Why Switzerland is a top fintech destination in 2026

- May 2

- 9 min read

TL;DR:

Switzerland’s principle-based regulation fosters faster market entry and greater product flexibility for fintech startups.

Crypto Valley in Zug leads Europe with significant VC funding and a dense ecosystem of blockchain companies.

The country’s political stability and low taxes create a favorable environment for long-term fintech success.

Switzerland rarely comes up first when people think of fintech hotbeds. Most founders default to London, Singapore, or New York. That instinct is understandable, but it misses something significant: Switzerland’s Crypto Valley in Zug alone attracted $728M in VC funding in 2025, representing 47% of all European blockchain venture capital. For a country of 8.7 million people, that number reframes the entire conversation about where the smartest fintech money actually flows.

Table of Contents

Key Takeaways

Point | Details |

Principle-based regulation | Switzerland’s flexible, innovation-friendly rules set it apart from prescriptive regimes. |

Multiple fintech entry routes | Sandboxes, fintech licenses, and DLT frameworks simplify market entry for startups. |

Unmatched stability | Switzerland’s political and financial steadiness builds trust and long-term opportunity. |

Crypto Valley advantage | Zug’s ecosystem offers unique network and funding benefits for blockchain ventures. |

Plan for cross-border limits | Swiss fintechs must strategically design their structures due to lack of EU passporting. |

Switzerland’s unique regulatory edge for fintech

When most people picture financial regulation, they imagine thick rulebooks, slow-moving bureaucrats, and lawyers billing by the hour to decode dense statutory text. Switzerland works differently. The Swiss Financial Market Supervisory Authority (FINMA) operates on a principle-based regulatory approach that prioritizes general principles over granular, prescriptive rules. In plain terms, this means the regulator asks what outcome do you need to achieve? rather than dictating exactly how you must achieve it.

This distinction matters enormously for fintech founders. Prescriptive frameworks, like those in certain EU member states, require you to fit your product into pre-existing rule categories. If your business model doesn’t map cleanly to an existing category, you face months of legal uncertainty. Switzerland’s approach is technology-neutral and competition-neutral, meaning it doesn’t favor one business model, payment rail, or technology stack over another.

Key benefits of this approach include:

Faster go-to-market timelines because founders spend less time navigating rule conflicts

Genuine product flexibility since regulators evaluate substance, not form

Lower compliance overhead at the early stages of product development

Reduced risk of sudden regulatory obsolescence when technology evolves

The Swiss State Secretariat for International Finance actively promotes this model, viewing it as a tool for keeping Switzerland competitive. Many of the business-friendly advantages that attract foreign entrepreneurs trace directly back to this regulatory philosophy.

“A principle-based framework treats entrepreneurs as capable of designing compliant solutions, rather than assuming they need to be handed a compliance manual at every step.” This trust-based dynamic creates genuine partnership between innovators and regulators, which is rare globally.

Pro Tip: Before engaging FINMA, document your business model’s intended outcomes clearly. Regulators here respond better to outcome-focused explanations than to product-feature lists.

Licensing options and fintech frameworks explained

Understanding Switzerland’s regulatory philosophy is one thing. Knowing which license actually applies to your business is another. Switzerland offers three primary regulatory paths for fintech companies, each designed for a different stage of business development and risk profile.

Here’s how the three main frameworks compare:

Framework | Deposit cap | Min. capital | Key restriction |

Regulatory sandbox | CHF 1 million | None | No interest paid, no investment of funds |

Fintech license (Art. 1b) | CHF 100 million | CHF 300,000 | No interest paid, no investment of funds |

DLT trading facility | Not applicable | Variable | Tokenized assets only |

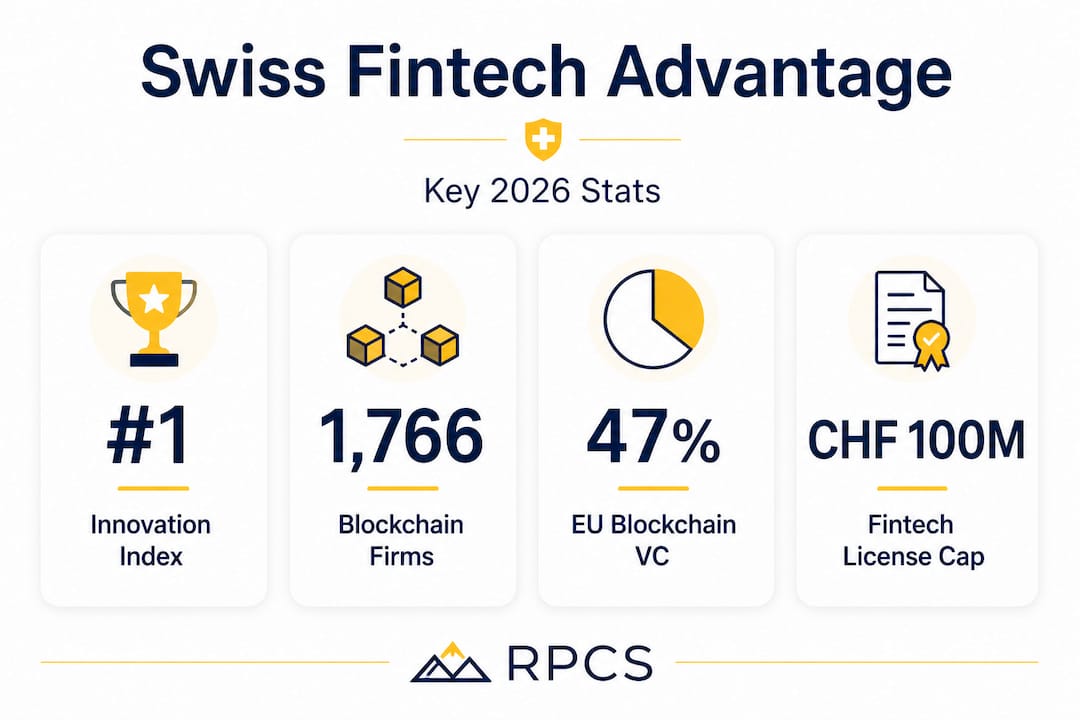

FINMA’s Fintech license, established under Article 1b of the Banking Act, is the most relevant tool for early-to-mid-stage startups. It allows deposit acceptance of up to CHF 100 million, requires minimum capital of CHF 300,000, and restricts firms from paying interest or investing client funds. That last point is a deliberate safety mechanism. The license is designed for payment processors, digital wallets, and custody services, not for deposit-taking banks.

The regulatory sandbox is even more accessible. With a cap of CHF 1 million, it’s designed specifically for testing and proof-of-concept phases. No license is required, no minimum capital is mandated, and you can operate for an extended period while refining your product.

The DLT framework, introduced in 2021, was a landmark move globally. Switzerland became one of the first major jurisdictions to create a specific legal framework for tokenized assets, covering DLT-based trading facilities and custodians. If your business involves tokenized securities, digital bonds, or blockchain-based settlement, this is your pathway. For a full walkthrough of the crypto-specific route, the crypto incorporation guide and steps to register a crypto company are worth reviewing before you make any formation decisions.

Here’s a practical sequencing approach for new entrants:

Map your business model to one of the three frameworks above

Determine whether your deposit volume will stay under CHF 1 million initially

Launch under the sandbox to test market assumptions without capital requirements

Once proven, apply for the Fintech license as you scale toward the CHF 100 million threshold

Engage legal counsel to assess DLT license applicability if you handle tokenized instruments

Your legal structure also matters. Choosing a company structure early in the process can save significant time during licensing applications.

Pro Tip: The sandbox is not a loophole. It’s a legitimate, FINMA-recognized mechanism. Use it strategically to validate your compliance model before committing to a full license application.

Political and economic stability: The Swiss advantage

Regulatory frameworks are only as reliable as the political environment that sustains them. Switzerland’s macro-level stability is not just a marketing talking point. It’s a measurable, empirical advantage backed by decades of consistent policymaking.

Switzerland has ranked #1 on the Global Innovation Index for 14 consecutive years, a streak that reflects the structural conditions enabling long-term innovation rather than short-term policy spikes. The drivers behind this consistency include:

Direct democracy: Major policy changes require popular approval, which prevents sudden regulatory shifts that can blindside investors

Political neutrality: Switzerland’s non-alignment reduces exposure to geopolitical disruptions that affect other financial centers

Independent central bank: The Swiss National Bank operates without political pressure, maintaining monetary stability

Low inflation: Switzerland consistently records among the lowest inflation rates in the developed world

Safe-haven Swiss Franc: The CHF is globally recognized as a store of value, providing investors with currency-level confidence

For fintech entrepreneurs raising capital or managing treasury, these factors translate directly into operational confidence. Currency risk, political instability, and regulatory reversals are real costs that erode startup runways. Switzerland’s track record minimizes all three.

This isn’t just favorable for investors. It’s favorable for your team, your banking relationships, and your ability to plan 3 to 5 years forward. The credibility and advantages for startups that come from operating in this environment extend into how international clients and banking partners perceive your company. Foreign entrepreneurs who have relocated to Switzerland frequently cite this stability as the primary long-term retention factor.

Crypto Valley and the rise of blockchain innovation

The canton of Zug sits about 30 kilometers south of Zürich. By population, it’s unremarkable. By blockchain density, it’s arguably the most important square kilometers in global Web3 development.

Crypto Valley now houses 1,766 blockchain companies, a 134% increase since 2020. The top 50 companies in the ecosystem are valued collectively at $467 billion. Ethereum’s Zug Foundation, Cardano’s IOHK, Polkadot’s Web3 Foundation, and dozens of other major protocols have established their legal entities here. This isn’t coincidence. It’s the product of deliberate regulatory clarity combined with network effects that now reinforce themselves.

The VC numbers tell a clear story. In 2025:

$728 million in total VC flowed into Crypto Valley

47% of all European blockchain VC landed in Switzerland

37% year-over-year growth, at a time when global fintech funding was declining in many other regions

62% of funding concentrated in blockchain network infrastructure

These aren’t vanity metrics. For a founder deciding where to incorporate, the density of capital, legal expertise, technical talent, and peer networks in Zug creates a compounding advantage. You’re not just incorporating in a stable country. You’re embedding your company into a live ecosystem where your next investor, technical co-founder, or banking relationship is a coffee meeting away.

“Crypto Valley’s network effects have reached the self-sustaining phase. The presence of major protocols and institutional-grade VC funds attracts founders, which attracts more capital, which attracts more founders.”

For international entrepreneurs launching in Switzerland, the practical implication is clear: locating in Zug isn’t just a tax decision. It’s a strategic positioning decision with compounding returns over time.

Considerations for international entrepreneurs

Switzerland offers real advantages, but it also comes with specific constraints that founders must understand before committing. A clear-eyed view of both sides leads to better structuring decisions.

The tax advantages are significant, particularly in Zug, where effective corporate tax rates can be among the lowest in Europe for qualifying structures. For crypto businesses generating income from token sales, staking rewards, or protocol fees, this can translate into substantial savings compared to operating from Germany, France, or the UK.

Use this checklist when planning your entry:

Define whether your product involves deposit-taking and at what volume

Confirm whether your target clients are Swiss, EU-based, or global

Assess whether you need EU passporting for your revenue model

Identify your applicable FINMA license category before incorporating

Evaluate canton-specific tax rates based on your revenue and profit profile

Review whether your token or digital asset qualifies as a security under Swiss law

The most important constraint to understand clearly: Switzerland does not offer EU passporting. A Swiss Fintech license does not automatically allow you to serve retail clients across EU member states. If your revenue model requires direct EU market access, you’ll need either a separate EU entity or a distribution agreement with a licensed EU firm. This is not a dealbreaker, but it does require careful business model design from day one. The company formation checklist covers many of these structural decisions in practical terms.

Key opportunities to prioritize:

Tax optimization through canton selection, particularly Zug and Schwyz

Sandbox use to reduce early compliance costs while building product-market fit

DLT framework access for tokenized asset businesses with global client bases

Access to Crypto Valley’s ecosystem for networking, talent, and capital

Pro Tip: If EU market access is central to your growth plan, structure a Swiss parent entity with a subsidiary in an EU member state like Luxembourg or Ireland. This gives you Swiss stability plus EU regulatory reach.

A founder’s perspective: The real calculus for fintech success in Switzerland

Here’s what most articles won’t tell you: Switzerland doesn’t reward founders who move fast and figure out compliance later. It rewards founders who invest in understanding the nuance upfront and then move confidently.

We’ve seen this pattern repeatedly with international founders who treat Swiss regulation as a formality. They incorporate quickly, open a bank account, and then hit a wall when a banking partner or institutional client asks detailed questions about their FINMA status, their AML program, or their data segregation practices. Those conversations become expensive and time-consuming, often delaying meaningful revenue by 6 to 12 months.

The founders who thrive here do something different. They treat the sandbox as a genuine learning environment, not a temporary workaround. They engage legal counsel at the structuring phase, not after the product is built. They choose their canton based on tax modeling, not on where a friend incorporated. These decisions are boring, but they’re the calculus that separates Swiss fintech success stories from expensive detours.

Switzerland’s 47% share of European blockchain VC in a year when global fintech funding was contracting should tell you something important: the capital here is disciplined and long-term. It flows toward companies that demonstrate regulatory sophistication, not just technical innovation. That’s actually a feature for founders who are serious about building durable businesses. It filters out the noise.

The mainstream fintech narrative focuses on big markets. Switzerland proves that market size is secondary to ecosystem quality. The foreign entrepreneurs who have built meaningful companies here understood this early. They saw Switzerland’s constraints not as limitations but as forcing functions that produced better, more defensible businesses.

How RPCS helps you launch and grow your fintech venture in Switzerland

Understanding the Swiss fintech landscape is one thing. Executing your entry without missteps is another.

At RPCS, we work directly with fintech founders and crypto entrepreneurs to handle the full formation process, from choosing the right legal structure to coordinating notarization, registration, and ongoing compliance. Our team manages Swiss company formation for GmbH and AG structures tailored to fintech and blockchain businesses. We also help you open a Swiss bank account, which remains one of the most challenging bottlenecks for foreign founders without local relationships. Beyond formation, our accounting services for Swiss fintechs keep your books clean and compliant from the first day of operations. If you’re ready to stop planning and start building your Swiss presence, we’re the team that knows how to get it done correctly the first time.

Frequently asked questions

What is Switzerland’s Fintech license and who should use it?

The Swiss Fintech license allows firms to accept up to CHF 100 million in deposits with minimum capital of CHF 300,000, making it ideal for payment platforms, digital wallets, and custody services that do not pay interest or invest client funds.

Does Switzerland give fintech companies access to the entire EU market?

Switzerland does not offer EU passporting, so your Swiss license does not automatically cover EU retail clients. Careful business model design or a separate EU entity is required for full EU market access.

Why is Zug called Crypto Valley?

Zug earned the name due to its dense concentration of 1,766 blockchain companies and its status as the top destination for blockchain VC in Europe, capturing 47% of all European blockchain venture capital in 2025.

How do Swiss taxes for fintech founders compare to other countries?

Switzerland offers some of Europe’s most competitive corporate tax rates in key cantons like Zug and Schwyz, making it especially attractive for crypto and fintech businesses optimizing for long-term profitability.

Recommended

Comments