review regardless of the bank’s tech capabilities.

A practitioner’s view: What most guides miss about Swiss bank onboarding

Most guides present Swiss bank onboarding as a checklist problem. Gather the documents, submit the application, wait for approval. But the real challenge is rarely about knowing what to submit. It is about submitting it correctly, consistently, and completely the first time.

We have seen entrepreneurs with perfectly legitimate businesses face repeated delays because their shareholder register did not match the commercial register extract, or because their source of funds explanation was technically accurate but lacked the narrative context a compliance officer needed to close the file. Banks are not looking to reject you. They are looking for reasons to approve you. Give them those reasons proactively.

Another underestimated factor is responsiveness. When a bank’s compliance team sends a follow-up request, how quickly and thoroughly you respond signals your reliability as a client. Slow or incomplete responses are interpreted as risk indicators, not just inconveniences.

Finally, do not optimize for speed at the expense of accuracy. Entrepreneurs who chase the fastest bank often end up in longer delays because they submitted incomplete dossiers to meet a self-imposed deadline. Reviewing Swiss company compliance tips before you begin will save you far more time than rushing the application.

Streamline Swiss bank onboarding with expert assistance

For entrepreneurs who want to avoid costly delays and simplify onboarding, partnering with an expert can make all the difference.

At RPCS, we support international entrepreneurs through every stage of Swiss bank account opening, from assembling your compliance dossier to coordinating directly with banking partners on your behalf. Our team understands what Swiss banks look for and how to present your company in the strongest possible light. We also provide Swiss company formation support and Swiss accounting solutions to keep your business fully compliant after your account is active. Contact us for a consultation and get your Swiss banking relationship started on the right foot.

Frequently asked questions

How long does Swiss company bank onboarding take?

Fintech and retail accounts typically take 1 to 4 weeks, traditional banks 4 to 8 weeks, and fully manual processes can extend up to 3 months depending on complexity.

Can non-residents open a Swiss company bank account remotely?

Yes, but most banks require video identification per FINMA Circular 2016/7, along with liveness checks and NFC passport verification for remote onboarding.

What documents are always required for Swiss bank account onboarding?

You will need to submit the commercial register extract, certified articles of incorporation, passports or IDs for UBOs and directors, a shareholder register, a business plan, financial statements, and proof of address and source of funds.

What are common reasons for onboarding delays or rejection?

The most frequent causes are incomplete documentation, discrepancies in ownership or due diligence data, or insufficient explanation of the company’s source of funds.

Recommended

Comments